Because they are key to our macro fundamental road map going forward, we continue to watch the ‘gold vs.’ theme very closely. These are like credit spreads, only they have nothing to do with bonds and everything to do with the future direction of macro markets.

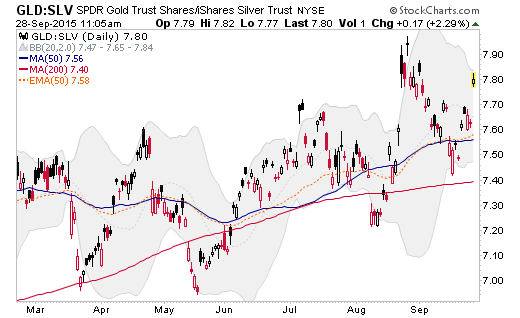

Gold vs. Silver is taking the post-consolidation ‘next leg higher’ we have been expecting. Next up are the targets for the Gold-Silver Ratio of ‘low 80’s to 90’, accompanied by plenty of macro market stress.

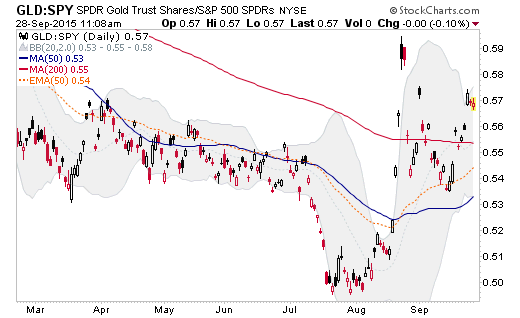

Gold vs. US Stock Market (SPY) is still constructive. Dear gold bugs, constructive means constructive, not bullish. Not quite yet. If it goes bullish then an important holdout in the gold mining macro fundamental case would come in line as conventional investors would be compelled to pay more attention to the sector.

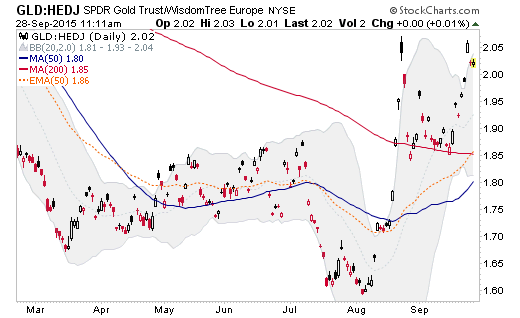

Gold vs. European Stock Markets (Euro-hedged HEDJ) is similar, but a little further along.

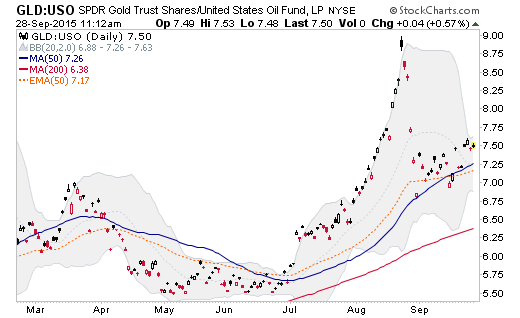

Gold vs. Crude Oil (USO) continues to look constructive for another up-turn as it rests above the 50 day moving averages. This is obviously a sector fundamental consideration for fuel-intensive mining operations.

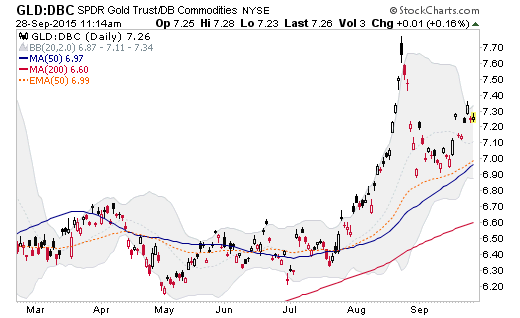

Gold vs. Commodities (DBC) is also constructive, and was the earliest signal we had on negative changes coming to global macro markets as it made its initial bullish move back in 2014.

Leave A Comment