Greetings,

We begin with China where the latest reports suggest that the nation’s economic growth may have bottomed for now.

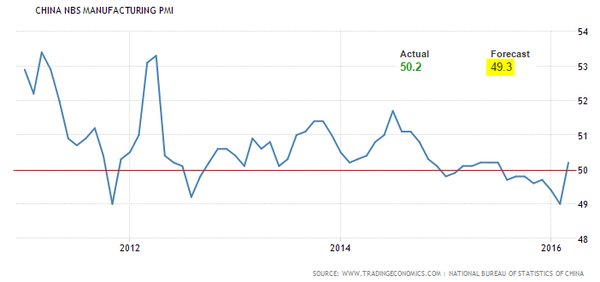

1. China’s official manufacturing PMI beat consensus, showing slight growth (PMI > 50).

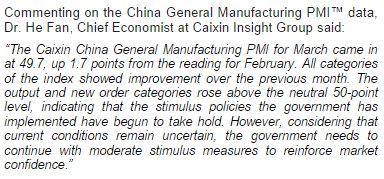

2. The China Caixin Manufacturing PMI also beat expectations. Here is a quote from Caixin on the latest results.

Source: Markit/Caixin

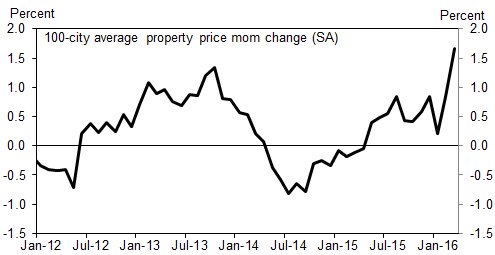

3. China’s property markets are heating up. This is the Soufun 100-city property price index.

Source: Goldman Sachs

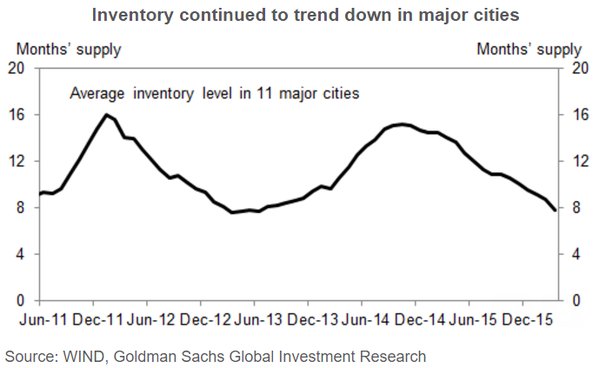

Moreover, China’s housing inventory continues to trend lower.

Source: Goldman Sachs

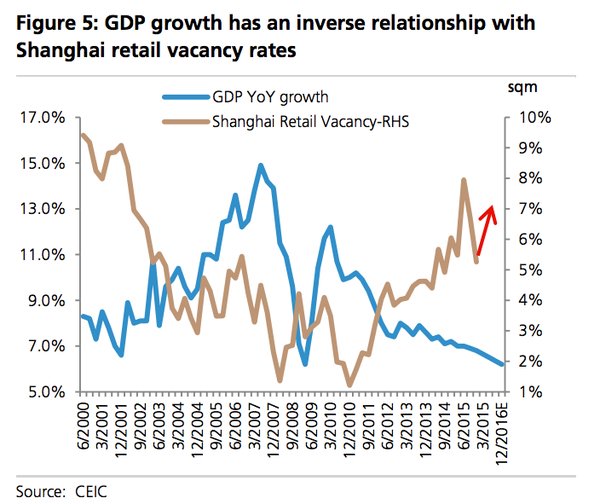

4. Of course, a number of headwinds/risks remain. UBS for example sees Shanghai retail vacancy rates rising going forward.

