Fed officials are hinting that the odds of December rate hike are edging up. Yesterday’s round of comments from several policymakers still leaves room for debate for deciding if squeezing monetary policy at next month’s FOMC meeting is a done deal. But compared with the remarks in recent months, the public chatter on Thursday had a hawkish tone, if only on the margins.

The crowd has certainly adjusted expectations for a rate hike next month. CME data at the moment shows that Fed funds futures are currently pricing in a roughly 70% implied probability that the central bank will pull the trigger in December and raise the target–slightly–above the current zero-to-0.25% range.

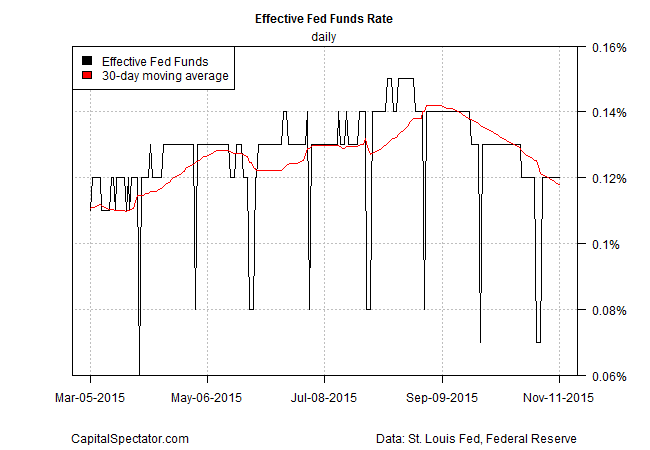

But if rates are due to rise, why is there no sign of the change bubbling in effective Fed funds (EFF)? After peaking in mid-September the EFF rate has continued to drift lower through Wednesday (Nov. 11). The 30-day moving average of EFF dipped just below 0.12%–the lowest since this past April. Presumably, EFF will start to inch higher in the days ahead if a rate hike is truly on the table.

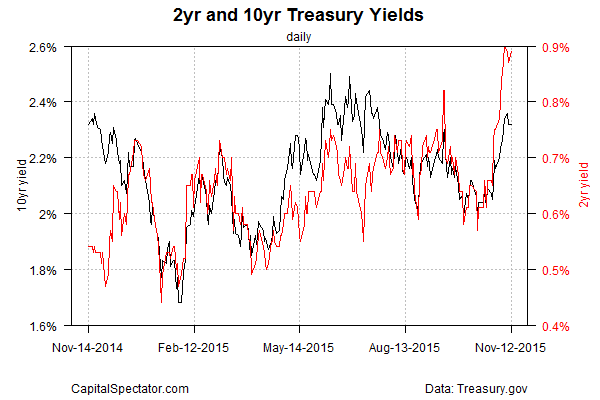

Meanwhile, the 2-year Treasury yield continues to hold on to its recent gains, based on daily constant maturity data from Treasury.gov. Considered the most sensitive spot on the yield curve for rate expectations, the sharp rise in the 2-year yield this month to 0.89% on Thursday–close to a five-year high–is a clear sign that the market’s pricing in higher odds of a rate hike.

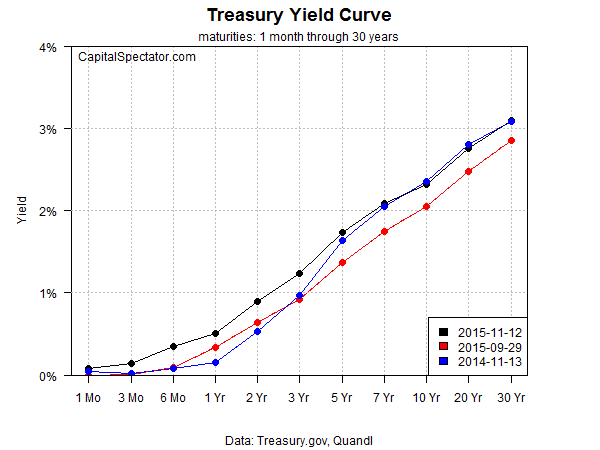

There’s also an upward bias across the yield curve generally compared with recent history. In the chart below, note the slight elevation in yesterday’s rates (black dots) vs. yields from 30 trading days previous (red dots).

No wonder that analysts are in near agreement that the Fed will announce a hike next month, according to The Wall Street Journal:

About 92% of the business and academic economists polled by The Wall Street Journal in recent days said they expected the Fed to raise its benchmark federal-funds rate at its Dec. 15-16 policy meeting. Some 5% said the Fed would stay on hold until March and 3% predicted the Fed would keep rates at near-zero even longer.

“It would take extraordinary market turbulence to knock them off course,” Wrightson ICAP chief economist Lou Crandall said. He, along with all but a handful of his fellow forecasters, predicted a December liftoff.

Leave A Comment