Meanderings about a zombie economy… that’s what dominated the questioning around Chair Yellen’s first-phase of 2-day testimony; including whether implementing a NIRP (Negative Interest Rate Policy) is questionable based on legalities. That’s not what they should focus on; rather the implications we discussed last night, and only lightly alluded-to by the Committee (Yellen or the Congressmen) or for the most part ‘skirted’. That’s because they NIRP would be a deleterious tactic.

Chair Yellen tried to walk a careful line (particularly the pre-release remarks), as sparked the early rally we suspected before a post-testimony part 1 decline also alluded to both with respect to the intraday pattern and the idea of fading the first move. As the 2nd video delves into much of what happened, as well as the backdrop we have outlined consistently (technically and fundamentally); I’m not going to dwell on extensive text tonight, since you know our overall view as well as the need to focus on the videos more so than the text presented here.

I am going to note a few key points: 1) a short-term indecision pattern to allow the S&P to lift off daily oversold was logical, and one never wants to short as a trader, in-front of a Fed Chairman’s testimony (heck with political correctness; a Chair can be a Chairman or Chairwoman; who cares who you describe it); 2) a way of describing policy DOES matter, and she did a horrible job by essentially inadvertently acknowledging they’ve talked about NIRP since 2010 (really that means all -and I really mean all- the domestic and international analysts that of course relied either on central bank (or Goldman?) optimistic presumptions that flew in the face of the Fed’s own data for many months or longer, are either just besides themselves (not knowing what to do or how to handle portfolios) now; or they are compelled to admit they relied on antiquated long-term strategies as were obliterated (or are still in that process) by the prolonged contraction; or 3) the impact of QE and low rates that allowed the ‘dangerous’ disconnect from all economic reality for the majority of the population as we’ve said for over a year and which indirectly contributes to the rise of ‘populism’ (on the left or the right) both here in the U.S., and in Europe too.

Typical me: I start with a few points; then keep going. Hah! Stop typing Gene.

If they do this (NIRP) we will get not just a ‘recession’, but they won’t have lots of weapons to use to maintain the ‘controlled’ Depression as I’ve termed overall has been under the facade of the previously-extended upside in financial asset sectors; not the all-important Average Household Income or Growth levels. It’s becoming political, but was never meant that way from my perspective. Now it’s manifest itself in both leading candidates (of the moment anyway) which proves my point, ironically enough: that regular people are pretty fed-up with things.

The risk is that this might ‘feed upon itself’, and now become a self-fulfilling sort of prophecy. To wit: add a crashing stock market (and softer housing prices) as well as an imploding auto industry; and will the Fed and pundits simply sit and ponder why ‘free’ loans aren’t stimulating purchases? Or will they wake-up and smell the coffee and realize that people finally get it that government is trying to push them into spending; push equity prices back-up by charging for saving; as well as do nothing that actually encourages CapEx or corporate hiring?

In sum: rather than a polarized society that they claim exists (you have that in Congress not in the public) you now have a society that is tired of divisiveness or realizes that the policies have been counterproductive for everyone (including the so-called 1% elites, which is becoming a shopworn term at this point), with a market drop that is absolutely hurting the investor class (essentially that didn’t heed warning signs we’ve shared for so long).

Not crowing; I’m concerned that things globally are far along in the course of deterioration; not much officials can really do shorter-term; and on-top of it the global geopolitical picture threatens to get out-of-hand even further this Spring and Summer. (North Korea just executed its Army Chief; the Russian Air Force is now essentially carpet-bombing Western Syria, while Turkey threatens not only to join Saudi Arabia in an intervention; but openly hurls ire at the USA for helping the Kurds, one of the few proper forces actually fighting ISIS etc.)

Even legendary credit gurus (I’ll prefer not to name them though most of you know at least three that this would apply to) are now saying we’re heading toward, or ‘might’ be ‘in’ a recession. No kidding. We track it since last July (said so ever since); if right that makes us the optimists, because based on duration it would end far sooner than the historical measure from some suggesting it’s just upon us. Of course with the challenges out there, if they throw NIRP in too; it will be deeper than the average duration.

Bottom-line: there is no bottom-line. At least with respect to downside targets. Puns aside; we’ll listen to the messages of the market as time evolves, and try to assess when it makes sense to consider accumulation. This has been a very successful time for us from a trading standpoint, as well as for investors able to avoid temptation and stay out (or lighten up) for over a year now on rallies. But at the same time we have empathy for the others, rather than being tempted to cast aspersions; it’s sort of like wishing things weren’t as bleak as we feared for the Nation, or much of the world.

We’ll keep our chin up of course; and suggest the same for everyone. Maybe it should be thought of this way: if this is the mood from having nailed this market; I can’t even imagine the sentiments from those who are remain bullish or buried in un-salvageable heavy long positions; those who keep catching falling knives; or even worse; longs that have margin or leveraged positions during even far worse than the market (I’ve warned against margin and the compounded risks for some time too).

