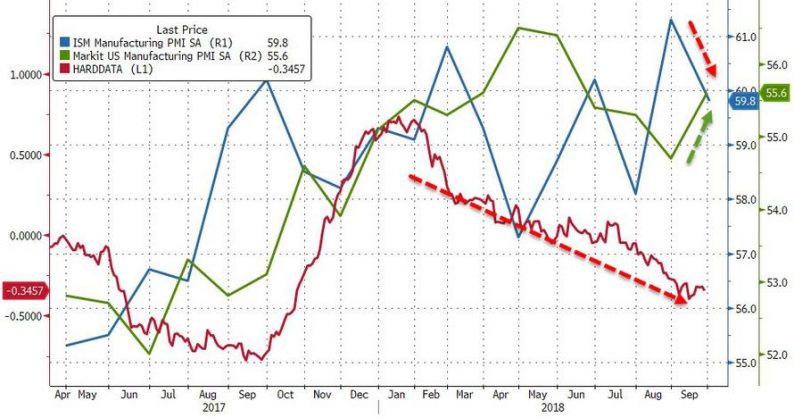

Following slight disappointment in Europe, and a collapse in Canada, Markit’s US Manufacturing PMI printed, as expected at 55.6 (highest since May) even as Services collapsed. ISM’s Manufacturing survey – which soared in August – was expected to drop, and did but more than expected (59.8 vs 60.0 from 61.3 in August)

Markit Manufacturing PMI rose from 54.7 to 55.6 (same as flash and expected level)

ISM Manufacturing fell from 61.3 to 59.8 (below expected 60.0)

Despite the ongoing slump in real ‘hard’ economic data, surveys continue to hope for the best…

The overall performance was driven by sharper rises in output and new orders, though new business from abroad continued to expand at only a marginal pace. Markit’s report shows employment drop to 53.6 vs 54.2 in August, the lowest reading since August 2017…

Chris Williamson, Chief Business Economist at IHS Markit said:

“US manufacturing showed resilience in the face of storms in September, with output rising at one of the fastest rates seen so far this year. New orders growth has lifted to the highest since May and is being boosted in particular by strong domestic demand, especially in consumer markets. In contrast, export orders grew only very modestly again.

“Worries about trade wars and tariffs continued to dominate, pushing business confidence in the outlook down to its lowest for a year.

“Tariffs, alongside higher oil prices, were meanwhile a key factor reportedly driving input costs higher. Almost two-third of all companies reporting higher input prices ascribed the increase to tariffs.

“Worries about the impact of tariffs on prices also led to increased incidences of stock building, exacerbating existing supply chain delays and driving prices further higher. Raw material inventories rose at one of the steepest rates seen this side of the global financial crisis.

“While stock building boosts current sales at suppliers it poses downside risks to growth in future months.”

Leave A Comment