The time tested proverb “A gold mine is a hole in the ground with a liar at the top” is generally attributed to Mark Twain, although he may have just popularized it. The last few years, he has a lot of company in feeling that way. Other than the coal miners, gold miners have probably been the most despised stock sector on earth the last 3 years. But then along comes the surprise January beat down in the stock market, and gold is showing some signs of life. A passing two month start-of-the-year blip some are saying, just like the start of every year since 2011, except for 2013, the crash year for gold. But there are some big differences this time at the start of 2016.

There is a banking angst building over the malinvestment debt of the ZIRP years, as I’ve mentioned in previous articles, and that has been boiling over here in mid February with a decimation of the big bank stocks. The whole banking/bad commodities loan mess engulfing our markets nowadays is perhaps sparking a major turn to gold, not as a commodity but as an alternative currency. If you want to look at a leading edge in all this, the country of South Africa is a good place to look.

This nation is a major gold miner and is also caught up in the emerging market currency problems typical of nations exporting a lot of commodities. The leading export destination of the copper, nichol, and whatnot from South Africa is China. During the years they were producing 60% or more of the world’s gold supply (to the late ’80s) many South African gold companies became public mainstays in the stock market. Currently they have slipped just out of the top 5 global producers, but the 5 ahead of them are either not emerging market nations or don’t have a lot of major public gold miners. As such, this nation’s currency/gold situation is an early tell of any major turn in gold. A Bloomberg article last month noted this South African thing as their gold miners pay all their costs in the local currency, the rand, and reap all their revenue in dollars:

“The gold price has held up pretty well, but the rand has blown off terribly,” Peter Major, a mining analyst at Cadiz Specialized Asset Management in Cape Town, said by phone. “Gold companies, which were marginal and barely making money when the rand was 13 to one, will benefit when the rand suddenly goes to 16 or 17. All of a sudden they’re making 20 percent more revenue and it all goes to the bottom-line.”

So how is this early gold tell doing?

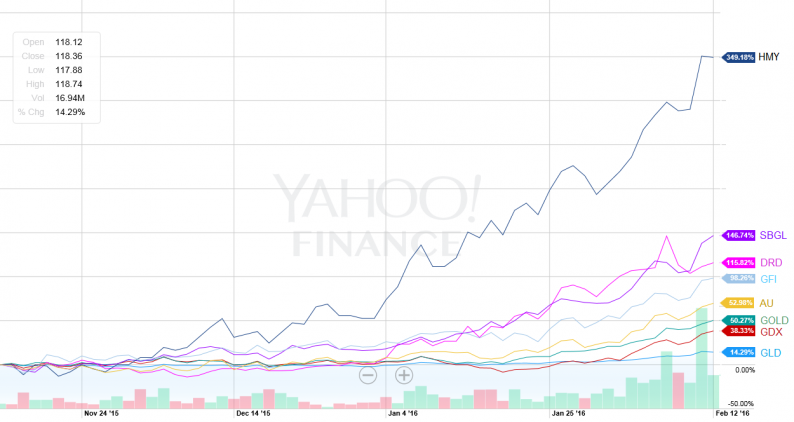

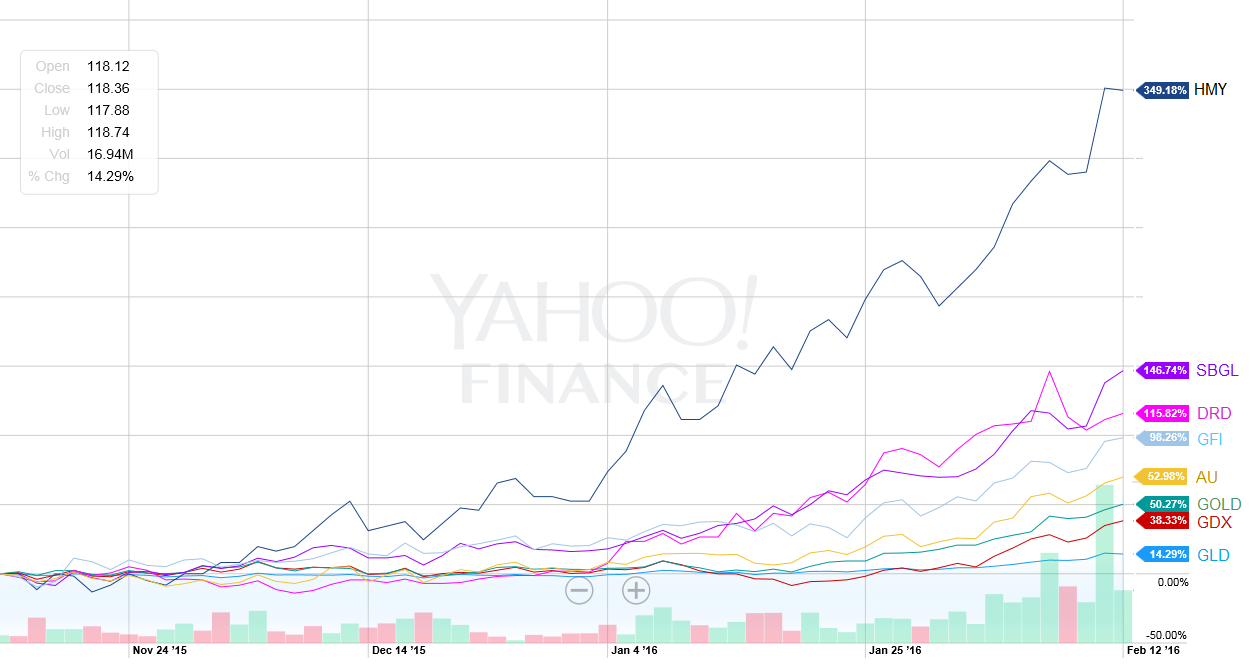

Here I compared a half dozen of South Africa’s largest gold companies with the gold price (GLD) and with the general gold miners ETF (GDX) over the last three months. A very large outperformance is clear and began even before the start of January. The above article points out that the currency problems of the world are responsible for some 20% more revenue coming the way of South Africa domiciled gold companies. And this is at no cost of revenue whatsoever for them and it all goes straight to profit, and stock values. If you average the performance of these stocks, you get a massive 98% outperformance over the GDX – in just three months. The market seems to think currency problems are here to stay, as well as better gold prices.

The steady decline of gold since the 2011 peak is generally thought of as a bear market. But I would like to explore the possibility that a very large scale bull market actually includes this 4 year decline, and may be departing into a phase 3 of this type of bull market, agreeing with the tell of the South African miners. Major bull markets tend to run in repeating patterns or fractals. Markets, as well as many things in nature, move in these patterns at different scales. One such pattern I have written about before is the separated parabola. An example of this is the currency market of 1920’s Germany, which was the most prevalent scale of this fractal, the 64 month:

Leave A Comment