Economists no longer expect a recession. Such was according to a recent WSJ survey of Wall Street economists. To wit:

“In the latest quarterly survey by The Wall Street Journal, business and academic economists lowered the probability of a recession within the next year, from 54% on average in July to a more optimistic 48%. That is the first time they have put the probability below 50% since the middle of last year.”

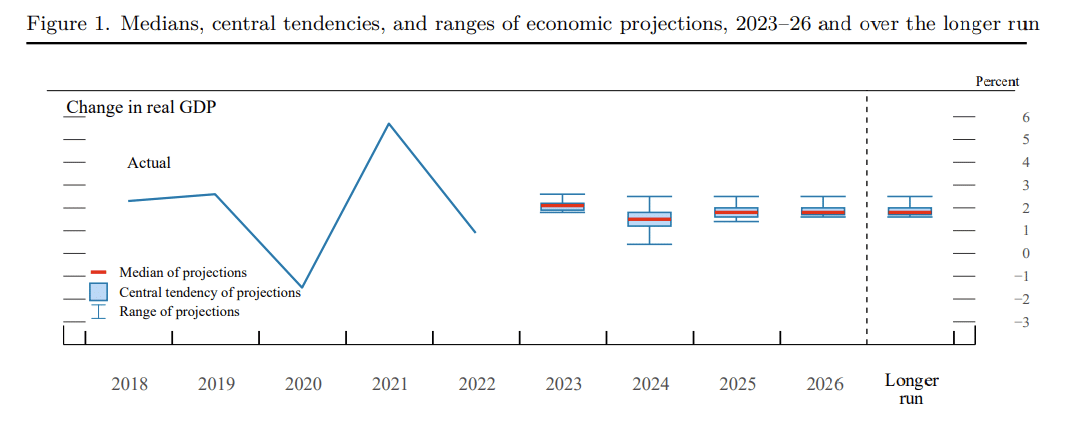

The Federal Reserve also suggests the same. Following the September FOMC meeting, the Federal Reserve reiterated its “higher for longer” mantra and upgraded its economic forecast to include a “no recession” scenario.

“Fueling the optimism are three key factors: inflation continuing to decline, a Federal Reserve that is done raising interest rates, and a robust labor market and economic growth that have outperformed expectations.” – WSJ

