Here we go again…

Since June of 2013, I have been writing about the reasons why rates can’t rise much and why calls for the end of the “bond bull market” remain wrong.

Regardless, about every 3-months or so, there is a tick up in rates and you can almost bet that soon thereafter will be a litany of articles explaining why THIS time the “bond bull market” is really dead. For example, just from this past week:

- Great Ready For The Great Bond Bust Of 2020

- The Great Bond Bull Market May Be Coming To An End

- 700 Years Of Bond Data Forewarn Of Rapid Reversal From Low Interest Rates

What is the argument from low rates will rise?

It basically boils down to simply this – rates are so low they MUST go up.

The problem, however, is that interest rates are vastly different than equities. When people go to make a purchase on credit, borrow money for a house, or get a loan for a new car, they don’t ask what the level of the stock market is but rather “how much will this cost me?” The differentiator between making a purchase, or not, is based on the simple outcome of the interest rate effect on the loan payment. If interest rates rise too much, consumption stalls, and along with it economic growth, causing rates to go lower. If economic demand is robust, rates rise to meet the demand for credit.

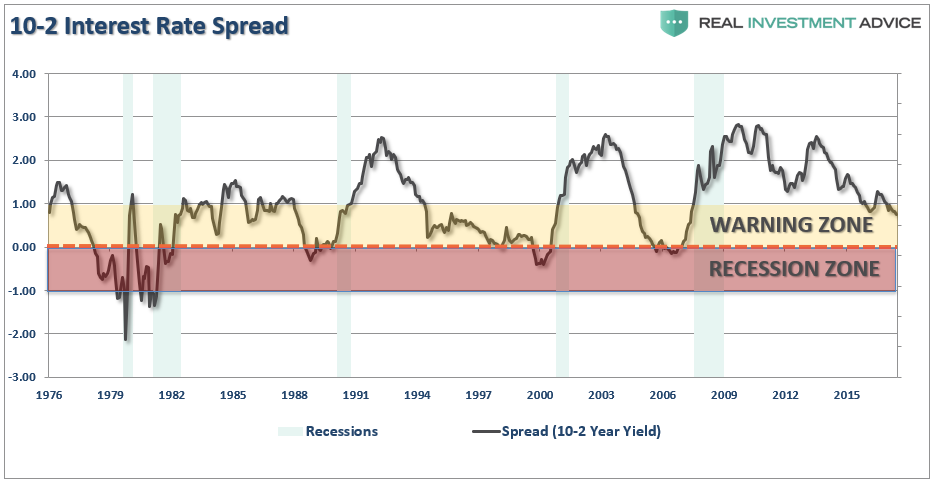

The trend and level of interests are the singular best indicator of economic activity. As Doug Kass recently noted:

“The spread between the two- and ten-year U.S. notes has fallen to 68 basis points — that’s the lowest print in ten years and if history is a guide it is signaling a potential domestic economic slowdown.”

“The flattening in the yield curve is happening despite a likely continued Federal Reserve tightening and a rise back to December levels for overnight index swaps (OIS). It was back in 2004 — as the Fed started its tightening cycle (that concluded in Summer, 2006) — that both the curve flattened and the five year OIS rose. At the conclusion of the tightening in the middle of 2006, a deep recession followed by about fifteen to eighteen months later.”

In other words, “It’s the economy, stupid.”

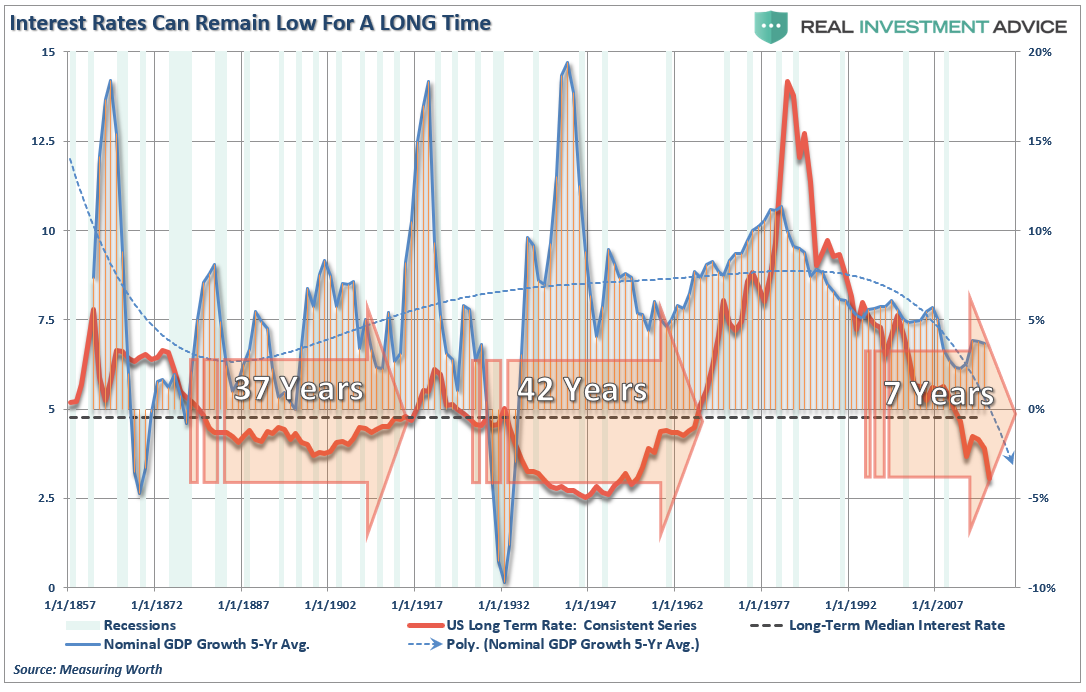

Economic Growth Drives Rates

The chart below is a history of long-term interest rates going back to 1857. The dashed black line is the median interest rate during the entire period. I have compared it to the 5-year nominal GDP growth rate during the same period.

(Note: As shown, interest rates can remain low for a VERY long time.)

Interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. There have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy.

Leave A Comment