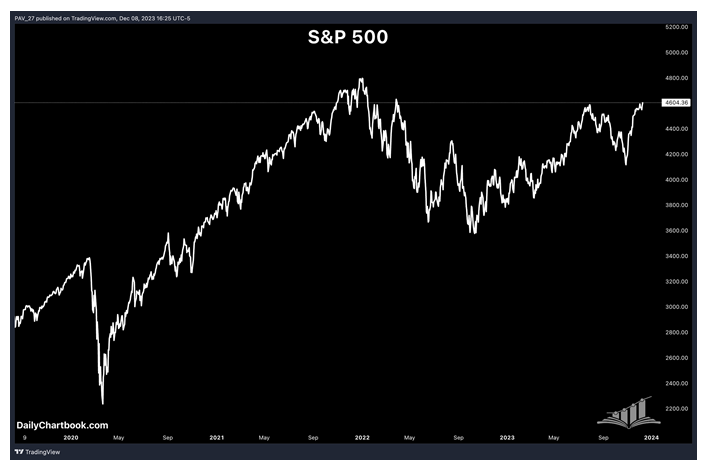

Welcome to our weekly commentary and insight on the markets, economy and global macro inputs that have an impact on the investment landscape in the near future. We are pleased you are here. Welcome to our weekly commentary and insight on the markets, economy and global macro inputs that have an impact on the investment landscape in the near future. We are pleased you are here. The markets ended on a positive note yesterday and continue their upward bias. We invite you to go back and review the past couple of weeks of Market Outlook which provided more details on how we began to see the rally coming in the markets. A combination of seasonal cycles coupled with positive indicators and our proprietary color charts showed a positive market environment approaching in late October. (Click here for last week’s Outlook) The S&P 500 had the highest daily close yesterday (Friday, December 8) since March of 2022 when it began its long decline and produced a negative 2022 yearly return. See chart below:

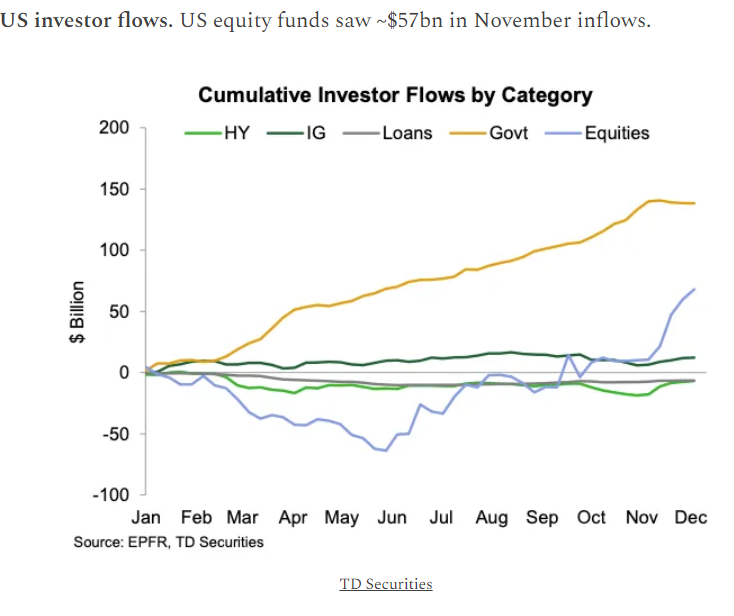

The markets ended on a positive note yesterday and continue their upward bias. We invite you to go back and review the past couple of weeks of Market Outlook which provided more details on how we began to see the rally coming in the markets. A combination of seasonal cycles coupled with positive indicators and our proprietary color charts showed a positive market environment approaching in late October. (Click here for last week’s Outlook) The S&P 500 had the highest daily close yesterday (Friday, December 8) since March of 2022 when it began its long decline and produced a negative 2022 yearly return. See chart below: November saw huge inflows into the stock market. See chart below:

