“Vanity of vanities, saith the Preacher, vanity of vanities; all is vanity.”

– Ecclesiastes 1:2, King James Version (attributed to King Solomon in his old age)

This week’s letter will take a look at the growing number of ridiculous, inane, and otherwise nonsensical absurdities that fill the daily economic headlines. I have gone from the occasional smile to scratching my head now and then to “WTF” moments several times a week.

Wondering if it was just me, I recently sent an appeal to a what became a large number of my friends and fellow writers and analysts, asking for their graphic examples of this paranormal economic activity. Suffice to say, it is not just me who sees absurdities. I received so many responses that I may have to extend this letter another week or two. (Note: This letter will print long, as there are lots of graphs.)

Some of what you’ll see depicted in the following charts originated a decade ago in the Global Financial Crisis – or was caused by the reactions of central bankers to that crisis. The many shocking, previously unimaginable acts by central banks and governments left us so numb that I think we started to simply accept them without much thought. That was our mistake: We must confront the unthinkable, not just shrug our shoulders at it. Because when we have our next crisis, I will bet you dollars to donuts that central banks and governments will react in ways that are even more unthinkable.

Before we get our thinking caps on, let me remind you that early registration is now open for my next Strategic Investment Conference. The dates are March 6-9, 2018, at the Manchester Grand Hyatt in San Diego. We’ll have a wonderful time with an all-star cast including Jeffrey Gundlach, Mark Yusko, John Burbank, Niall Ferguson, and George Gilder. I’m in negotiations with other well-known names, too.

Now on to the bonfire.

Vanity of Vanities

If you work in the financial industry you’ve probably read, or at least know plenty about, the Tom Wolfe novel Bonfire of the Vanities. It’s a great book, but it’s not the source of this letter’s headline. I’m thinking back further to the original “bonfire of the vanities” in fifteenth-century Florence.

In 1490 the ruling Medici family brought in Dominican friar Girolamo Savonarola to serve them, but within a few years he was more or less ruling the city. In 1495, during the pre-Lenten carnival, Savonarola began hosting a “bonfire of the vanities,” at which people would burn objects that inspired the deadly sin of vanity: mirrors, cosmetics, musical instruments, and so on. This being Florence, they also destroyed tons of artworks, tapestries, books, furniture, and other priceless treasures. Did doing so make them any less vain? Probably not, but I’m sure the bonfires were quite magnificent.

In a similar manner, we in this century routinely “burn” hard-won lessons (or at least expel them from our thoughts) because someone with an ulterior motive convinces us they’re useless or harmful. That’s rarely true, as we often discern too late, and then we have to learn the same lessons again.

Think about this. How often do central bankers, regulators, corporate leaders, lawyers, politicians, and ordinary investors make the same mistakes over and over again? All the time. If we would stop burning our memories, we might make better progress. But no, we must have our bonfires. And so the absurdities are perpetuated.

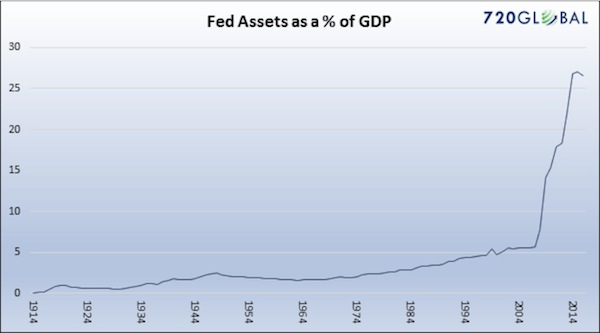

To kick off our tour of absurdities, Michael Lebowitz of 720 Global sends this chart of Federal Reserve assets as a percentage of GDP. You might notice a slight trend change along about 2008:

Not to put too fine a point on it, but this is bonkers. I understand that we were caught up in an unprecedented crisis back then, and I actually think QE1 was a reasonable and rational response; but QEs 2 and 3 were simply the Fed trying to manipulate the market. The Keynesian Fed economists who were dismissive of Reagan’s trickle-down theory still don’t appear to see the irony in the fact that they applied trickle-down monetary policy in the hope that by giving a boost to asset prices they would create wealth that would trickle down to the bottom 50% of the US population or to Main Street. It didn’t.

The Fed has left that bloated balance sheet alone for almost 10 years. And now for some reason they feel it is urgent to reduce the balance sheet even as they also raise rates. This is not model-based monetary policy; it is simply an emotional monetary policy experiment. I can understand raising rates – I wish they had done that four years ago. I can even understand reducing the balance sheet. But at the same time? When you don’t know what you don’t know? I mean really, there is no way to know how the market is going to react to either of these events, let alone to both at the same time. This seems to me the height of monetary policy lunacy.

We never share your email with third parties.

The Fed’s stimulus efforts manifested themselves, among other places, in years of near-zero interest rates, helpfully illustrated here by Peter Boockvar:

Leave A Comment