Both investors who favor momentum stocks and those who focus their portfolios around high-quality stocks have probably had a very difficult 2016 so far, but for very different reasons. As a result, it may be a good idea to include both in investment portfolios particularly in light of the macroeconomic changes that are going on right now. Fundstrat advises investors to choose value stocks to take advantage of the weakening U.S. dollar and momentum stocks to benefit from the easing credit environment.

2016 brought two different problems

Fundstrat Global Advisors analyst Thomas J. Lee and his team said general investor sentiment suggests that two problems prevail right now. Some investors reported being defensive at the beginning of the year, did well in January but then lost quite a bit of ground over the last six weeks. Others were apparently “caught in a downdraft” in January, but the February rally wasn’t enough to bring them back up to flat for the year.

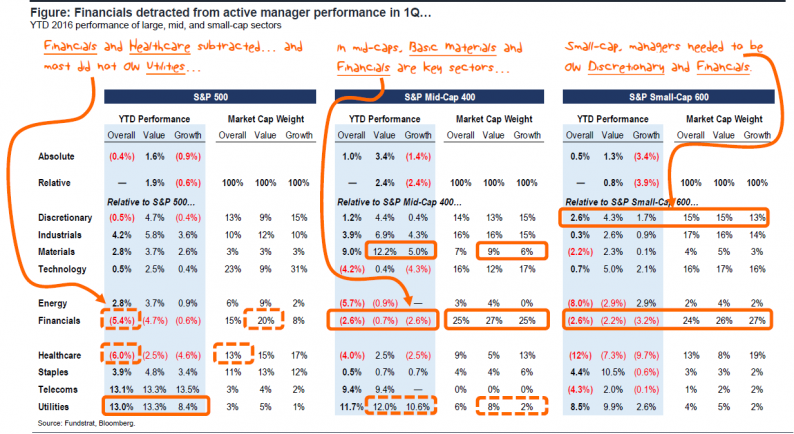

Lee said this year has brought both “divergent sector performance” like what we saw in the second half of the year and also “sector reversals that were not ‘fundamental’ based.” He noted that large-cap Healthcare and Financials stocks have underperformed but that this hasn’t been as much of a problem as the Utilities sector’s massive outperformance.

Mid-cap Basic Materials stocks have outperformed by about 900 basis points or 1,220 basis points in mid-cap value stocks. Small-cap Healthcare stocks caused the same problems as large-cap Healthcare stocks.

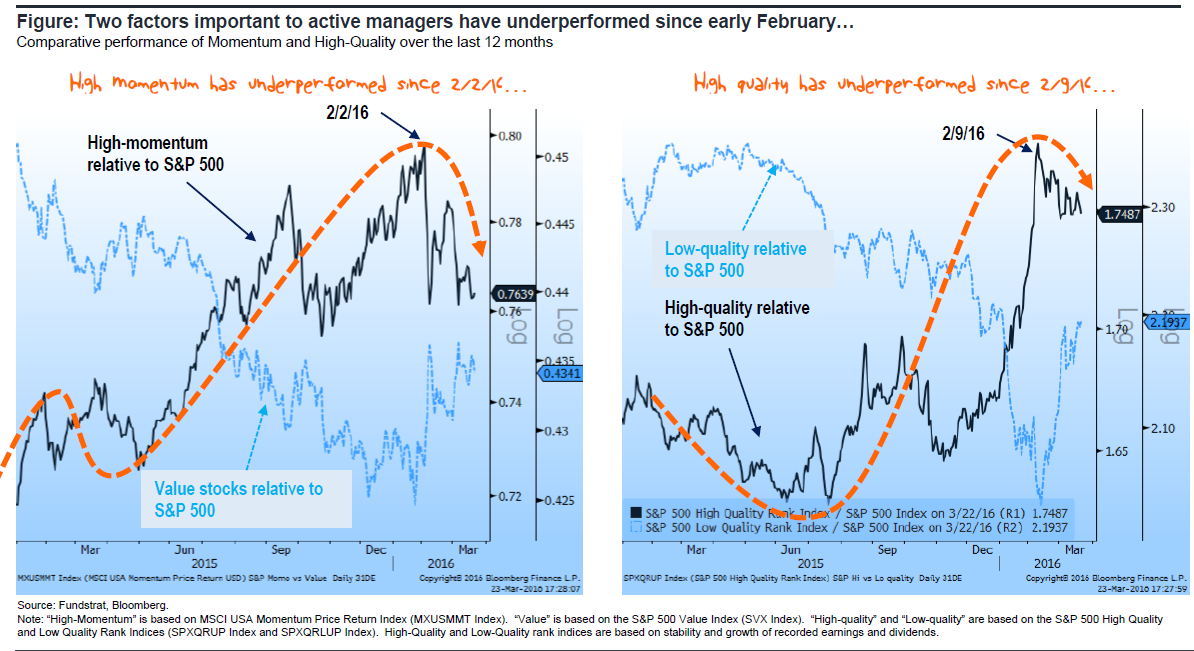

Momentum and high-quality stocks taking a toll

Lee said that currently, investors are positioned for a strong U.S. dollar and are overweight on momentum and high-quality stocks, although these stocks have been underperforming since early last month.

He thinks that most investors expect the U.S. dollar will remain where it is, although he believes it will weaken even more. The reasons given for not believing the U.S. dollar will weaken more are: “divergence of monetary policy and divergence of GDP growth rates.” However, he believes the recent currency moves can be explained by relative inflation.

Leave A Comment