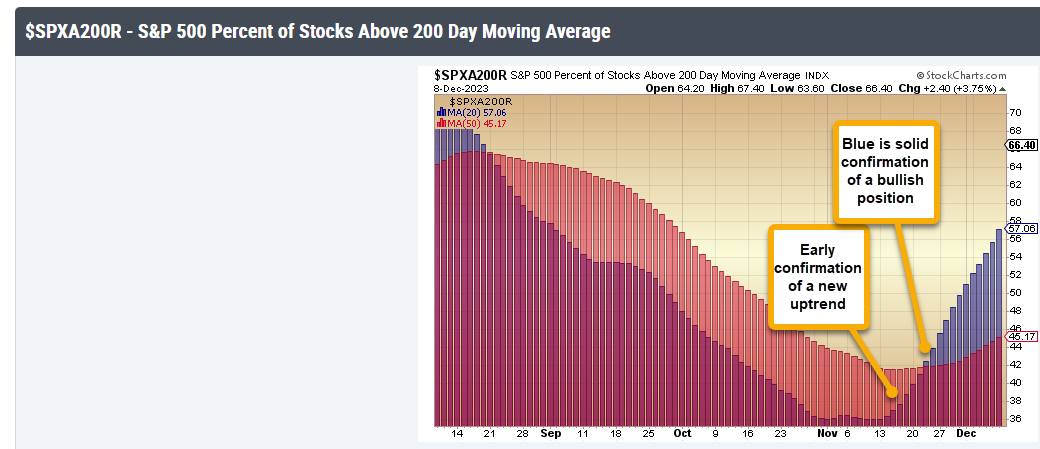

November saw huge inflows into the stock market. See chart below: While we cover the short, intermediate and longer-term charts that are compared to their 20-, 50- and 200-day moving averages for the Dow, the NYSE, NDX, and S&P 500, we want to illustrate below the longer term chart for just the S&P 500. It is rather easy to make the case that we are indeed in a period of upward market bias. Every day the number of S&P 500 companies that are above their 200-day moving average is increasing.

While we cover the short, intermediate and longer-term charts that are compared to their 20-, 50- and 200-day moving averages for the Dow, the NYSE, NDX, and S&P 500, we want to illustrate below the longer term chart for just the S&P 500. It is rather easy to make the case that we are indeed in a period of upward market bias. Every day the number of S&P 500 companies that are above their 200-day moving average is increasing. We consider this one of our longer term “safe” illustrations and indications of a positive or negative market environment. In late October we showed that the 20-day and 50-day charts had indicated a positive, bullish bias was approaching in the last week of October.Subscribers (of Profit Navigator) are aware of that algo’s powerful and robust engine, and that indicated a positive signal (and to take a position in SPY or SSO (2x SPY)) towards the end of October. The signal was triggered a few days before the market turned at the end of October. It’s All About the Magnificent 7.We continue to hear the narrative that it is all about the Magnificent 7’s overweight influence on the S&P 500. These 7 stocks, Alphabet, Apple, Amazon, Microsoft, Netflix, Nvidia and Tesla, do have a significant influence on the S&P 500 index (certainly as well with the NASDAQ 100-QQQ)Most of these stocks are valued at or above $1 trillion in market cap so they are the biggest companies in America (Apple is now over $3 trillion in market value). Given that the S&P 500 index is a market cap influenced index it makes perfect sense that these 7 companies would comprise 30% or more of the S&P 500 index influence. For the purposes of this illustration, let’s look at the group as if it was ONE stock. These are some of the current characteristics that would make up this one stock:

We consider this one of our longer term “safe” illustrations and indications of a positive or negative market environment. In late October we showed that the 20-day and 50-day charts had indicated a positive, bullish bias was approaching in the last week of October.Subscribers (of Profit Navigator) are aware of that algo’s powerful and robust engine, and that indicated a positive signal (and to take a position in SPY or SSO (2x SPY)) towards the end of October. The signal was triggered a few days before the market turned at the end of October. It’s All About the Magnificent 7.We continue to hear the narrative that it is all about the Magnificent 7’s overweight influence on the S&P 500. These 7 stocks, Alphabet, Apple, Amazon, Microsoft, Netflix, Nvidia and Tesla, do have a significant influence on the S&P 500 index (certainly as well with the NASDAQ 100-QQQ)Most of these stocks are valued at or above $1 trillion in market cap so they are the biggest companies in America (Apple is now over $3 trillion in market value). Given that the S&P 500 index is a market cap influenced index it makes perfect sense that these 7 companies would comprise 30% or more of the S&P 500 index influence. For the purposes of this illustration, let’s look at the group as if it was ONE stock. These are some of the current characteristics that would make up this one stock:

