The financial sector still gets a bad rap. Seven years after the financial crisis and justifiably so.

In his 2013 book “Finance & The Good Society,” economist Robert Shiller describes a utopia where finance can benefit today’s society. He identifies how financial innovations of the past, like insurance and pensions for example, improved the lives of the masses. The lauded professor at Yale shares his suggestions about the future of finance and how the industry can reform and prosper by serving the common good.

Can you imagine?

Yea, me neither.

I’m sorry to be cynical but you have a better chance of finding a unicorn in your driveway and taking it for a trot over a magical rainbow.

The halcyon days for finance are over.

Today, in the shadow of the Great Recession, forgotten by Wall Street and insidiously faded into the fog of averages, the financial industry is more than ever a marketing machine designed to convince the masses to purchase products they don’t need and to stick with investments that offer more risk for less reward.

The pundits seek to convince, not enlighten. They warn (scare) that if we don’t invest in the manner they suggest, we are in great danger of outliving our money, the boogey-man of inflation will inevitably arise from under our cash and devour our nest egg while we sleep.

From behind their manipulated statistics, these ‘experts’ communicate in serious tones a cozy belief that your household balance sheet has recovered from the Great Recession.

You know better.

Now, more than any other period since 2008, retirees and those near retirement, are vulnerable to the lies that appear pervasively in financial media.

Survival depends on you knowing the difference between white lies that don’t matter and dark fabrications that have the potential to derail your retirement planning.

There are three financial lies you must ignore to preserve your wealth right now.

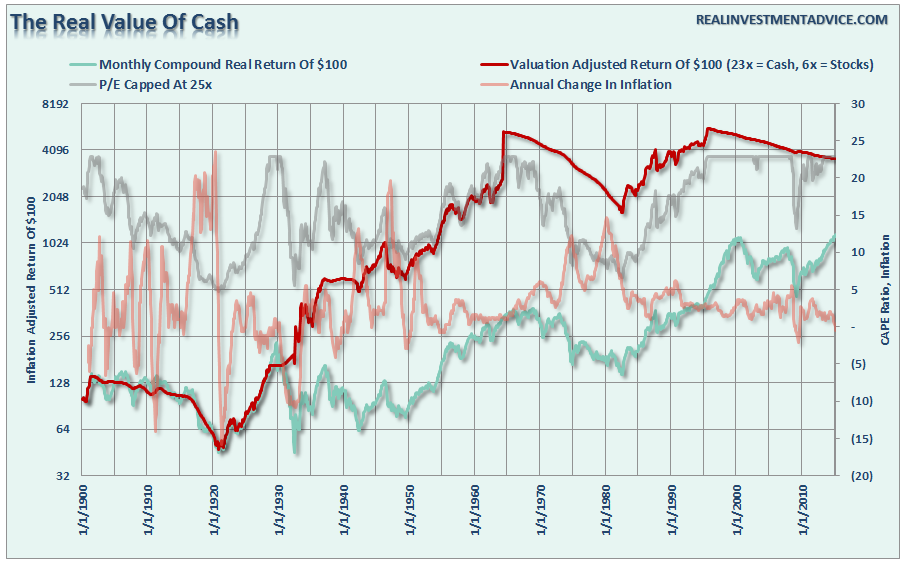

Lie #1 – Cash is trash.

Many financial talking heads consider holding cash dangerous to their livelihoods. Why maintain cash when money could be allocated to expensive managed accounts or locked up in investment vehicles where ongoing fees can be charged.

These cunning souls know if they can convince you to remain invested at all times, especially when markets are sliding, then the financial firms they represent can continue to make a predictable revenue stream to appease shareholders.

The experts hope you fall victim to the behavioral pitfall labeled anchoring. When emotionally connected to a loss, you’ll wait for that losses to recover to your original purchase price before taking action, even if the current value reflects a change in fundamentals. The opportunity cost of sticking with losing investments and waiting for recovery can be detrimental to your financial health.

Leave A Comment