Denny’s (DENN) is one of our favorite places to eat with the kids on a weekend morning, or after a long night out with friends. This is a diner-style restaurant, featuring a relatively low-cost menu which features breakfast all day. While the performance of the stock has been strong, we feel shares are a bit expensive here. It is out thesis that shares are presently overvalued. In this column, we will discuss recent performance, as well as offer our projections for 2018, relative to the valuation of the stock.

Price action and valuation

Take a look at the price of Denny’s stock in the last year:

Source: SEC filings

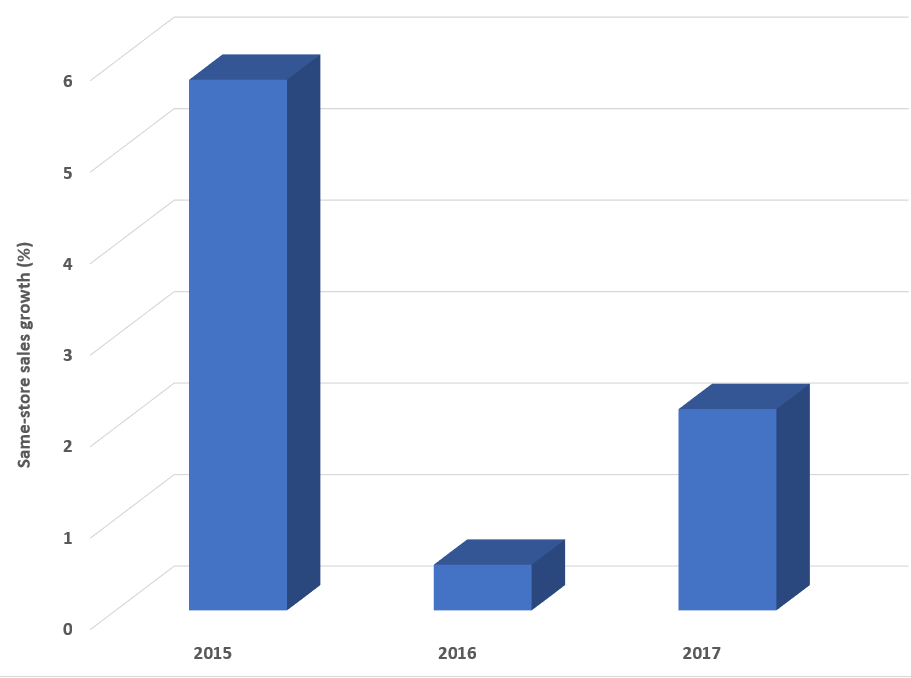

As you can see, shares have risen to a near 52-week high. At $15.10 per share, this puts the stock at 27 times trailing earnings, priced well above the sector average of 21, which suggests the name is baking in continued growth. To justify this price, we want to see strong revenue growth, continued mid-single digit comparable sales growth, and most importantly significant earnings per share growth. Let us discuss.

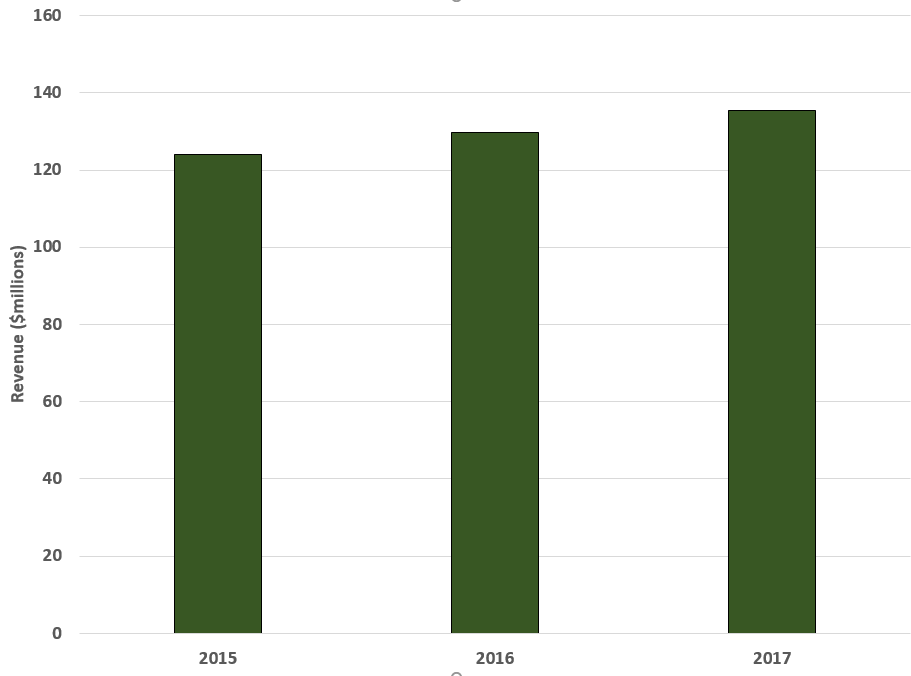

Sales growth slightly below expectations

We saw total Q4 operating revenue grow a respectable 4.5% to $135.5 million, continuing a trend of rising sales:

Source: SEC filings

The main problem we have here is not so much the pace of sales growth, but the fact that it was $1.2 million below our target of $136.7 million. We were admittedly more bullish than the Street consensus of $135.8 million. In either event, sales were below expectations.

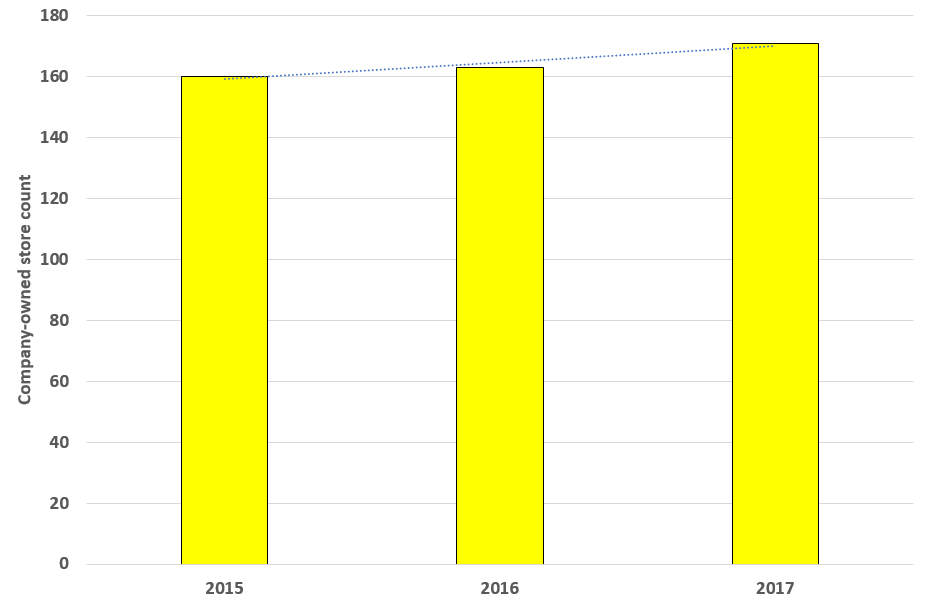

What went into these sales figures?

The 4.5% growth stemmed primarily from a strong performance in company-owned restaurant sales. Company-owned restaurant sales were up 6.0% to $100.3 million, primarily due to a greater number of company restaurants compared to the prior year quarter, and same-store sales growth in Q4:

Source: SEC filings

Source: SEC filings

Leave A Comment