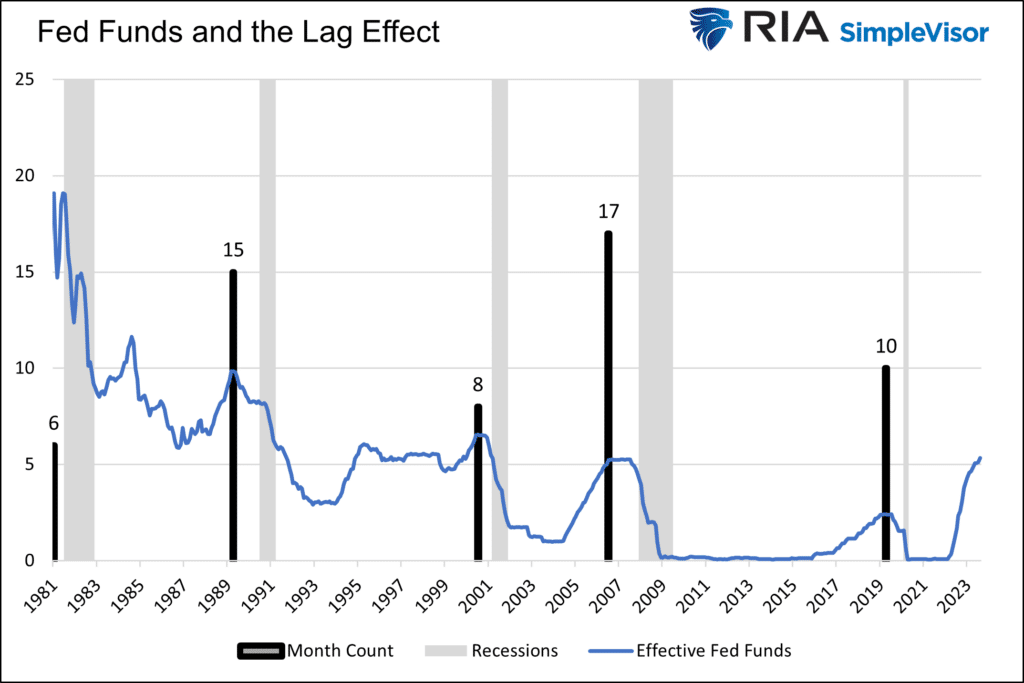

The problem with that optimism is that it is entirely based on lagging economic data. More importantly, that lagging data is subject to relatively large negative revisions in the future. Furthermore, as discussed previously, tighter monetary policy’s “lag effect” is still working through the system. As Michael Lebowitz noted:

“Changes in interest rates only impact new borrowers, including those with maturing debt who must reissue debt to pay back investors of the maturing bonds. Accordingly, higher rates do not impact those with fixed-rate debt that is not maturing. The lag effect occurs due to the time it takes for the new debt issuance to bear enough weight on the economy to slow it down.“

In other words, if the average delay between the final rate increase and recession is 11 months, and the last hike was in July 2023, the risk to forward expectations is quite elevated.Such is why the Fed and economists are always a day late and a dollar short.

A Day Late And A Dollar Short

Given the dependence on economic data subject to significant revisions, it is unsurprising that the Fed and economists are often incorrect in their prognostications. As we wrote in “Fed Projections Are Useless:”

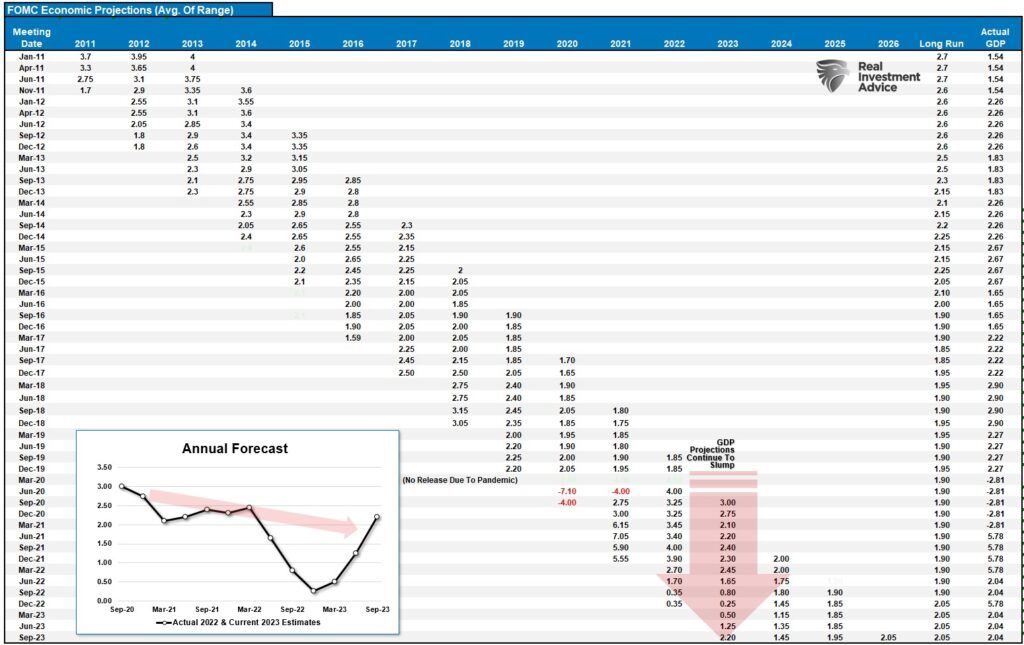

“However, there is a problem with the Fed projections. They are historically the worst economic forecasters ever. We have tracked the median point of the Fed projections since 2011, and they have yet to be accurate. The table and chart show that Fed projections are always inherently overly optimistic. As shown, in 2022, the Fed thought 2022 growth would be near 3%. That has been revised down to just 2.2% currently and will likely be lower by year-end. Like Wall Street analysts with earnings estimates, the Fed’s projections are always initially overly optimistic and guided lower to reality.”