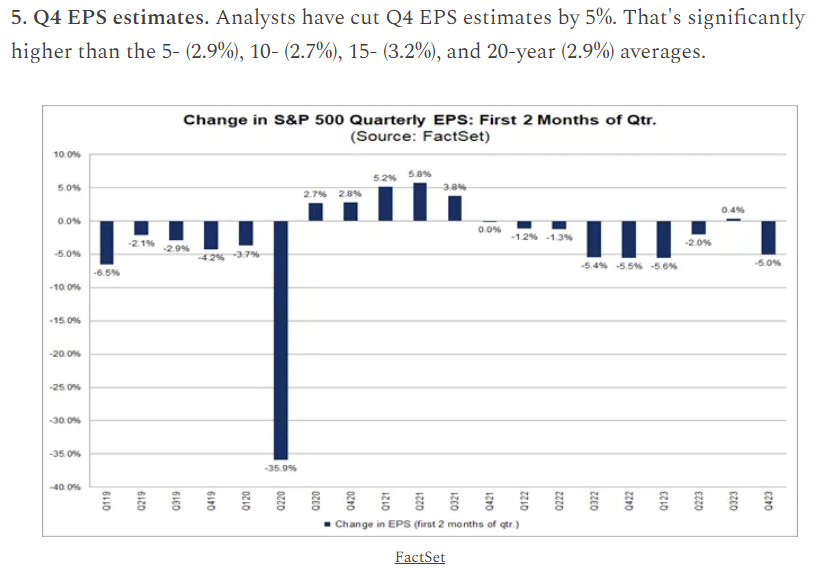

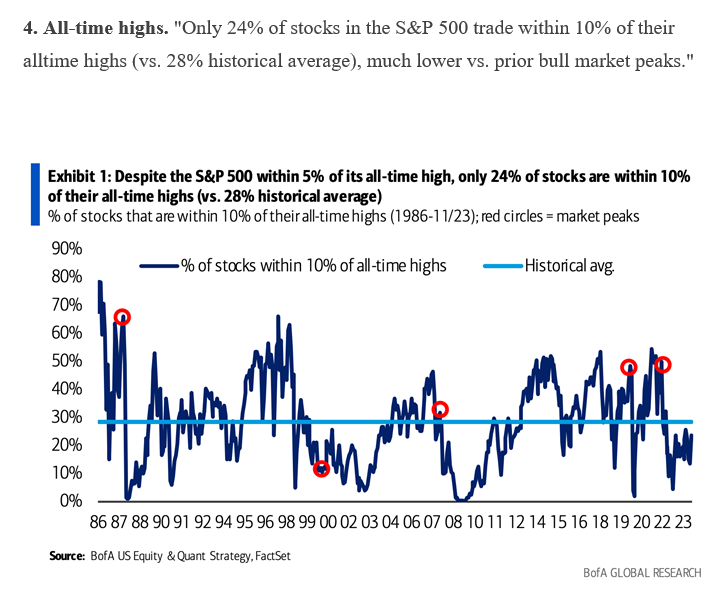

These 7 stocks have helped fuel the S&P 500 index’s 19% gain for 2023. Compare that to the equal weighted index (where each of the 500 companies have an equal 2% contribution to the index) which is up 6% year-to-date.If you notice the last bullet point above, you will note that expectations are for these 7 stocks to begin to have earnings per share growth that begins to decelerate.Would we recommend buying these 7 stocks now? Since we don’t make discretionary decisions and instead depend on our formulaic algorithms to do the heavy lifting, our likely answer is we would be CAUTIOUS. These stocks are priced for perfection. Momentum may carry them further but if you look at the analysis they are selling at very high P/E multiples at this time.Looking at the most recent expectations for earnings growth (according to FactSet) for the markets (see below), you will notice that analysts are starting to reduce their forecasts for positive earnings growth. If EPS growth rates start to slow, it may very well have a greater impact on these 7 as they now sell for lofty valuations. This is also why some of these stocks have stalled recently while smaller companies, including those in the Russell 2000 small-cap index have begun to appreciate and gain momentum. Don’t listen to all the narrative that it is ONLY these 7 stocks that are driving the market. This is not true and as our color chart above indicates, many, if not the majority of the stocks that make up the S&P 500 are currently participating in this year’s positive return. More importantly, many stocks that comprise the S&P 500 index are considered attractively priced and more favorably valued with plenty of room to appreciate further. See chart below:

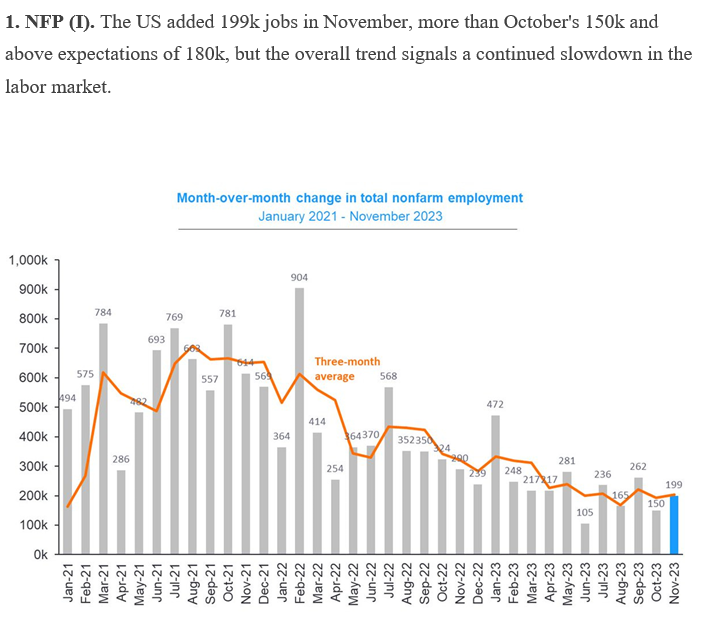

Don’t listen to all the narrative that it is ONLY these 7 stocks that are driving the market. This is not true and as our color chart above indicates, many, if not the majority of the stocks that make up the S&P 500 are currently participating in this year’s positive return. More importantly, many stocks that comprise the S&P 500 index are considered attractively priced and more favorably valued with plenty of room to appreciate further. See chart below: JOBS… For now, it looks like a soft landing.Friday, November’s job report came out at 8:30 EST. This monthly release came out above expectations at 190,000 new jobs created. Unemployment dropped. These numbers were better than October’s 150,000 jobs and slightly better than the estimated 180,000 number expected. Job creation continues to show a positive albeit a slowing monthly number. It is the consistent slowing throughout 2023 that will likely prevent the Fed from raising rates further at their December meeting next week. See chart below:

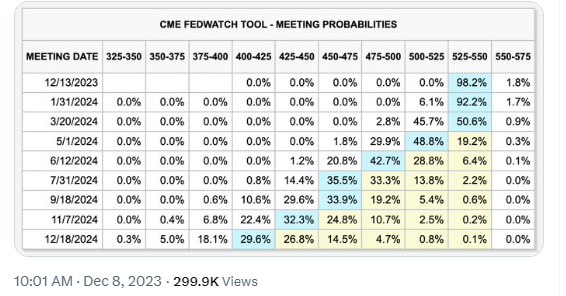

JOBS… For now, it looks like a soft landing.Friday, November’s job report came out at 8:30 EST. This monthly release came out above expectations at 190,000 new jobs created. Unemployment dropped. These numbers were better than October’s 150,000 jobs and slightly better than the estimated 180,000 number expected. Job creation continues to show a positive albeit a slowing monthly number. It is the consistent slowing throughout 2023 that will likely prevent the Fed from raising rates further at their December meeting next week. See chart below: For now, the country appears to be fully employed. People have high enough disposable incomes to pay bills, buy groceries, keep Amazon crazy busy daily, enjoy entertainment, and have enough left off to travel and keep the economy bustling.A few weeks ago, the GDP print (positive) also beat expectations. However, since then certain parts of the economy have slowed enough that interest rates have fallen by over 70 bp on the 10-year Treasury (from 5% in October to 7.24% yesterday). Has the Fed engineered a soft landing? For now, it appears so.In fact, many of the leading economists believe that the economy will avoid a recession so long as job creation and GDP stay positive, even if in low positive monthly changes. There are those Analysts however, that wish to remain cautious as we go into 2024. (Can we avoid a hard landing?)One such analyst who has a long history of accurate market calls and continues to dissect micro variables of the economy is Michael Hartnett of Banc of America Corp. Michael takes a different tact regarding the fall in interest rates that has been occurring the past 6 weeks. He believes that they are signaling sputtering economic growth.The strategist, who has remained bearish even as the S&P 500 rallied about 19% this year—said lower yields were one of the main catalysts of equity gains in the current quarter. However, should they drop further to 3% that would signal (to him) a “hard landing” for the economy.The narrative of “lower yields=higher stocks” would flip to “lower yields=lower stocks” Hartnett wrote in a note dated December 7, 2023.After one of the best November stock market gains in a century, the rally in US stocks has just about stalled this month. The S&P is only up 0.40% so far in December.Economists and money managers appearing on the major media are even moving up when the Fed may begin reducing interest rates. We don’t see it yet and maintain our “higher for longer” narrative. Here are the current estimates for if/when the Fed will begin cutting interest rates. The consensus is now for May 2024 with some believing that it could happen as early as March 2024. (if that happened that should provide a tailwind for the stock market). See chart below:

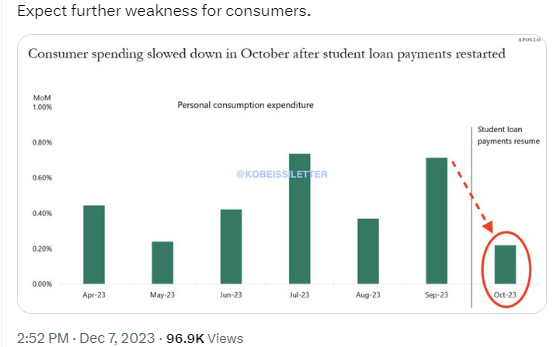

For now, the country appears to be fully employed. People have high enough disposable incomes to pay bills, buy groceries, keep Amazon crazy busy daily, enjoy entertainment, and have enough left off to travel and keep the economy bustling.A few weeks ago, the GDP print (positive) also beat expectations. However, since then certain parts of the economy have slowed enough that interest rates have fallen by over 70 bp on the 10-year Treasury (from 5% in October to 7.24% yesterday). Has the Fed engineered a soft landing? For now, it appears so.In fact, many of the leading economists believe that the economy will avoid a recession so long as job creation and GDP stay positive, even if in low positive monthly changes. There are those Analysts however, that wish to remain cautious as we go into 2024. (Can we avoid a hard landing?)One such analyst who has a long history of accurate market calls and continues to dissect micro variables of the economy is Michael Hartnett of Banc of America Corp. Michael takes a different tact regarding the fall in interest rates that has been occurring the past 6 weeks. He believes that they are signaling sputtering economic growth.The strategist, who has remained bearish even as the S&P 500 rallied about 19% this year—said lower yields were one of the main catalysts of equity gains in the current quarter. However, should they drop further to 3% that would signal (to him) a “hard landing” for the economy.The narrative of “lower yields=higher stocks” would flip to “lower yields=lower stocks” Hartnett wrote in a note dated December 7, 2023.After one of the best November stock market gains in a century, the rally in US stocks has just about stalled this month. The S&P is only up 0.40% so far in December.Economists and money managers appearing on the major media are even moving up when the Fed may begin reducing interest rates. We don’t see it yet and maintain our “higher for longer” narrative. Here are the current estimates for if/when the Fed will begin cutting interest rates. The consensus is now for May 2024 with some believing that it could happen as early as March 2024. (if that happened that should provide a tailwind for the stock market). See chart below: Continue to watch the payroll growth over the next few months. If you see a rise by less than 100,0000, that could signal a harder landing forthcoming.It is interesting to note that Mr. Hartnett’s analysis contrasts with BofA’s own quantitative strategist Savita Subramanian (who often appears on CNBC), who expects the S&P 500 to continue rallying to record highs next year on cooing inflation and corporate efficiencies.Forecasters at Deutsche Bank Group AG and RBC Capital Markets also predict an all-time high for the index in 2024.Morgan Stanley’s Michael Wilson who accurately predicted the bear market of 2022, and continues to be quite bearish, has a more neutral outlook. One area of concern for 2024 is consumer spending.We are all too aware that 70% plus of economic activity in the US is consumer spending. October spending slowed down leading some economic pundits to predict that we could see a hard landing next year in the retail sector as consumers are increasingly getting more “tapped out”. See October chart below:

