I am aware of all the doomsday Yen hyper-inflationary predictions due to their soaring debt-to-GDP ratio. And these Japanese bears very well might prove correct… In the long run. But as Mr. Keynes taught us, the long-run is an awfully long time. In the meantime, I think there is a terrific opportunity in Japanese assets, and that also includes the currency.

This flies in the face of most market pundits’ forecasts. You will often hear recommendations to buy Japanese equities, but they will often be couched with warnings that it needs to be done on a “currency hedged basis.” And it’s easy to see why.

BoJ Balance Sheet Expansion

Over the past half-dozen years, the BoJ has gone fully bat-s** crazy with balance sheet expansion. It’s unprecedented in modern economic times. Yet many believe this to be the final stage in what has been two decades of insane monetary policy.

Contrary to most conventional wisdom, the BoJ’s quantitative easing programs in the late 1990’s and 2000’s was not nearly as dramatic as many pundits remember. It seemed frightening at the time, but that was because Japan was the only country stuck at the zero bound and forced to expand their balance sheet.

The moment the economy seemed ready to finally spark, the Japanese government pulled back on both the monetary and fiscal stimulus, worried that, much like an engine with the choke on, they would flood it. Well, this proved disastrous and the result was that the economic engine never fully started.

You might disagree with that assessment, so be it. It doesn’t really matter. Although it took almost two decades, eventually the Japanese people came to this conclusion and elected Prime Minister Abe, largely on his dramatic economic reform platform.

As you will notice, the BoJ is no longer making the mistake of closing the choke at the first engine turn that catches. The BoJ has taken their balance sheet from 30% in 2011 to almost 100% today.That’s an insane amount of stimulus.

So there is little wonder that most forecasters are extremely wary of being long a currency whose supply has been increased so dramatically.