Source: UBS

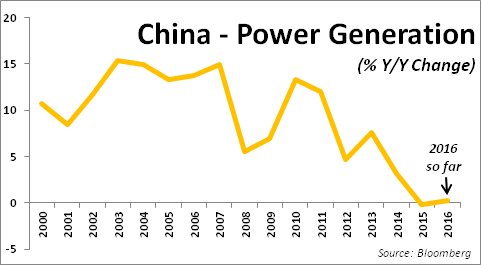

5. China’s “old economy” (heavy industry, etc.) is still struggling as seen by the nation’s power generation growth.

Source: @RBS_Economics

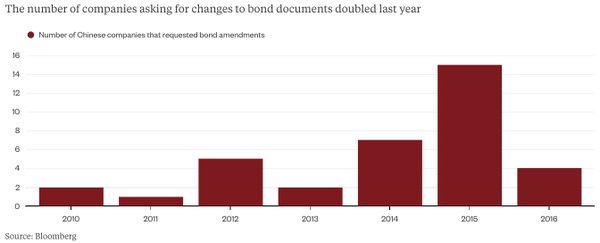

6. There has been an increase in China’s firms asking foreign debt investors to loosen covenants/terms on their debt. China’s corporate credit remains vulnerable.

Source: @vexmark, @Bfly

In other developments, the offshore RMB rate at which banks lend to each other in Hong Kong (HIBOR) went negative for one day. The reason has to do with Beijing imposing reserve requirements for offshore deposits, forcing some banks to cut their deposit balances and flooding the interbank market with liquidity.

Source: @fastFT

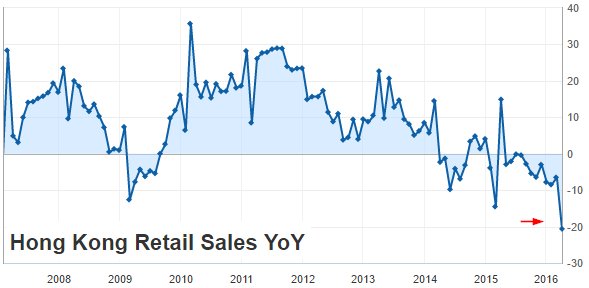

Also in Hong Kong, we see retail sales plunge 13.6% – the biggest slump since 1999.

Now let’s discuss some developments in other emerging economies.

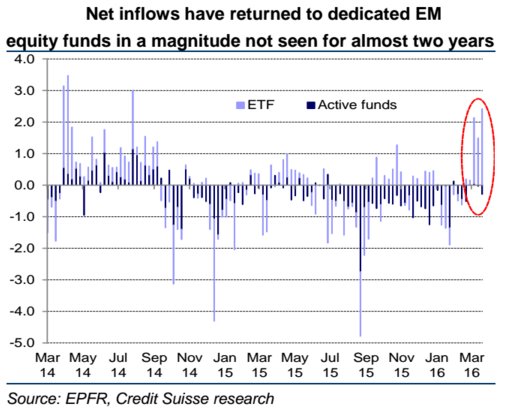

1. Emerging markets (EM) ETF inflows have been the strongest in almost 2 years.

Source: Credit Suisse

2. The dovish Fed and the resulting weakness in the US dollar have added to investors’ confidence in EM investing – for now.

Source: barchart

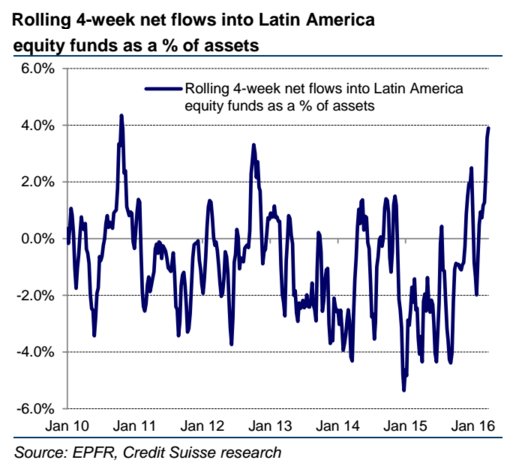

3. Here are the net inflows into Latin America.

Source: Credit Suisse

Leave A Comment