Today I revisit a subject that was prominent in the American conscious post-global economic crisis and brought to the forefront by the rare earth element and lithium bubbles from 2009 to 2011:

The United States of America depends on imported supplies for most of its industrial metals, minerals, and materials demand.

I spoke and wrote extensively about the US of A’s dearth of domestic production and dependence on risky, corrupt, unstable, and/or unfriendly sources in 2011 and 2012. Here are selected examples: (Mercenary Interview March 4, 2011; Mercenary Musing, August 6, 2012; Mercenary Video, June 9, 2012).

Over the past 14 months, the Trump administration has rolled back government regulations, streamlined bureaucracies, cut taxes, and proposed major infrastructure buildouts and tariffs on imports of aluminum, steel, and Chinese goods. Combined with a stronger economy, booming stock markets, and higher commodity prices, it seems likely that mineral demand will increase in the short to midterm. So this is an opportune time to provide an update on our overwhelming reliance on foreign sources to meet domestic mineral demand.

The United States Geological Survey publishes an annual compendium of mineral and material commodities and documents domestic production, imports, exports, apparent consumption, and official government stockpiles among other data (USGS Mineral Commodities Summaries).

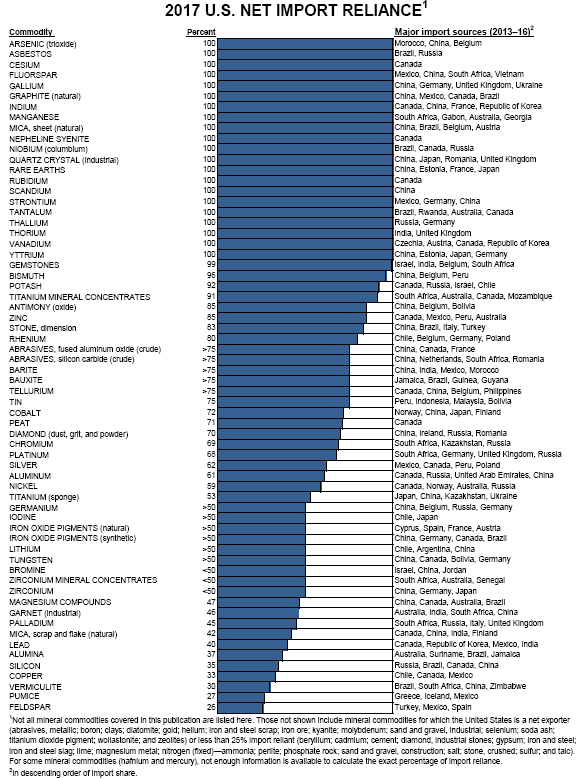

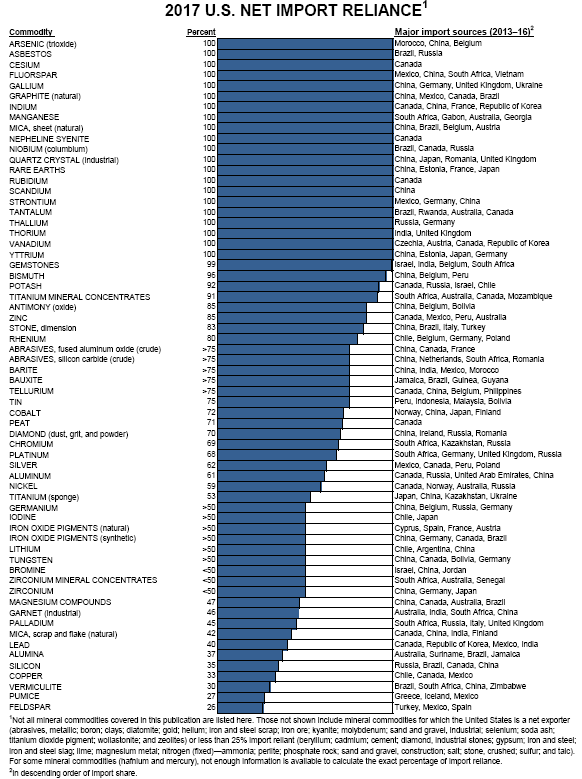

Let’s start with a chart from the 2017 publication that shows US net import reliance for the 64 industrial metals, minerals, and materials with >25% dependence:

From the chart and footnote listings in the USGS document:

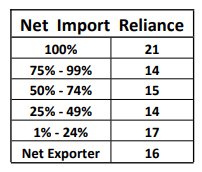

The 2017 United States net import reliance data for 97 minerals is summarized in the following table:

Americans should be concerned not only because of our dependence on other countries for the majority of essential industrial commodities but also because of some of the countries that we are most dependent on.

Let’s look at countries that are unfriendly, unstable, and/or corrupt and the number of materials for which we import a quarter or more (25%) of annual demand:

The United States, despite being >25% dependent on foreign sources for 64 materials, holds strategic stockpiles of only 14.

Leave A Comment