Yesterday’s upbeat report on consumer spending and income in the US provides fresh support for last week’s moderately hawkish comments from Fed officials, who hinted that another interest-rate hike is near, perhaps as early as next month’s Federal Open Market Committee (FOMC) meeting. Yet support for pricing in a new round of policy tightening is modest at best via Treasury yields. Is that because job growth is expected to slow in this Friday’s employment report for July after two months of strong increases?

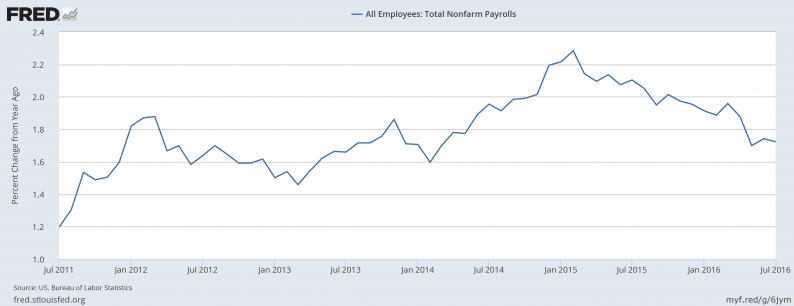

Total nonfarm payrolls are on track to rise by a moderate 175,000 in August, according to Econoday.com’s consensus forecast. That’s a decent gain, but it’s well below July’s increase of 255,000 and July’s 292,000 surge. Monthly data is noisy and so it’s best to focus on the year-over-year trend. The August estimate translates into a 1.74% increase vs. the year-earlier level, fractionally above July’s annual pace.

Job growth has clearly slowed in year-over-year terms, which isn’t terribly surprising for an economic recovery that’s celebrated its seventh birthday in June—one of the longest expansions on record, according to NBER data. The question is whether the Fed will feel compelled to continue squeezing rates when the trend for job growth is on a downward trajectory?

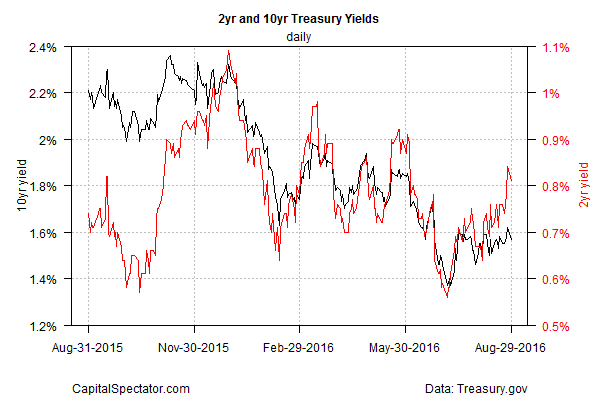

The Treasury market isn’t discounting the possibility of a rate hike in the near term, but there’s still a fair amount of skepticism. Consider the 2-year yield, which is highly sensitive to rate expectations. Although this widely followed maturity has bounced higher in recent weeks, yesterday’s rate eased to 0.81%, based on daily data from Treasury.gov. That’s still well below the nearly 1.0% rate that prevailed in early March, when fears were widespread that a new recession was lurking.

Fed fund futures yesterday (Aug. 29) were pricing in a 21% probability of a rate hike for the Sep. 20-21 FOMC meeting, down slightly from last week’s peak, based on CME data.

Leave A Comment