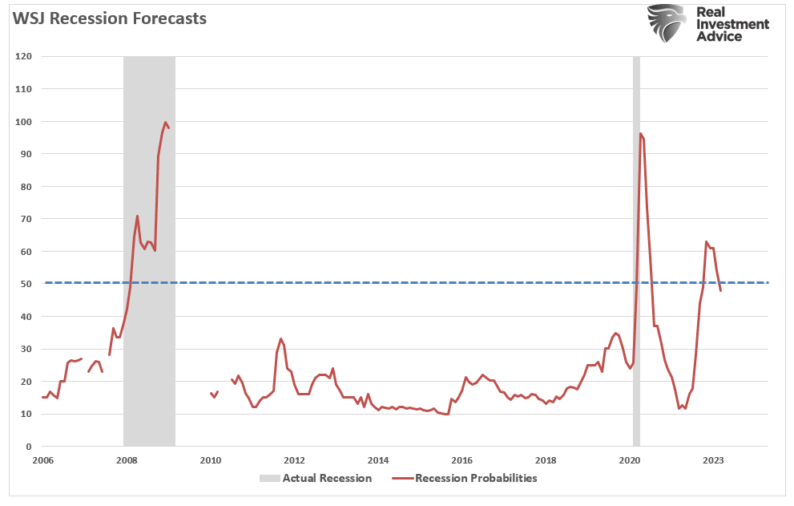

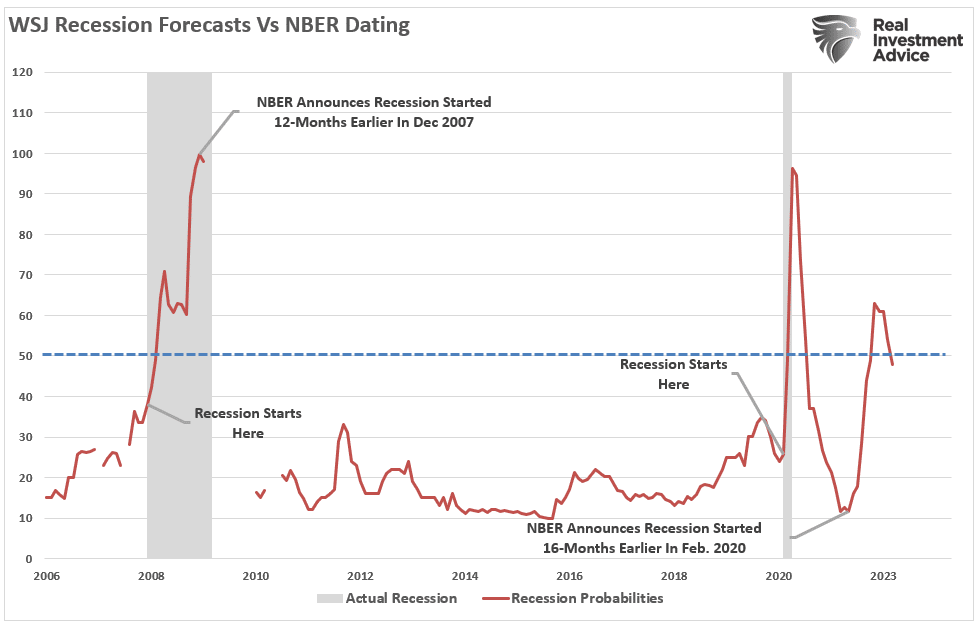

Of course, economists are not much better. Let’s revisit the WSJ survey of Wall Street economists from above. However, this time, we will note the dates that the National Bureau Of Economic Research (NBER) dated the beginning and end of the last two recessions. (The WSJ survey only dates back to 2006.)

While this sample size is relatively small, it does reinforce the point that economists are generally wrong about a “soft landing” scenario. The problem with assessing the state of the economy today based on current data points is that these numbers are only “best guesses.” Economic data is subject to substantive negative revisions as data gets collected and adjusted over the forthcoming 12- and 36-months.Consider for a minute that in January 2008, Chairman Bernanke stated:

“The Federal Reserve is not currently forecasting a recession.”