In any event, maybe I just sense this as a spot where there was a spot for the stock market to rebound ‘within the context of a bear market downtrend’, and it tried, but then the Fed Chair shot it down with everything but a full confession. Yellen’s efforts to reflect a calm personna, with a bit of candor, screamed lots of sobriety to a market, and helped it accelerate a reversal from the early spike; a turn from up-to-down suggested in our first video of the morning. Now, before it is said ‘oh good’; I would have preferred that the market put on more of a show as far as rebounds even if I had been wrong about that turn.

Why? Because it would have eased the oversold technical condition a bit more. Of course ‘crashes’ only occur from oversold; and this era is a ‘process’ kind of evolution. That’s why the VIX is still sub-30 and why the S&P isn’t deep into the 1700’s yet. Stay tuned; there’s more to come.

Conclusion: holding short March E-mini / S&P from the 2065 level.

Daily action – my ‘brief’ remarks sort of covered it. So do the videos. Market of course faltered and reversed today, multiple times, traversing hundreds of Dow points in both directions. This reflects a lack of liquidity and very treacherous or thin market conditions. Oil prices trying to rally and then reverse didn’t help. A story about Iran and Saudi Arabia agreeing to talk about stabilizing Oil prices at one point helped; though hard to believe at the moment; though financials say they both would benefit, so you never know (we’re all in-favor of higher Oil).

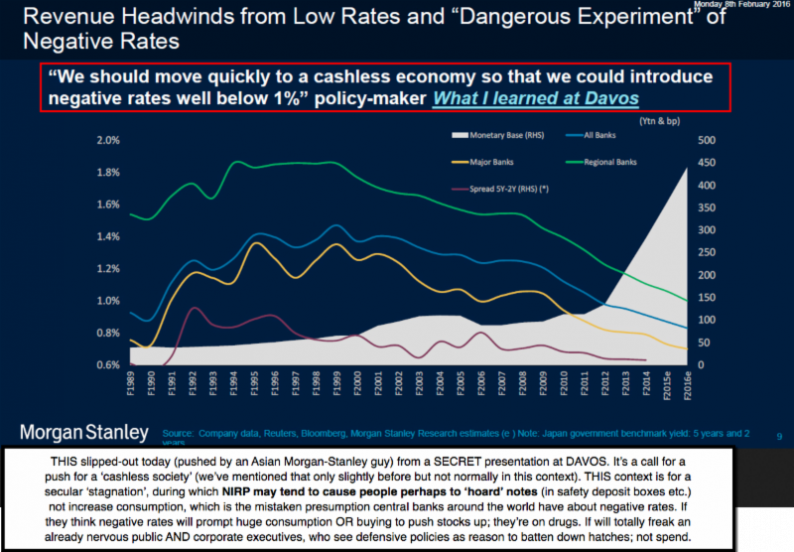

This evening Tokyo is down yet-again; and while I think the focus today finally bringing NIRP out into the open is welcomed (analytically); perhaps the legality discussion was ‘cover’ for the real aspect, which is the ‘stupidity’ of using NIRP, which can be gleaned from what happened in Japan (think no ability to float the bond issues necessary to run a society that’s build on debt and not surplus and you cut to the chase). So I think they’ll not do it; but meanwhile here they scare people; and that can scare markets, even without implementing such a policy.

And sure; realization that both present candidates are Wall Street nightmare fodder, is and will have more impact on the market; which wants to resurrect the old game (I have said for over a year that they would be unhappy when the ‘punch-bowl’ was taken-away and return to the well even after ‘last call’. Yup.)

As to the ‘no more cash crowd’; well that (sparked by NIRP fears) could be the over-reach that finally wakes some people up; and prevents it from occurring. It is not about left or right; it’s about common sense and a halt to the insanity. And there’s no way a cashless society works without a slave labor world. Otherwise, people move to barter or an underground economy in which even state & local government participate in. This would likely backfire on politicians or globalists, or central bankers, who advocate it. If their control grid starts fraying (already is to a degree), it can unravel further (in some countries like China maybe totally), and there you have an actual revolution risk; not a political one like here.

I still fear the timidity we’ve shown on the global stage has had an unintended series of outcomes (to say they’re intended would be to accuse leadership not of naivete, but of something more sinister); which have yet to gel to main event status. Symbolism might matter. Not one media outlet I’ve heard of makes the point of where tomorrow’s (some say last-ditch) key meeting of the U.S., UK, France, Russia, Iran, Saudi and Syria (and others) to try to save the Middle East from conflagration takes place: MUNICH.

We could again challenge the January lows as soon as after Yellen’s Phase 2 testimony; as she has ‘a chance’ to right-the-ship by negating the ‘impressions’ her comments on NIRP and recovery gave the market on Wednesday. Can we hope that her staff has enlightened her of the necessity to tone that down a lot?

Prior highlights follow:

Leave A Comment