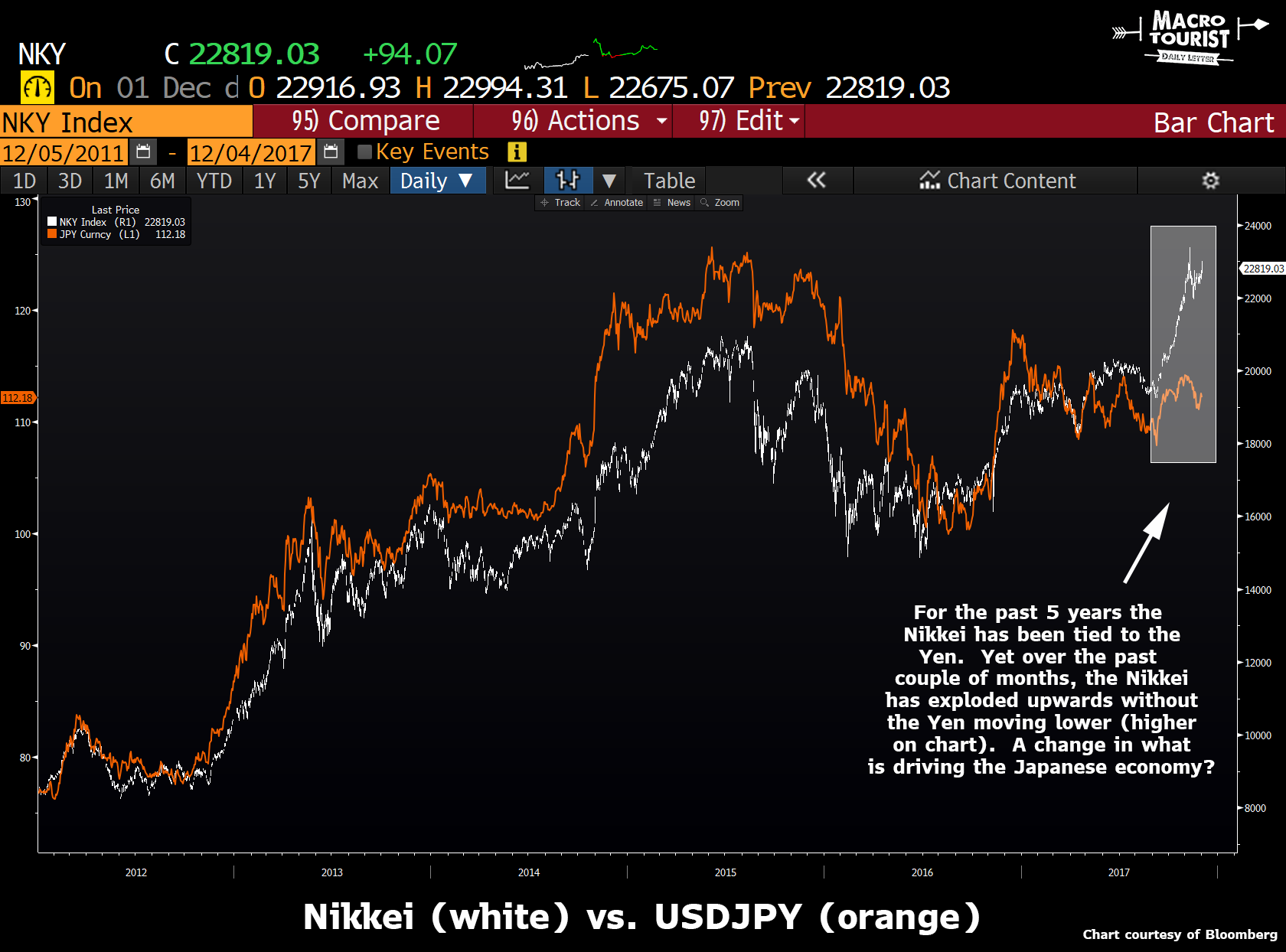

For the first couple of years of Abeconomics, the Yen did weaken. Materially. The USD/JPY rate went from 75 to 125.

And this currency devaluation drove the stock market. From 2012 until just recently, the Yen and the Nikkei traded almost tick for tick.

But look closely at the last six months. The Nikkei is running like it stole something without a corresponding decline in the Yen. Could it be that something changed?

Maybe the aggressive balance sheet expansion is behind us?

Even though the BoJ balance sheet chart looks like a one-way rocket to the moon, if you look closely at the data, it becomes apparent that the rate of change is slowing.

And it’s finally getting noticed. From the Nikkei:

TOKYO – The Bank of Japan is slowing the supply of money, arousing speculation that it is paving the way for a trimming of its ultra-easy monetary policy.

The supply of funds to the market in November showed an increase of 51.7 trillion yen ($458 billion), effectively the smallest annual pace of growth since the BOJ introduced easing of a “a different dimension” in April 2013. The central bank is steadily shifting the focus of its easing policy to controlling interest rates, away from “quantitative” measures, as prices have doggedly refused to rise.

The BOJ implemented powerful easing measures, accompanied by a few surprises, in the first half of Haruhiko Kuroda’s governorship starting in March 2013. Now, in little more than a year, the central bank has shifted to a waiting game while paying attention to financial institutions.

On Monday, Kuroda said at a Europlace financial forum in Tokyo that since changing the monetary easing framework in September 2016, there has been no change in either the BOJ’s policy or its thinking. He said the BOJ has secured financial stability, and control of the the yield curve is going well.

The BOJ had maintained yield curve control “quite effectively and efficiently without creating financial problems,” he said, adding that current levels of the BOJ’s yield targets were “quite appropriate.”

According to a plan announced at the end of November, the BOJ will continue cutting the purchase of short-term Japanese government bonds in December. An increasing number of participants in the bond market are starting to forecast that the BOJ will further reduce purchases of JGBs and raise the target rate of long-term rates from zero next year.

When the BOJ introduced its aggressive easy-money policy several years ago, Kuroda said the central bank would “double the monetary base in two years,” making the monetary base the target of easing measures.

The BOJ supplies funds to the market through such means as issuing banknotes and buying government bonds. Japan’s monetary base – the total amount of money supplied by the BOJ – exceeds 470 trillion yen, up more than threefold over the past five years.

But growth of the money supply has been slowing sharply. While the BOJ supplied money at roughly an annual pace of 80 trillion yen last year, the pace began slowing by stages at the start of this year. In November, it came to 51.7 trillion, the smallest amount in four years, as the easing policy was held in check in its initial stages in April-July 2013.

Leave A Comment