With gold surging on the back of the risk-off sentiment that swept through markets on Monday following North Korea’s latest nuclear test, it’s worth asking if everyone’s favorite inflation hedge, doomsday insurance, and shiny paperweight might be overbought.

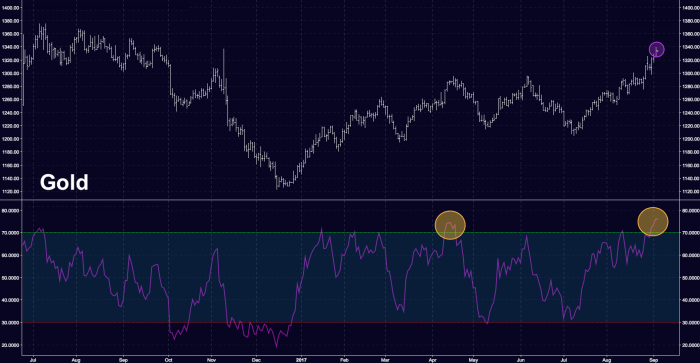

As Bloomberg’s Sebastian Boyd mused in a quick note this afternoon, “the RSI is suggesting that gold is overbought [and] the last time it looked like this was in April, before it lost 5.5% in a month.”

Again, part of the story here is that gold could get some of the haven flows that would normally go to the yen. Because if this gets bad – and reports that Japan is preparing plans to evacuate 60,000 citizens living in or visiting South Korea suggest it might – then investors will likely shun the yen in favor of bullion and the franc (because as far as we know, Kim isn’t firing missiles at Switzerland).

But there’s always a counterargument. “Gold is still just an inverse real yield play,” Mark Cudmore wrote last week, adding that “since most major central banks — such as the Fed and the ECB — are more likely to hike rather than cut rates as their next move, despite a lack of sustained inflation, it’s unlikely the next major move in real yields is going to be lower.”

[Aside: for more on this, see this post from our buddy Kevin Muir, The Macro Tourist]

Of course no one is thinking about that when the H-bombs are being tested and when the ICBMs are screaming by overhead. And indeed, another quote from the same piece by Cudmore sounds rather ominous in retrospect. To wit:

There’s just a U.S.-centric negativity weighing on the dollar, U.S. yields and stocks — it’s all about Trump, the debt ceiling and the Fed balance sheet, and nothing to do with North Korea. Yet.

So that was five days ago. And “yet” came on Sunday.

We’ll leave you with an excerpt from the latest note by SocGen’s Kit Juckes:

Leave A Comment