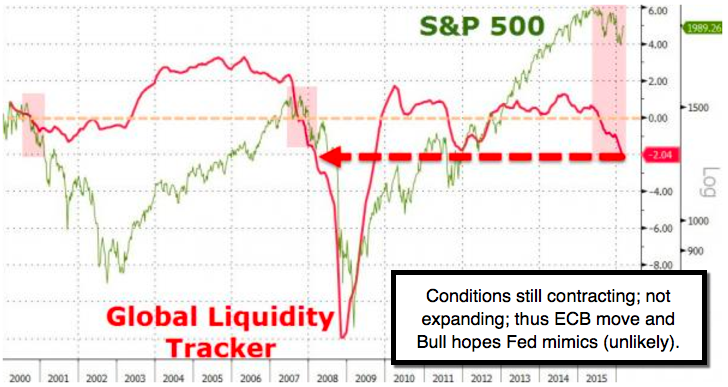

The diminished efficacy of central bank expansion policies increasingly is being recognized by traders, if not monetarists or official interpretations. While I did correctly refer to the ECB-triggered bounce (in advance) as a highly likely ‘buy the rumor / sell the news’ event (a hair above the rebound S&P highs with a ‘pop & flop’ outcome); it’s amazing that investors often don’t see the subtleties of what’s going on. Europe is bailing out bad banks; likely seeing a lower Euro (aside rebounds when FX traders sell intraday weakness); stronger Dollar and at least temporarily new pressure on Oil.

Though we outlined that on Wednesday (and it all worked-out accordingly); you also had OPEC ‘deny’ any meeting of members and non-member producers; a possibility we foresaw based on the intransigence of countries like Kuwait and of course Iran (which could, but so far isn’t, being swayed by Kremlin leverage).

G20 earlier showed us that central bankers are trying to temper what we’d said is a ruinous series of competitive devaluations; as the Chinese in particular are desperately trying to sustain industry (by nationalizing many failing firms, which is the most-key story probably missed in financial reporting during the focus on ECB moves). Deflation continues and is not reversed the way these guys are doing it; and again there is not a fiscal capacity in the EU (sovereigns temper what Draghi can do; and in this case he still has done way too much to we think the chagrin of the Bundesbank).

If Europe continues devaluing the Euro (directly or simply the markets); this is going to help their exports a bit, but the Chinese currency will also be impacted. The whole investor ‘risk-averse cycle’ may see a ‘rinse & repeat’ outcome. So if they settle for a narrower currency range (since they ‘must’ realize alternatives) for the Euro, that will keep the Dollar a bit narrower, and overall that’s stability; which is sorely lacking. However, looking for a break through parity by the Euro might be a wild card, but isn’t totally off the table as the initial reaction implied. So that matters; since even a 1.06-.07 handle on the Euro would thrust the US Dollar higher, and impact China as well as Japan; and help weaken the DJIA, as the U.S. export-situation would be weakened even further.

In-sum: the main issue is that ‘uncertainly’ is heightened, not reduced, by both the ECB’s moves (which smack of desperation and bad-bank bail-outs); while a skeptical Great Britain eyes this complex macroeconomic situation warily. The overall result (and pressures on China) risk compromising currency stability the central bankers pledged to try to sustain (in a comparatively narrow range).

Leave A Comment