It’s been a while since I have posted, so I will ease in with a short and simple one.

When talking to credit managers, I always ask for names that they are avoiding. More times than not, one of the companies mentioned is Deutsche Bank. Credit managers either feel it is too complex to value, or they do not trust the markings of the smorgasboard of derivatives that decades of unrestrained capital market share growth has brought.

After all, we are talking about the firm audacious enough to buy Bankers Trust. I am old enough to remember when Bankers was the firm when it came to complex derivative products.

Yet with this superstar status came a very aggressive trading culture.

Who can forget forget BT pillaging P&G in the infamous ‘wet dream’ trade?

Do you really think this ‘ROF’ (rip-off factor) wouldn’t also be aimed against the firm as well?

Back then traders were paid up front for derivative trades that would sometimes be on the book for years and even decades to come. Deutsche Bank was more willing than many other Wall Street firms to allow these sorts of trades to garner market share – but I sure wouldn’t want to be the one managing that risk for the life of the product.

And I shouldn’t blame it all on BT. Deutsche Bank got into a fair amount of trouble on their own during the 2008 credit crisis. Although Ryan Gosling was smart enough to get short the housing sector, there were plenty of other Deutsche Bank employees that were long out the hoop.

All in all, Deutsche Bank has typically been an overleveraged, difficult to value, aggressive global bank that seems to only participate in the negative portions of each region’s fate.

So it is with little surprise that the current European economic struggle is affecting DB more than the other global banks.

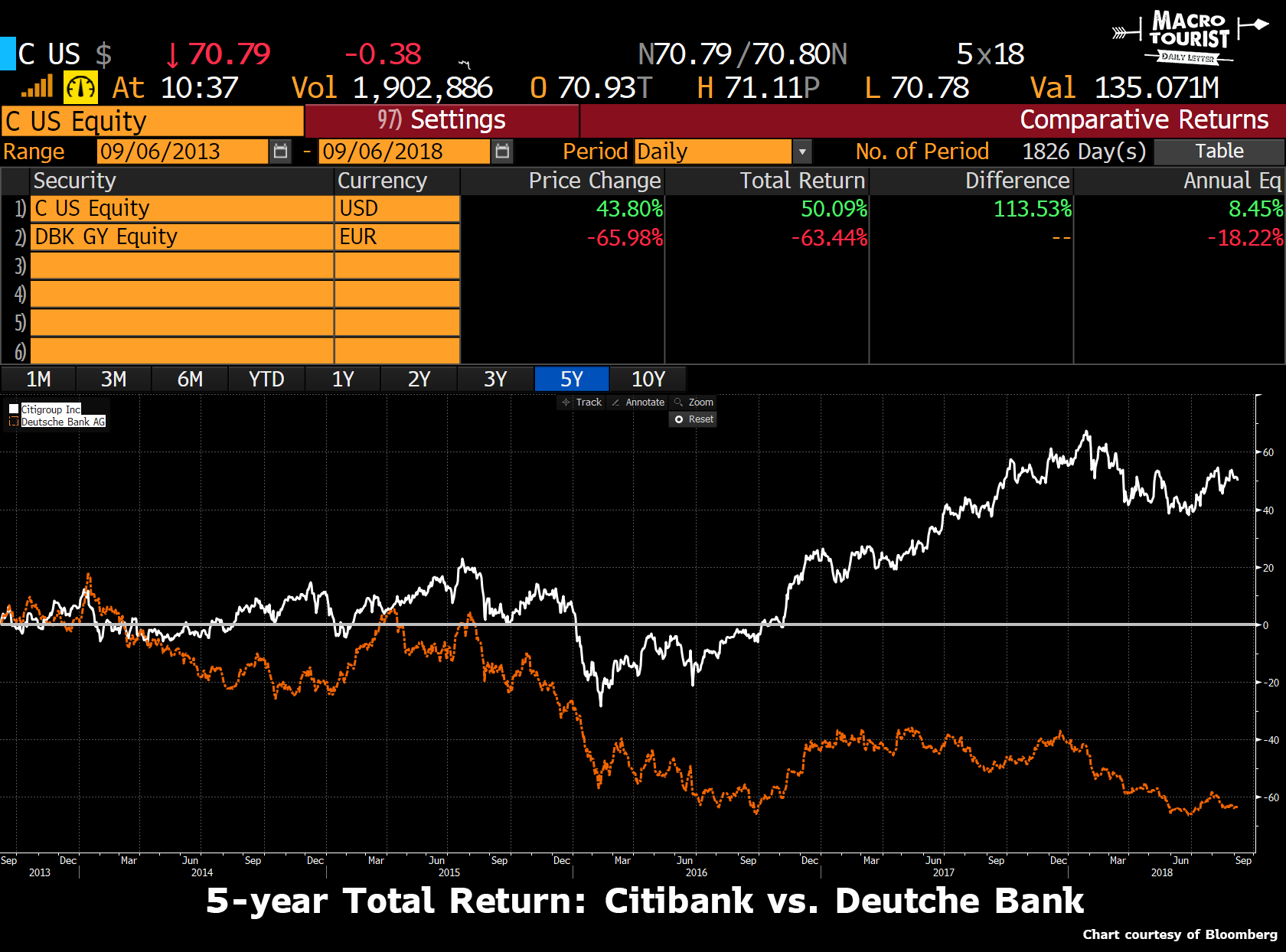

Let’s look at the US “DB-equivalent” Citibank over the past five years:

Citibank has managed to eke out almost an 8.50% annualized return while Deutche Bank was negative 18% with a total loss of 66%.

Leave A Comment