Secular shift ramifications start in Japan (as exports gravitated to other nations) resulting in competitive devaluations, and excessive stimulus by central bankers trying to stem the tide, with the outcome being a race to the bottom that is sadly by no means ended.

As excited as I am about new technologies (including autonomous cars, though I have no intention of driving a fully-automated model that may be to autos what over-controlling computers were to earlier Airbus airliners, with disastrous results), I question whether volume consumption levels exist for now. That’s a problem that vexes all manufacturers and exports; will buyers actually show up?

Since the ‘Epic Debacle’ there has been a ‘consumer cocooning’ we’ve referred to occasionally, a middle-class withdrawal from excess consumption, as well as a reflection on job insecurity, plus a surrender of millions from factories that this Nation allowed to be deconstructed as we outsourced heavy industry.

All of this is ‘interrelated’ and contributed to what I called the unfolding a new era of societal discord, plus lack of harmony between those giving-up, those profiting from enormous stimulus lifting financial assets at the expense of a private sector revitalization (2015 clearly emphasized this pattern with rotational trends peaking in so many previously sustainable sectors). One of the keys to 2016 and beyond will be in ascertaining which of these can be revived or even prosper in a reformed and prolonged recovery that we have projected the United States will be leading, as time evolves.

In the short run, the trick is to avoid societal discord going over-the-edge, even if that means an economic and reform semi-revolution takes place.

This is not a merely a domestic challenge. Actually the risk of violent, rather than mere political upheaval, is all tied together, and already evidenced in all-too-many nations as we all know.

Oddly enough, the FOMC ‘macro-based’ monetary policy and recent rate hike start a trend in recognizing this instability, and a threat to global cohesion that has been evident to many of us for quite some time. The catch is, whether or not the ‘real’ reason for the Fed’s move will be understood, and contain or limit, if not immediately reverse ‘capital flight’ from former export-leaders, and in a sense start the pattern of reduced currency flow to perceived safety. There is that possibility, but this will take time because they let things go so long. It also depends on whether consumers regain faith, because in many countries, including China they clearly didn’t replace export customers.

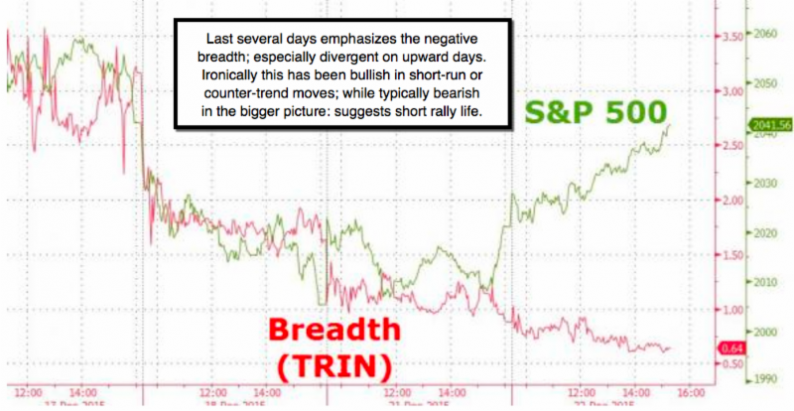

Leave A Comment