The saying goes “birds of a feather flock together.” With the news that Valeant (VRX) had named Joseph Papa, its new CEO, we began to analyze just what Valeant was getting. Through this analysis, we found that Perrigo Company (PRGO: $97/share), the firm Mr. Papa is leaving behind, exhibits many similarities to Valeant, including misleading non-GAAP measurements, aggressive, shareholder destructive acquisitions, and executive compensation misaligned with shareholders’ interests. Perrigo is in the Danger Zone.

History of Success Wiped Out In A Few Short Years

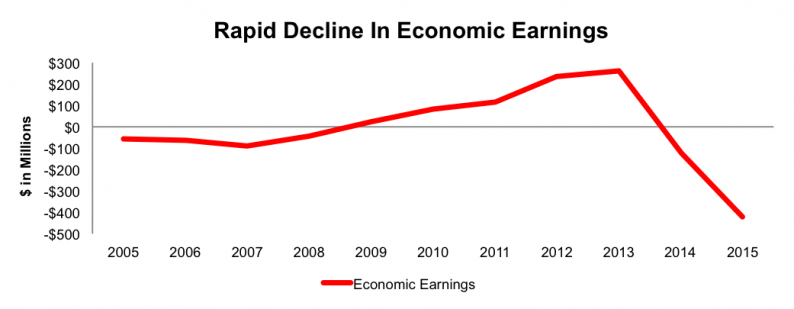

Many years of good decisions can be wiped out by one bad one, and Perrigo’s leadership made many bad decisions. We won’t debate the history of success from 1998-2012. Perrigo grew economic earnings, the true cash flows of business, from -$597 in 1998, to $232 million in 2012. The problems started when Perrigo began engaging in financial engineering, including “accretive acquisitions” and its 2013 tax inversion through the acquisition of Elan. Since 2013, Perrigo’s economic earnings have declined from $259 million to -$421 million, as per Figure 1. See the reconciliation of Perrigo’s GAAP net income to economic earnings here.

Figure 1: Economic Earnings Drastically Falls

Sources: New Constructs, LLC and company filings

This decline in economic earnings mirrors Perrigo’s return on invested capital (ROIC), which has fallen from 14% in 2012 to a bottom-quintile 4% in 2015.

Further compounding the issues, Perrigo has greatly increased debt and diluted shareholders over this time frame. From 2012-2015, Perrigo’s debt increased 55% compounded annually to $5.6 billion. Its shares outstanding grew from 93 million to 146 million, or 16% compounded annually from 2012-2015. Perrigo funded its acquisition-based growth at the expense of shareholders.

Non-GAAP Metrics Paint A False Reality

Investors listening only to Perrigo management’s focus on non-GAAP earnings would have a vastly different view of the company than those of us looking through to the underlying economics of the business. The fall of Valeant makes the non-GAAP measurements clear. Here are the expenses Perrigo removes to calculate its non-GAAP net income:

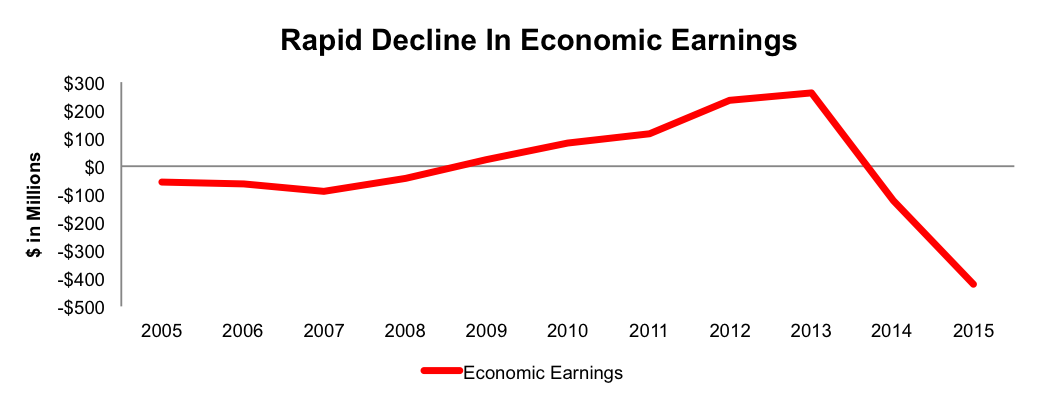

In 2015, Perrigo’s non-GAAP net income was a staggering $981 million, compared to $128 million GAAP net income and -$421 million economic earnings. Figure 2 shows the discrepancies between GAAP, non-GAAP, and economic earnings

Figure 2: Perrigo’s Non-GAAP Is Nonsense

Sources: New Constructs, LLC and company filings

Executives Were Incentivized To Destroy Shareholder Value

The cause of the shareholder destructive behavior is the company’s executive compensation misaligned with shareholders’ interests plan. Perrigo bases executives’ short-term incentive pay on non-GAAP operating income, adjusted to remove standard operating expenses as detailed above. Through this plan, executives are incentivized to grow revenue through any means, while ignoring the cash flow impact of their actions.

The misalignment of incentives at Perrigo proved particularly damaging to shareholders in 2015 in a series of events that mimicked the disaster for Men’s Wearhouse investors that resulted from the Jos. A Bank acquisition (see special report). In 2015, Mylan (MYL) launched a takeover bid for Perrigo, which valued PRGO at $26 billion. Perrigo spent nearly $87 million to fight off the takeover and claimed the deal was not in the best interests of its shareholders. Today, PRGO has a market cap of $14 billion. Shareholders ended up $12 billion poorer, but guess who got richer? After fighting off this takeover, executives were rewarded for “their key contributions related to Mylan’s takeover attempt. In total, executives received $3.5 million in bonuses while investors lost $12 billion.

Leave A Comment