HCP (HCP) released its 4th quarter and full year results on February 9th.

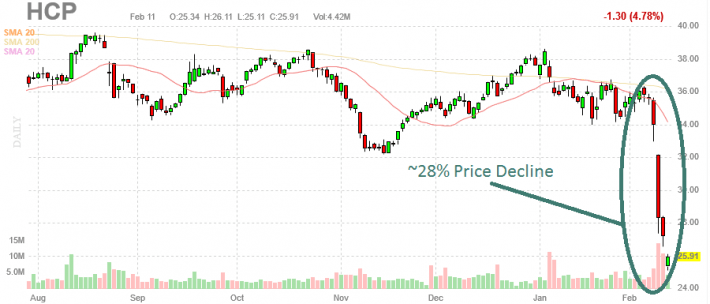

The market did not like the results. HCP stock fell from $34/share down to $28/share in one day. The company’s stock has declined ~28% over the last week.

Source: Finviz

The company’s stock has a dividend yield of 8.5%. If HCP can pay steady or increasing dividends it is an absolute bargain.

If it doesn’t, it is a ‘yield trap’ – a stock or REIT that lures in income investors with its high dividend – only to slash the dividend later.

HCP’s price decline is a result of its post-acute/skilled nursing segment posting poor results. Specifically, the segment’s HCR ManorCare assets are performing poorly.

HCP generates around 25% of its income from the post-acute/skilled nursing segment. HCR ManorCare operations are responsible for 72% of the post-acute/skilled nursing segment. This means HCR ManorCare is around 20% of HCP’s total business.

Knowing the percentage size of the underperforming asset is important in determining what will happen with HCP’s dividend (and earnings).

At ~20% of the company’s business (based on income), HCR ManorCare is important to the company.

Changes in payer mix from traditional Medicare to Managed Care plans have reduced both rates and patients to post-acute/skilled nursing facilities. The company has reduced the book value of its HCR ManorCare holdings from ~$6 billion to $5.2 billion reflecting the deterioration in these assets.

The HCR ManorCare division is no longer profitable. The division is not able to cover its fixed payments. Fixed Charge Coverage Ratio over the last 6 months is at 0.97x. Anything below 1 means fixed charges are not being covered. The ratio was likely significantly lower in the 4th quarter.

According to HCP’s management, the 4th quarter is supposed to be an ‘up’ quarter for HCR ManorCare (emphasis added):

Leave A Comment