Introduction

I know very little about blockchains (BC), distributed ledger systems, and crypto-currencies such as Bitcoin. But I am a bit dumbfounded by the claims of what “the BC era” will bring. In what follows, I comment on some of these claims appearing in a paper written by Don and Alex Tapscott in the MIT Sloan Management Review. Quotes from the article start with BC. The lead-in to my comments is EM.

A Little Background

BC: For the last century, academics and business leaders have been shaping the practice of modern management. The main theories, tenets, and behaviors have enabled managers to build corporations, which have largely been hierarchical, insular, and vertically integrated. However, we believe that the technology underlying digital currencies such as Bitcoin — technology commonly known as blockchain — will have profound effects on the nature of companies: how they are funded and managed, how they create value, and how they perform basic functions such as marketing, accounting, and incentivizing people….

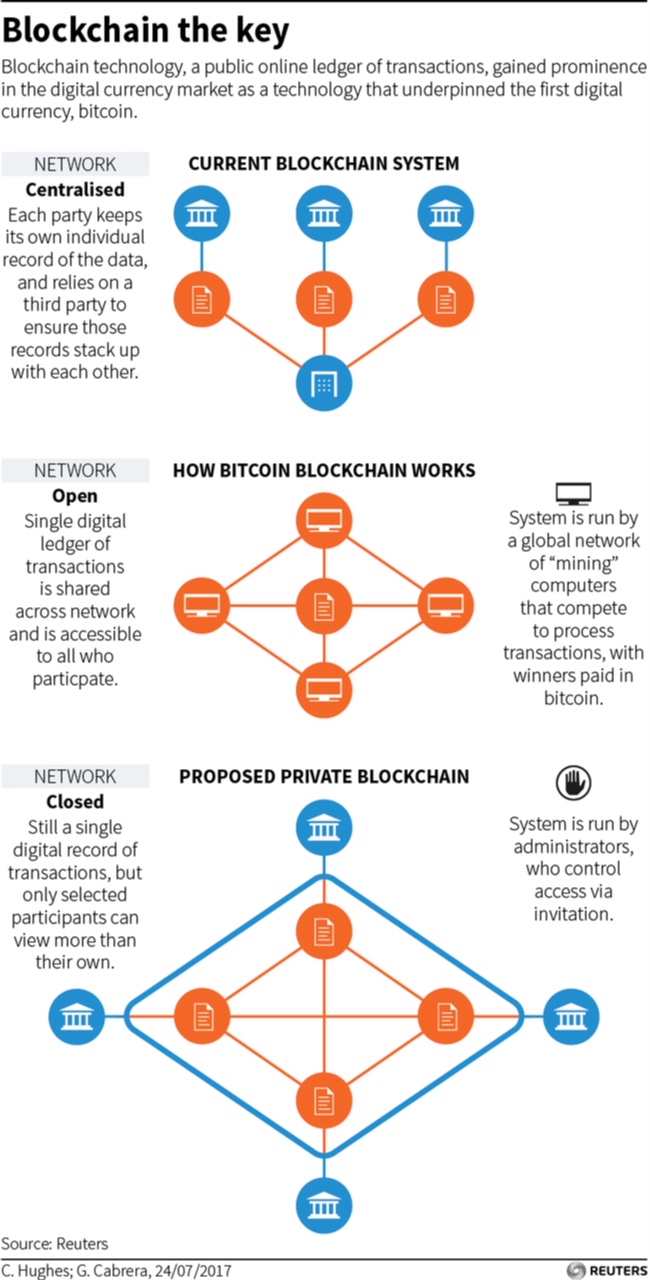

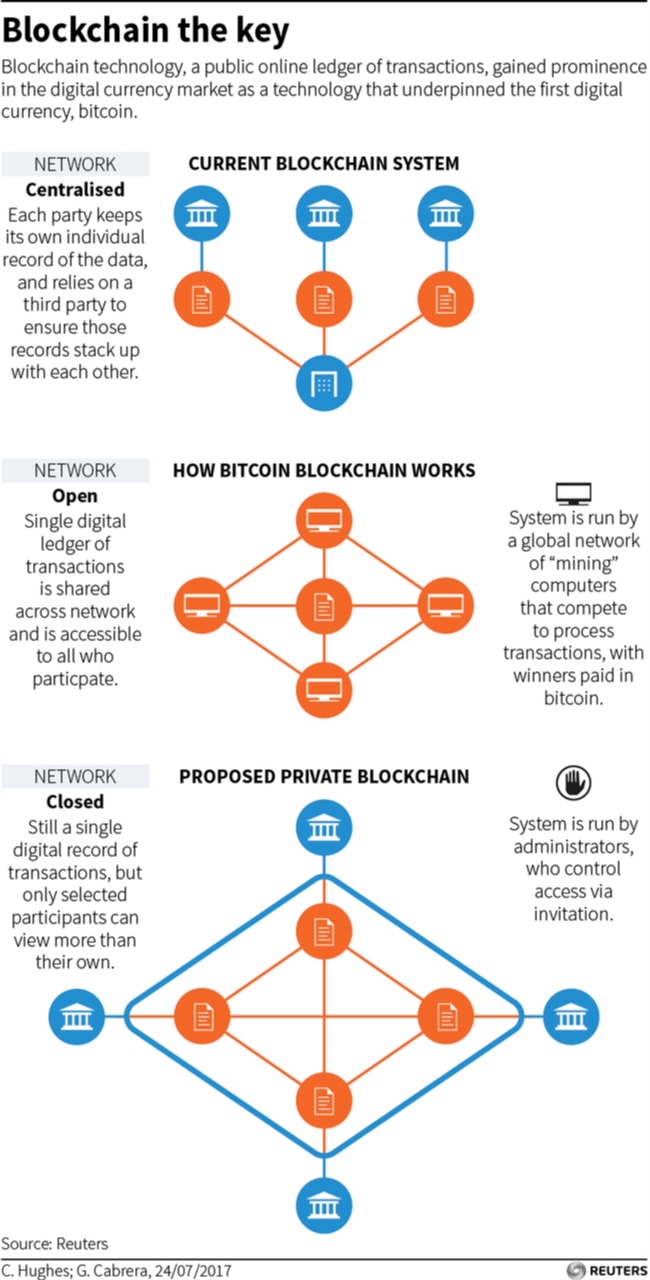

EM: It sounds interesting. Here is another piece on the same topic. For those who learn from images, this picture might help.

BC: In some cases, software will eliminate the need for many management functions….”

EM: Yes. And indeed, I have written (and worry) about the labor saving automation occurring in most goods and services industries. The macro effect has been to reduce the demand for laborers and wages globally. But automation is running apace and I am not sure how BC will affect what is already happening.

BC: The internet vastly improved the flow of data within and between organizations, but the effect on how we do business has been more limited. That’s because the internet was designed to move information — not value — from person to person. When you email a document, photograph, or audio file, for example, you aren’t sending the original — you’re sending a copy. Anyone can copy and change it. In many cases, it’s legal and advantageous to share copies.

By contrast, if you want to expedite a business transaction, emailing money directly to someone is not an option — not only because copying money is illegal but also because you can’t be 100% certain the recipient is the person he says he is. As a result, we use intermediaries to establish trust and maintain integrity. Banks, governments, and in some cases big technology companies have the ability to confirm identities so that we can transfer assets; the intermediaries settle transactions and keep records. For the most part, intermediaries do an adequate job, with some notable exceptions. One concern is that they use servers that are vulnerable to crashes, fraud, and hacks. Another is that they often charge fees — for example, to wire money overseas. They also monitor customer behavior and collect data, and they exclude the hundreds of millions of people who can’t qualify for a bank account. And sometimes, they make terrible mistakes, as the 2008 financial crisis made evident.”

EM: All true. And yes, there are currently transactions fees associated with moving any asset. And yes, more digitalization will probably lead to these fees being reduced. But just how BC will make us safer beyond what is already happening is not clear.

Leave A Comment