In addition to boosting the intangible “wealth effect” by raising consumer confidence and encouraging spending, rising stock prices have a benign effect on the broader economy by directly stimulating US economic growth and GDP. And vice versa: when stocks drop, tightening financial conditions, US GDP is impacted adversely.

That’s the observation made in a Friday note from Goldman economists, which tries to quantify the growth effect of the equity sell-off, and finds that “the stock market is likely to turn from a significant contributor to strong growth at the start of the year into a modest drag next year, barring a further rebound in equity prices.”

Picking up where another recent Goldman note left off, which as we discussed yesterday concluded that the Fed will have to hike rates more than the market expects in order to substantially tighten financial conditions and slow down the economy, bank economists Jan Hatzius and Dean Struyven write that “the 6% decline in the stock market since late September has been the most important driver of the recent tightening in financial conditions.” As a result, the bank now estimates “that the 0.5% boost to GDP growth from higher equity prices at the start of the year has already disappeared.”

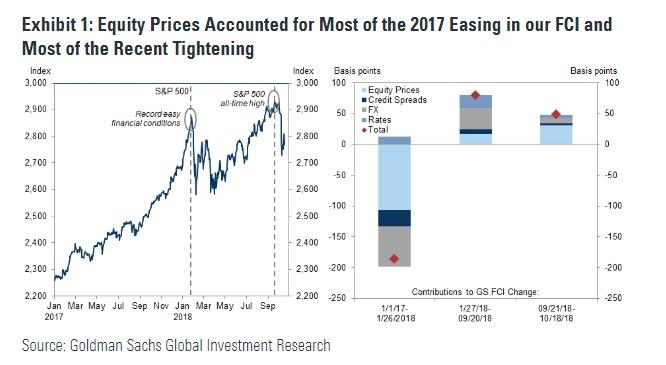

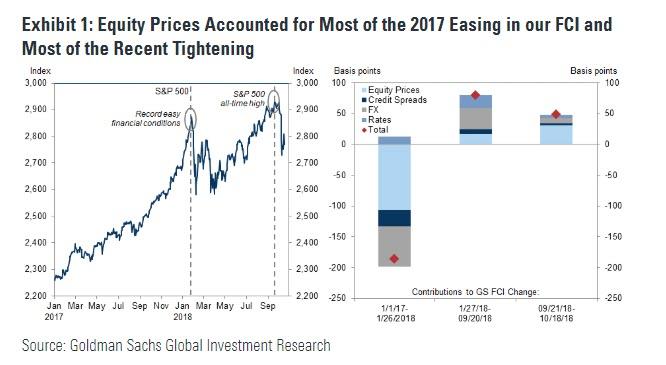

As shown in the chart above, Goldman explains that the run-up in the equity component, i.e. rising stock prices, of the Financial Conditions Index drove most of the 185 basis points easing from the start of 2017 till late January, when the index hit its record low. Conversely, the 6% sell-off in the S&P 500 since the September all-time high has been the biggest factor in the tightening of financial conditions and has accounted for two thirds of the roughly 50bp FCI tightening over the last month (other factors include the rise in rates and the dollar which account for about half of the -1.5% swing in the FCI impulse from +0.75pp at the start of the year to -0.75pp in the first half of next year).

Leave A Comment