So what do you do when your John Deere and your entire business revolves around selling really expensive equipment to farmers who have been absolutely decimated financially by low crop prices and can no longer convince commercial banks that they’re worthy of additional debt needed to buy fancy new tractors?Well, you take some plays from the automotive industry, that’s what. Here’s how it works:

Step 1: Setup a captive financing arm to underwrite all of the credit risk that no reasonable commercial ag bank would touch with a 10 foot pole.

Step 2: Boost your tractor sales volumes by financing every farmer who walks through your door with a soybean dream and pulse.

Step 3:When you run out of farmers willing to buy your brand new shiny green tractors then just start selling all your production volume to yourself and then lease it to customers at an attractive price.This way you can still show sales growth and never have to cut production volume.

Step 4: Finally, when it all goes horribly wrong because used tractor prices crash due to the flood of off-lease volume and brings down the new market with it then you take a one-time charge to write-off the losses, wall streets forgives you...it was just a 1x charge, right…and then you promptly rinse and repeat.

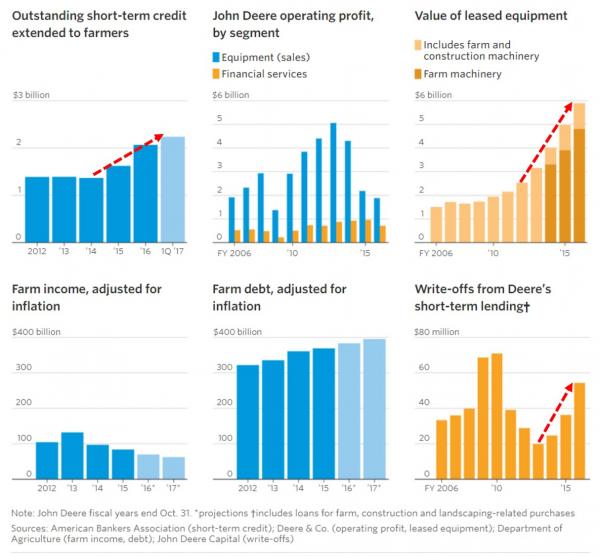

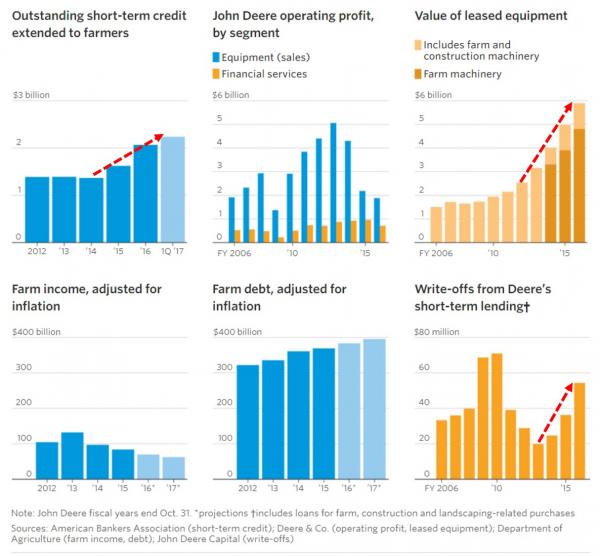

From the looks of the charts below, we’d say John Deere is currently on the tail end of ‘Step 3’ as loan and lease balances are soaring and write-offs are just starting to spike.

As the Wall Street Journal points out today, John Deere has literally become the 5th largest agricultural lender in the country behind commercial banks Wells Fargo, Rabobank, Bank of the West and Bank of America, according to the American Bankers Association. But it’s not just equipment financing risk the John Deere is underwriting these days as they’ve also started financing short-term working capital loans to help farmers buy everything from seed to chemicals and fertilizers and equipment spares.

Leave A Comment