The roller-coaster ride in global markets in recent weeks has raised new doubts about economic growth in general and the case for a Fed rate hike this month in particular. But the resilience of key Treasury yields in recent days suggests that the bond market may be rethinking the case for the worst-case scenario that seemed inevitable over a few days last week. It could all reverse course in a heartbeat–especially if tomorrow’s employment report for August falls short of expectations for solid growth. Meantime, the rebound in US yields this week suggests that reports of optimism’s death may have been exaggerated.

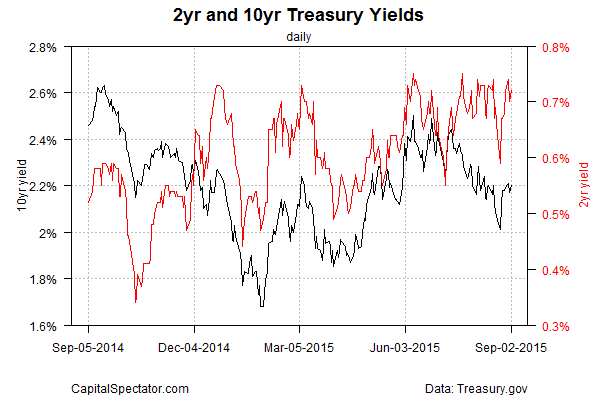

Or maybe it’s just another instance of the dead-cat bounce? We’ll know more in a few days. For now, the 2-year yield—arguably the most sensitive spot on the yield curve for rate expectations—has again moved close to a four-year high after a sharp drop in late-August. The 2-year yield ticked up to 0.72% yesterday (Sep. 2), based on Treasury.gov’s daily data–up from 0.59% on Aug. 24.

The benchmark 10-year yield is firmer this week as well, inching up to 2.20% yesterday. Although that’s still well below the roughly 2.50% mark seen earlier this year, the mild rise in recent days for the 10-year yield has reversed the previous slide that pushed the rate close to 2.0% at one point in late-August.

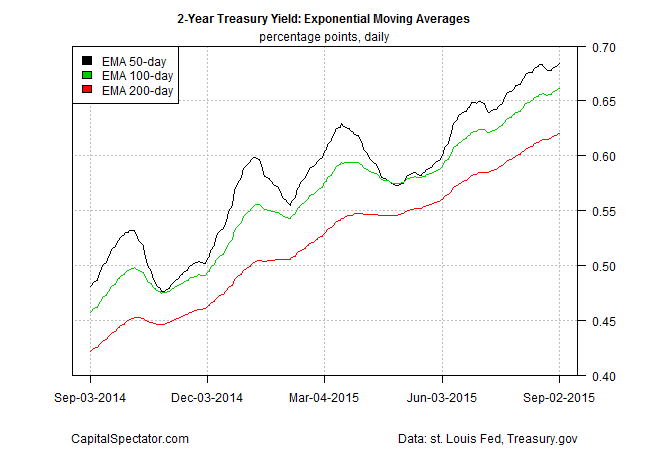

Looking at yields through a momentum filter—exponential moving averages (EMAs)—shows that the upside bias for the 2-year rate remains intact through yesterday.

The 10-year yield’s momentum, by contrast, is neutral to slightly negative at the moment, although it’s not yet clear if the recent reversal is temporary or the start of a new leg down.

In any case, the evidence for expecting trouble in the US economy remains a speculative forecast, based largely on weak markets of late. The economic numbers, on the other hand, still point to moderate growth, as yesterday’s ADP Employment report implied.

Leave A Comment