After a turbulent overnight session on Monday morning, this morning traders settle at their desks to find a relatively calmer environment, with US equity futures down 0.2% to 2,371.75, while European stocks fell for a third consecutive day, and Asian markets which closed mixed (China up, Nikkei down, MXAP up 0.2%). Basic metals continue to slide following another drop in copper as a result of the biggest inventory inflow to LME warehouses in 15 years, coupled with worries about China’s telegraphed slowdown.Some have also pointed out that the market topped just in time for the SNAP IPO, which after crashing yesterday to below its IPO break price of $24, continued to sink in the pre-market this morning.

In addition to hopes about an imminent Fed rate hike shifting to concerns, as reported yesterday JPMorgan warned that hawkish Fed rhetoric has increased the likelihood for a short-term pullback after stocks hit the bank’s year-end target of 2,400 the previous week. The dollar rose modestly as a surge in corporate bond issuance pushed up Treasury yields.

Markets appear to have topped off the relentless post-election surge, and are coming off recent peaks as investors start to contemplate what the upcoming March interest rate increase will mean for risk assets. They also have to contend with overnight headlines out of China where the “Two Sessions” are taking place, and where Premier Li Keqiang warned of larger challenges ahead during his work report to the annual National People’s Congress gathering in Beijing. In Europe, politics has become the main market driver as election campaigns in the Netherlands, France and Germany put the status quo under threat.

“The ‘pothole’ is a political one with far-right parties gaining ground in opinion polls ahead of both a Dutch and French ballots in spring,” Luca Paolini, chief strategist at Geneva-based Pictet, said in a research note. “We are scaling back exposure to European stocks, albeit retaining our overweight stance.”

Germany’s largest lender continued to grab attention and European stocks fell for a third consecutive day on Tuesday, once again dragged down by financials as Deutsche Bank shares slid again on deepening concern about its health after its $8.5 billion cash call. Deutsche shares dropped as much as 3% to a fresh 2017 low. They have lost more than 10% in the last few days since the bank said it would tap investors for $8.5 billion.

Furthermore, a batch of weak corporate earnings reports and the biggest fall in German industrial orders since the depths of the global financial crisis also disappointed investors, setting the tone for a lackluster session in Europe.German industrial orders slumped 7.4 percent in January, the biggest fall since January 2009 and nearly three times as steep as the 2.5 percent fall expected by economists.

“Weak German industrial orders suggests it’s not a one-way ticket in Europe – there’s been a lot of bullishness around European equities lately but maybe this is a sign it’s not all positive. Deutsche Bank is not helping either,” Neil Wilson, senior market analyst at ETX Capital, told Reuters.

Across the Atlantic, S&P 500 futures pointed to a slightly lower open on Wall Street, further cooling off last week’s record highs. MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.4%, and Japan’s Nikkei closed down 0.2%.

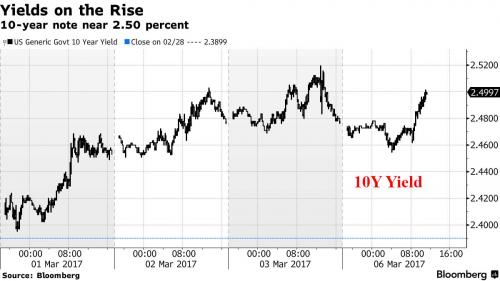

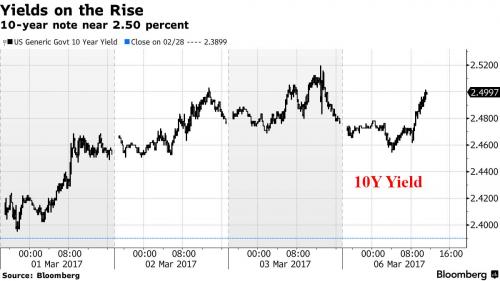

In currencies, the dollar inched higher against a basket of trade-weighted peers. The dollar index rose 0.1 percent to 101.73 mirroring Monday’s slender gain. The Bloomberg Dollar Spot Index added 0.2 percent, headed for its sixth advance in seven days. A rate hike from the Federal Reserve next week is virtually fully priced into financial markets, so the dollar and U.S. bond yields might be vulnerable to a correction lower. But investors saw enough room to push the greenback and yields higher on Tuesday, lifting the 10-year yield for the fifth day in a row back above 2.50 percent and the two-year yield up a basis point to 1.32 percent, on what traders attributed to interest rate locks following another massive corporate issuance session.

The Aussie Dollar has rallied after the RBA left rates on hold, as widely expected. The post meeting statement pointed to a firmly on hold RBA and few expect a change in the cash rate through 2017 or 2018. The pound was the biggest mover on major FX markets, falling nearly a third of one percent against the dollar to a seven-week low of $1.2202. Britain’s House of Lords will on Tuesday try to force the government to give lawmakers a greater say over the terms of Britain’s exit from the European Union and final approval of an eventual deal with the block.

Leave A Comment