It seems that the never-ending “thirst for yield” from the world’s massive pension funds, combined with the ever-present “cash on the sidelines” problem, is driving the creation of yet another global financial bubble in emerging market junk bonds.

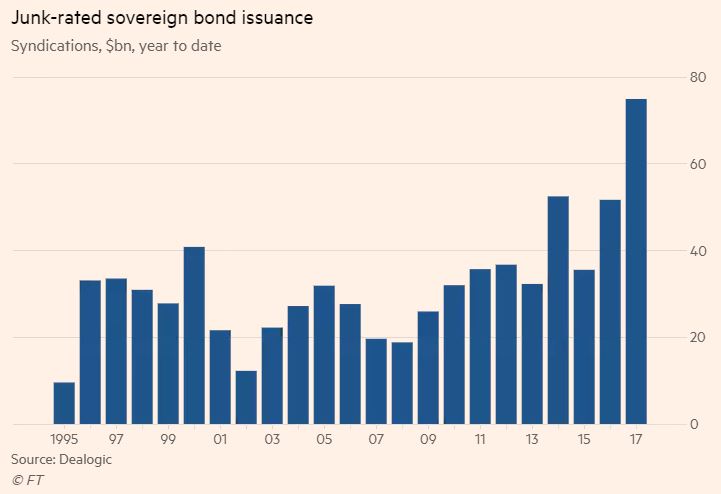

Alas, as the FT points out today, the world’s largest fixed-income investors can’t seem to get enough of the risky paper as bond issuance by the most financially vulnerable countries has suddenly spiked to an all-time high of $75 billion just as spreads are tightening to all-time lows.

Junk-rated emerging market sovereigns have raised $75bn in syndicated bonds so far this year, up 50 per cent year on year to the highest total on record, according to figures from Dealogic, a data provider.

The increase has buoyed the total volume of debt-raising by developing economies; non-investment grade issuance has made up 40 per cent of the new debt syndicated in EM so far in 2017.

These rare and new issuers have been lured into the market by attractive pricing — strong investor demand for EM debt has pushed pricing up and yields down, making it one of the best-performing assets globally in 2017.

According to Bloomberg Barclays indices, EM’s local currency-denominated sovereign debt has returned 10.4 per cent since the start of this year, while dollar-denominated debt has returned 7.6 per cent. By contrast, US Treasuries have returned 2.5 per cent while European nations’ debt has returned 0.9 per cent.

Of course, for all the “doom and gloom” predictions of an imminent crash in Emerging Markets (here and here, among many others), not only have these not materialized, but the average yield on corporate junk bonds issued by emerging markets has dropped to record-low levels of around 5.5%, compared to nearly 10% just 2 years ago.

For a case study of the yield-chasing insanity unleashed by central bankers, one has to look no further than Tajikistan.

Leave A Comment