There’s something peculiar about the “yeah, but it’s all tech” market meme.

We’re guilty as charged when it comes to perpetuating the idea that tech is largely responsible for a disproportionate share of all the good things happening in markets. Just yesterday, for instance, we noted that equities’ resilience in the face of the junk bond rout looks to be attributable to tech just not caring.

But saying “everything is terrible if you strip out all the things that aren’t terrible” is no more a valid proposition than the opposite – i.e. saying “everything is great if you just strip everything that isn’t great.” The latter is something that gets bandied about all the time and indeed it’s a go-to quip for those who are inclined to be perpetually cynical.

Of course what’s good for the goose is good for the gander, so if you can make fun of people who paint a rosy picture by lampooning them as purveyors of the “everything is great if you strip out all the things that aren’t great” line, well then you can similarly lampoon the pessimists by pointing out the fact that they insist on saying “everything is terrible if you strip out all the things that aren’t terrible.”

The point: it’s not entirely fair to say “yeah but it’s all tech” because to a certain extent, that’s like saying “if you ignore what’s going well, nothing is going well.”

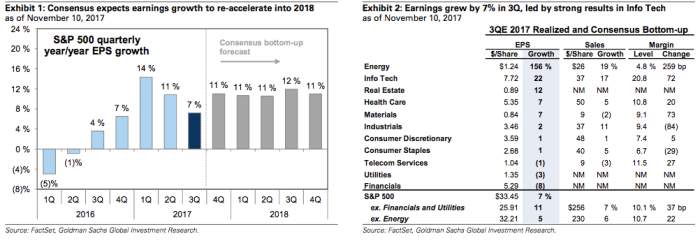

That said, you don’t want to simply put on the proverbial blinders when it starts to seem like one sector is shouldering a disproportionate share of the burden. First consider this 30,000 foot take on Q3 earnings season from Goldman:

S&P 500 earnings grew by 7% in 3Q, the latest piece in a mosaic showing an extremely healthy operating environment for US corporates.

3Q earnings growth was supported by both solid sales growth and rising margins. S&P 500 revenues increased by 7% as six of eight sectors grew the top line in the quarter, helped by a 2% year/year decline in the trade- weighted USD. Margins expanded by 37 bp to an all-time high of 10.1%. Most sectors expanded profit margins, led by increases in Energy (5%, +259 bp), Materials (9%, +73 bp), and Info Tech (21%, +72 bp; see Exhibit 2).

Leave A Comment