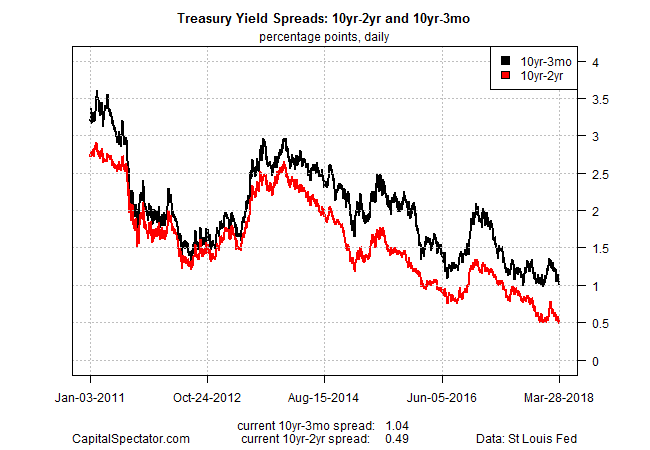

Two Federal Reserve officials have recently dismissed it. But a research note published this month by the San Francisco Fed paper advises that the yield curve is still a relevant economic signal for monitoring the business cycle. The disparate views within the central bank arise as the yield difference between the 10-year and 2-year rates continue to plumb new post-recession lows.

This widely followed spread fell to 49 basis points yesterday (March 28). The slide marks the lowest print since October 2007, just two months before the Great Recession started. Not everyone sees this as a warning, but the San Francisco Fed reminds in a research commentary from earlier this month that the yield curve has shown strong “predictive power” in forecasting US recessions.

Is this time different? Yes, according to some analysts, including Federal Reserve Chairman Jerome Powell. Last week, he effectively dismissed the value of the yield curve as a recession predictor because inflation is low and stable, in contrast with previous decades. Cleveland Federal Reserve President Loretta Mester echoed that skepticism on Monday, asserting that there is “no evidence” for thinking that a flatter curve signals a weaker economy at this time.

The San Francisco Fed begs to differ, explaining that “while the current environment appears unique compared with recent economic history, statistical evidence suggests that the signal in the term spread is not diminished.”

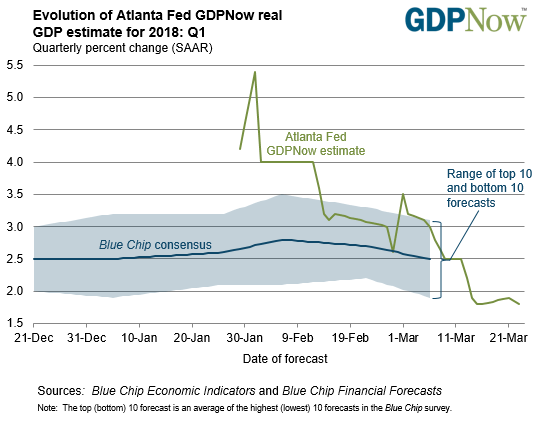

The debate about the relevance of the yield curve is sure to heat up if the spread continues to slide. Although the rate difference is still mildly positive, the latest dip follows downgrades in first-quarter GDP growth via the Atlanta Fed’s widely followed GDPNow model. The March 23 update trimmed the Q1 estimate to 1.8%, more than a percentage point below the 2.9% gain in last year’s Q4.

To be fair, a low yield spread shouldn’t be confused with a negative spread. History shows that relatively low readings for the 10-year/2-year rate difference can persist for years with an expanding economy — in the mid-1990s, for example. Perhaps a repeat performance describes the current climate.

Leave A Comment