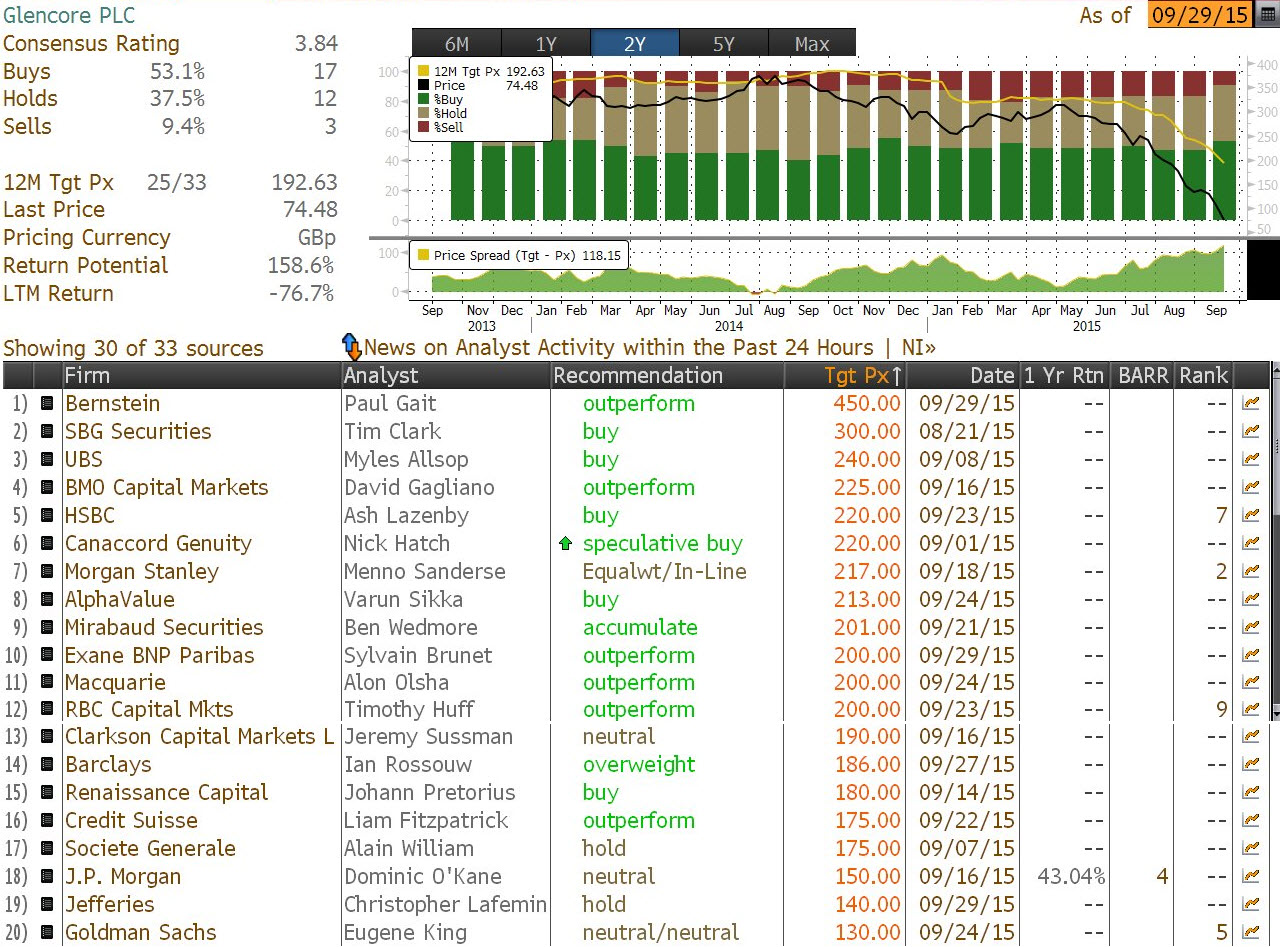

After its biggest daily crash in history on concerns Glencore’s (or Glenron as it has been called recently) equity is worthless unless commodities stage a dramatic rebound (a crash which together with the plunge in Volkswagen has cost the Qatar sovereign wealth fund $12 billion in paper losses), the company’s awestruck sellside following – the vast bulk of which has been defeneding a “buy” rating ever through the company’s historic collapse, has decided to give it one last push, and double down all-in on their ridiculous, and massively money-losing “buy” recos.

Click on picture to enlarge

First, it was Bernstein’s Paul Gait (with a laughable price target of 450p – the highest on the street -or about 380p higher than the current price), which said it sees real economic value in both of Glencore’s businesses – clearly, hence the price target. The problem is it never saw the catalyst that slammed the stock to record lows. Bernstein continues that its assessment of commodity trading, a “fundamental building block of the global economy,” as having suddenly lost fundamental value “seems absurd.”

What Bernstein is unable to grasp is that “commodity trading” has not lost value at all, but it is Glencore’s commodity trading that now faces a binary future, one where a downgrade from Investment Grade does in fact lose all value of Glencore’s trading division, as the company simply can not continue to operate under its current liquidity regime with a “Junk” rating.

More from Bernstein, which also says that the market “appears to have an endless appetite to price the instantaneous present as if it were a fair reflection of everlasting reality,” which is “less than staggering in its intellectual profundity.”

Because when you’ve been epically wrong, surely your best bet is to go ad hominem with the entire market.

Bernstein’s bottom line: insolvency concerns are unwarraned even if the industrial assets continue to produce spot Ebitda margins at spot prices, and the trading unit contributes nothing, Bernstein still sees 93p of value.

Leave A Comment