Two articles in the last two days, one on Bloomberg, the other on the Wall Street Journal, provided key reasons we should not worry about stock market bubbles.

It’s Only 1997

Bloomberg explains In Dot-Com Bubble Time, It’s Still Only 1997 for U.S. Equities.

“Terrified that rallies in Facebook Inc., Amazon.com Inc. and Google portend a millennial catastrophe along the lines of the dot-com bust? Relax. Going by one doomsday clock, it’s only 1997 in bubble years … when there was still 2 1/2 years and 60 percent to go in what became the longest bull market on record.”

It’s Different This Time

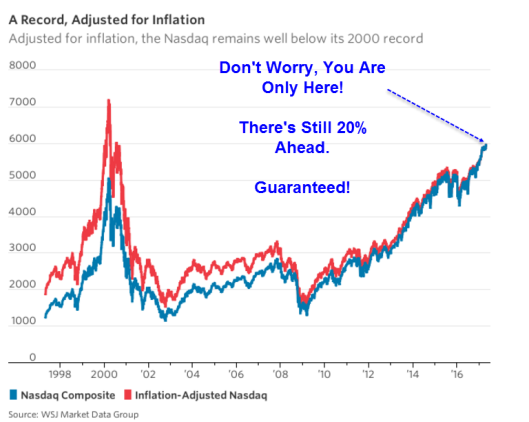

The Wall Street Journal says This Time Is Different: Two Reasons Not to Be Alarmed by the Nasdaq Record.

The Nasdaq Composite crossed the 6000 mark on Tuesday morning, setting another record in a year that is already a hot one for the index, and further putting the old dot-com days in the rear-view mirror. But there are at least two notable old records it has not yet surpassed. One is a measure of how far the index still has to go, the other is a mark nobody really wants to see again.

1. Inflation-adjusted Nasdaq. Adjusted for inflation, the Nasdaq Composite still has not broken its record high, fully 17 years after that peak, according to data from the Journal’s Market Data Group.

2. Price-to-earnings ratio. The dot-com boom was such a spectacular feeding frenzy that by one measure of valuation, the Nasdaq Composite is not even at 40% of its peak.

The companies in the index collectively traded at 27.5 times their last 12 months of earnings, according to Thomson DataStream.

Don’t Worry, You Are Only Here.

Shiller P/E Ratio

Base image: Shiller PE Ratio

While waiting for that final 20% (and why should it stop there?) relax. Repeat after me: It’s not bubbly, it’s Bubblicious. Enjoy the ride.

Leave A Comment