As lenders stretch to find ways to lend more money and boost interest income in a time of rising funding costs, and as borrowers continue to overextend themselves, risky unsecured personal loans are soaring in popularity.

According to the WSJ, companies like American Express, Lending Club, and even Goldman Sachs are heading a charge of offering unsecured personal loans at a record pace. In the first half of this year, it was reported that these lenders mailed a record 1.26 billion solicitations for these types of loans – and the second quarter marked the first time lenders mailed out more solicitations for these loans than for credit cards. Credit cards are an overwhelmingly larger business.

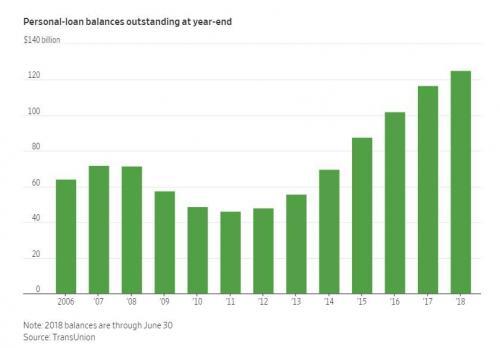

With many ordinary middle-class Americans increasingly seeing the inflation-adjusted incomes declining, it is hardly a surprise that the market for these loans is growing extraordinarily quickly: $81.9 billion in unsecured loans were extended during the first half of this year, a 13% rise according to data provided by Experian. This growth rate is outpacing most other forms of new debt: auto loans and leases, for instance, rose 9% over the same period of time.

The total size of the market is now just over $120 billion, or nearly double the peak reached during the financial crisis.

As the economy continues its “boom” and we push further into a decade-long credit cycle, lenders are starting to bear more risk and dole out these types of loans to less creditworthy individuals to try and keep interest payments coming in. This report follows an article we wrote just two days ago, noting that demand for commercial and industrial loans had suddenly tumbled.

After a period of surprisingly strong growth following the near contraction in early 2017, commercial bank C&I lending tumbled during the period July 11th to August 8th by $15bn, or 0.68% – the biggest 4-week decline since March 2017 and before that the aftermath of the financial crisis.

Leave A Comment