In hindsight, in December 2008, the NBER dated the start of the official recession in December 2007.If Ben Bernanke didn’t know a recession was underway, how would we?Let’s take a look at the data below of real (inflation-adjusted) economic growth rates:

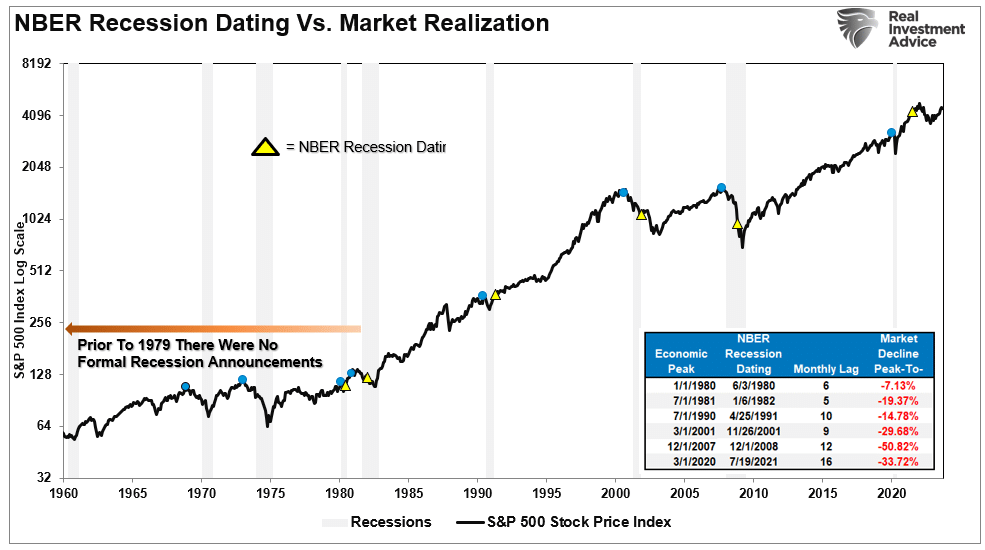

Each of the dates above shows the economy’s growth rate immediately before the onset of a recession. You will note in the table above that in 7 of the last ten recessions, real GDP growth was running at 2% or above. In other words, according to the media, there was NO indication of a recession.But the next month, one began.The chart below shows the S&P 500 with two dots. The blue dots are when the recession started. The yellow triangle is when the NBER dated the start of the recession. In 9 of 10 instances, the S&P 500 peaked and turned lower before the recognition of a recession.

Do you see the problem of the “no recession” call by economists?

Waiting On The Data

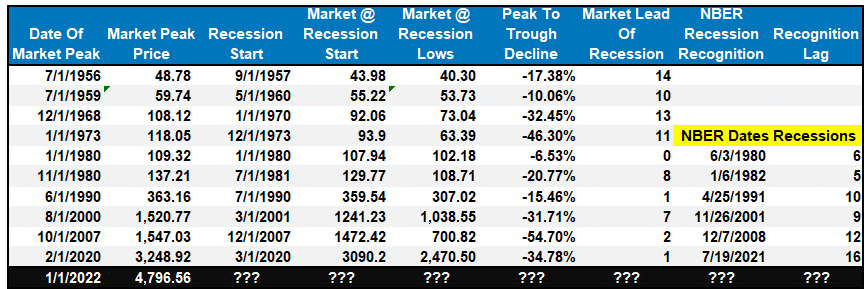

While the WSJ economists are seemingly confident in their expectation of “no recession,” the economic data hasn’t caught up with economic realities. The table below shows the date of the market peak and real GDP versus the start of the recession and GDP growth at that time.  Before 1980, the NBER did not officially date recession starting and ending points.For example:

Before 1980, the NBER did not officially date recession starting and ending points.For example:

As noted above, during 2007, most media, analysts, and the economic community proclaimed there was “no sign of recession.”They were wrong.Today, we are once again seeing many of the same early warnings. Leading economic indicators, inverted yield curves, and the change in monetary velocity suggest the risk of a recession is elevated.There are three lessons to be learned from this analysis:

We suspect the bevy of WSJ economists will again be incorrect in their assumptions.Unfortunately, we won’t have that evidence until it is too late.More By This Author:The Pain Trade Is Higher Into Year-EndSurging Deficits – The Bear’s New MemeRestrictive Yields Will Be The Fed’s Waterloo

Leave A Comment