Lately, there has been a lot of chatter about the “Return Of Animal Spirits” as the catalyst to drive markets higher…and higher…and higher. But exactly what does that mean?

Animal spirits came from the Latin term “spiritus animalis” which means the breath that awakens the human mind. Its use can be traced back as far as 300BC where the term was used in human anatomy and physiology in medicine. It referred to the fluid or spirit that was responsible for sensory activities and nerves in the brain. Besides the technical meaning in medicine, animal spirits was also used in literary culture and referred to states of physical courage, gaiety, and exuberance.

It’s more modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money,” wherein he used the term to describe the human emotions driving consumer confidence. Ultimately, the “breath that awakens the human mind,” was adopted by the financial markets to describe the psychological factors which drive investors to take action in the financial markets.

The 2008 financial crisis revived the interest in the role that “animal spirits” could play in both the economy and the financial markets. The Federal Reserve, then under the direction of Ben Bernanke, believed it to be necessary to inject liquidity into the financial system to lift asset prices in order to “revive” the confidence of consumers. The result of which would evolve into a self-sustaining environment of economic growth.

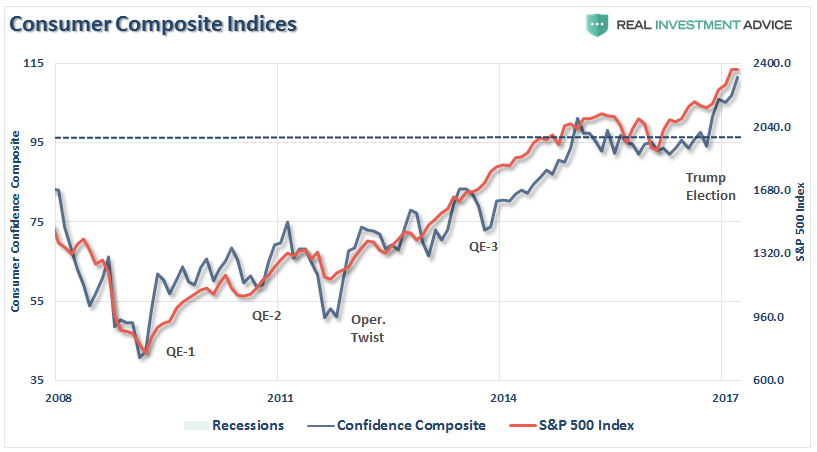

Ben Bernanke & Co. were successful in fostering a massive lift to equity prices since 2009 which, in turn, did correspond to a lift in the confidence of consumers. (The chart below is a composite index of both the University of Michigan and Conference Board surveys.)

Unfortunately, despite the massive expansion of the Fed’s balance sheet and the surge in asset prices, there was relatively little translation into wages, full-time employment, or corporate profits after tax which ultimately triggered very little economic growth.

The problem, of course, is the surge in asset prices remained confined to those with “investible wealth” but failed to deliver a boost to the roughly 90% of American’s who have experienced little benefit. In turn, this has pushed asset prices, which should be a reflection of underlying economic growth, well in advance of the underlying fundamental realities. Since 2009, the S&P has risen by roughly 220%, while economic and earnings per share growth (which has been largely fabricated through share repurchases, wage and employment suppression and accounting gimmicks) have lagged.

Leave A Comment