Shares of cable operator Charter Communications (CHTR) have been on a roll lately, rising more than 50% during the last 12 months. You would think after such a big run that the company must have had a dramatic change of fortune, but really it is just a traditional cable company offering customers bundles of services while consolidating smaller regional competitors.

The story might sound a lot like Comcast (CMCSA) because they are pretty much in the same business. Comcast owns NBC Universal, so they have a content wing as well, but the two companies are the nation’s leading cable businesses in the United States, with nearly half of all U.S. households (~50 million residential customers cumulatively).

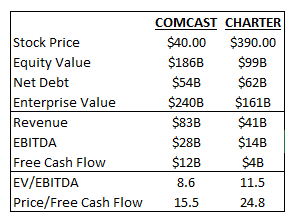

Investors would therefore likely conclude that Charter and Comcast were being afforded similar public market valuations, but you would be wrong. After Charter’s magnificent rise from $250 to nearly $400 per share (during which time Comcast shares have risen a more modest 20%), the smaller player now trades at a huge premium.

As the chart below shows, Charter fetches a 35% premium on EBITDA and a 60% premium on free cash flow:

It appears that merger chatter involving Charter may be behind a large part of the stock market move lately. Verizon (VZ) and Sprint (S) are both rumored to be eyeing a deal that would morph them into more than a cell phone provider, and perhaps adding wireless to the cable / internet / landline phone bundle would bring down costs and prove synergistic.

What investors seem to be missing, however, is that there is nothing unique about Charter’s business. The company still gets 40% of its revenue from cable video services, which are declining due to cord-cutting. The only strong business segment is broadband, which accounts for about 35% of revenue, but there is a limit there too. Population growth has slowed dramatically in the U.S. and offsetting cable losses by raising prices on internet service will only work for so long.

Leave A Comment