As we noted in yesterday’s FOMC Preview report, another rate hike this month was a “done deal” for the Federal Reserve, and Powell and Company delivered the expected 25bps increase as expected. The more interesting aspects of today’s release came from the central bank’s accompanying monetary policy statement and the quarterly Summary of Economic Projections.

The central bank made just one change to its monetary policy statement, but it was a doozy: The Fed dropped its long-standing reference to monetary policy remaining “accommodative.” While this change was inevitable at some point (after all, the central bank has stopped QE, started tapering, and raised interest rates eight times in the last few years), the timing suggests that Fed policymakers believe they are nearing a “neutral” interest rate. Of course, with inflation hovering around the Fed’s target, unemployment currently below its projected “longer-run” level, and plenty of fiscal stimulus flowing through the economy, there’s a strong case for above “neutral” interest rates over the next year or more, sothis change does not signal an imminent end to the current rate hike cycle.

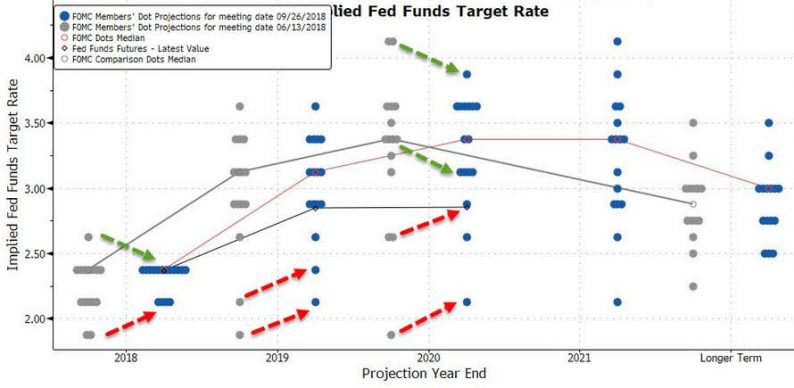

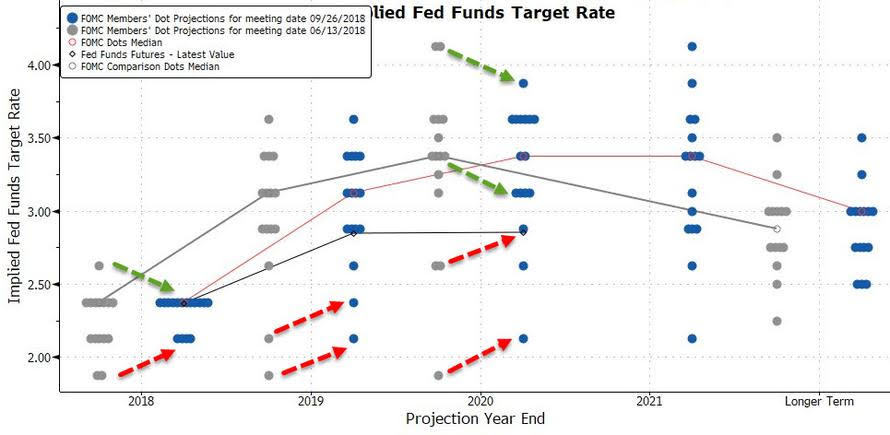

Speaking of interest rates, the Fed also released its member’s estimates for key economic variables in the future. As the chart of the Fed’s “dot plot” shows, the expected path of interest rates is starting to tighten, with outlier projections coming back toward the median member’s expectations in 2019, 2020, and the so-called “Longer-Term:”

Source: ZeroHedge, Federal Reserve

The median interest rate dot remained unchanged in 2018 (2.375%), 2019 (3.125%), and 2020 (3.375%), the median longer-run dot for the neutral interest rate ticked up slightly to 3.000%. Meanwhile, the central bank also revised up its forecasts for GDP growth in 2018 and 2019 (to 3.1% and 2.5% respectively), though it opted to revise its forecast for Core PCE inflation a tick to just 2.0% in 2019.

Leave A Comment