Continue to watch the payroll growth over the next few months. If you see a rise by less than 100,0000, that could signal a harder landing forthcoming.It is interesting to note that Mr. Hartnett’s analysis contrasts with BofA’s own quantitative strategist Savita Subramanian (who often appears on CNBC), who expects the S&P 500 to continue rallying to record highs next year on cooing inflation and corporate efficiencies.Forecasters at Deutsche Bank Group AG and RBC Capital Markets also predict an all-time high for the index in 2024.Morgan Stanley’s Michael Wilson who accurately predicted the bear market of 2022, and continues to be quite bearish, has a more neutral outlook. One area of concern for 2024 is consumer spending.We are all too aware that 70% plus of economic activity in the US is consumer spending. October spending slowed down leading some economic pundits to predict that we could see a hard landing next year in the retail sector as consumers are increasingly getting more “tapped out”. See October chart below: In a recent article featuring Elon Musk (Founder of Tesla) and Michael Burry (author of the BIG SHORT) commented on consumer spending, Musk painted a negative picture by stating “A large number of people are living paycheck to paycheck and with a lot of debt.” He further commented that credit card payments have hit “extremely punishing” levels. “If the consumer cannot pay them off and they are still accruing interest at 20%, these people are headed to a bad place.”Similarly, Michael Burry has been predicting since 2022 that consumers were blowing through their pandemic savings, putting less money away, and using their credit cards more often to afford higher prices and rising interest payments. He predicted that would inevitably lead to a spending slowdown and a recession.Recently, Citadel’s Ken Griffin, bond billionaires Bill Gross and Jeff Gundlach, JP Morgan’s Bob Michele as well as Morgan Stanley’s Mike Wilson, economist David Rosenberg and Stephanie Pomboy have ALL RAISED the same concerns.Their worries are rooted in the fact that American consumers have faced a double-whammy of brutal inflation and surging borrowing costs during the past 18 months. Prices grew and hit a 40-year high of over 9% last summer, and these inflated costs remain intact regardless of any cooling that you might be seeing or hearing about. Corporate America is not going to suddenly reduce prices. These higher prices along with stable margins are here to stay. They are sticky and will continue to cause undue pain on the American consumer.For now, many economists expect a slowdown in household spending but not a full-blown recession. The jury is out.More By This Author:A November to Remember! What Might December Hold? A Shiny Metal Makes a New Historical High.Emerging Markets Versus U.S. MarketsEconomic Modern Family-Home For The Holidays

In a recent article featuring Elon Musk (Founder of Tesla) and Michael Burry (author of the BIG SHORT) commented on consumer spending, Musk painted a negative picture by stating “A large number of people are living paycheck to paycheck and with a lot of debt.” He further commented that credit card payments have hit “extremely punishing” levels. “If the consumer cannot pay them off and they are still accruing interest at 20%, these people are headed to a bad place.”Similarly, Michael Burry has been predicting since 2022 that consumers were blowing through their pandemic savings, putting less money away, and using their credit cards more often to afford higher prices and rising interest payments. He predicted that would inevitably lead to a spending slowdown and a recession.Recently, Citadel’s Ken Griffin, bond billionaires Bill Gross and Jeff Gundlach, JP Morgan’s Bob Michele as well as Morgan Stanley’s Mike Wilson, economist David Rosenberg and Stephanie Pomboy have ALL RAISED the same concerns.Their worries are rooted in the fact that American consumers have faced a double-whammy of brutal inflation and surging borrowing costs during the past 18 months. Prices grew and hit a 40-year high of over 9% last summer, and these inflated costs remain intact regardless of any cooling that you might be seeing or hearing about. Corporate America is not going to suddenly reduce prices. These higher prices along with stable margins are here to stay. They are sticky and will continue to cause undue pain on the American consumer.For now, many economists expect a slowdown in household spending but not a full-blown recession. The jury is out.More By This Author:A November to Remember! What Might December Hold? A Shiny Metal Makes a New Historical High.Emerging Markets Versus U.S. MarketsEconomic Modern Family-Home For The Holidays

Leave A Comment