Besides the upcoming FOMC meeting on May 2-3, and French & Italian politics – the decisive runoff round of the French election takes place this Sunday – this week’s releases are dominated by US payrolls expected to come around 170k. The busy release calendar continues with Norges bank and RBA meetings as well as global manufacturing PMIs.

The market’s focus during the week of 5/1 will begin to shift away from the micro as the CQ1 earnings season winds down and back to the macro w/a slew of eco data and some central bank decisions scheduled (including the FOMC on Wed 5/3 and US jobs on Fri 5/5; also note that Yellen is scheduled to speak Fri after the jobs report at 1:30pmET). The eco data out this week could be crucial in helping to resolve the current debate around growth

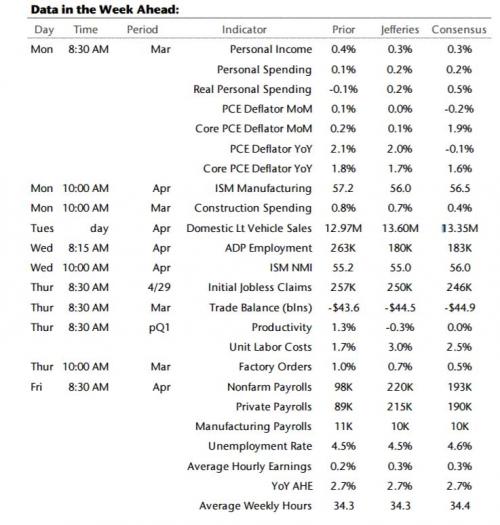

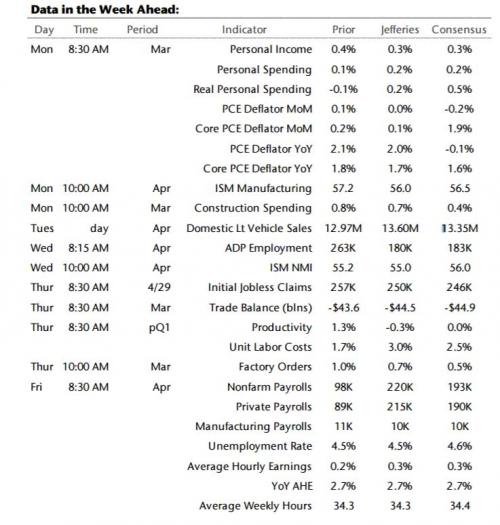

In the US, the data calendar will be very busy this week, highlighted by Monday’s personal income and spending data (including the PCE Deflators) and Friday’s April employment data. We expect solid income, modest spending, and relatively soft deflators, continuing the theme of very tame inflation data that we have seen over the past quarter. On employment, we expect a solid rebound in payroll growth following last month’s weather-induced disappointment and the overall tone will be consistent with the notion that the labor market is at or near full employment. Specifically, we also expect that AHE will rise on trend and that the unemployment rate will be unchanged at 4.5%. Rounding out the calendar, Wall Street expects modest declines in the ISM indexes, though both will remain at solid outright levels, a bump in auto sales following the March swoon, and solid construction spending as well.. In addition, there are several scheduled speaking engagements by Fed officials this week.

FOMC decision preview – the Fed statement on Wed (there won’t be a supplemental or Yellen presser) is expected to be pretty innocuous. JPM believes the Committee’s goal will be to acknowledge the softer run of data while still keeping June on the table as a live meeting. The bank continues to expect the Fed to hike rates at the June meeting, but does not think the statement will send a strong signal of impending action. Look for the statement to say that economic growth slowed early in the year, but to add that it is in part due to transitory factors. The second paragraph of the statement will continue to note that risks are roughly balanced.

Earnings preview – this week is another fairly big one for earnings with 131 S&P 500 companies and 85 Stoxx 600 companies reporting. Among the big names are Apple (Tuesday), BP (Tuesday), Facebook (Wednesday) and Shell (Thursday). As Jim Reid notes, we’ll see if they can continue what has been a decent start to earnings season to date. Indeed the trend so far is one of the strongest on record. In the US we have had reports from about 60% of the S&P 500 and 81% have beat at the earnings line, coming in 6.7% above consensus. This compares to the historical beat of 73% of companies and a median beat of 3.4%. This is made even more impressive by the fact that consensus estimates were not downgraded in the month leading up to earnings season compared to a typical 1% downgrade. He notes also that the results so far point to 15% EPS growth in Q1which is the fastest pace since 2011. Our European equity strategists note also that EPS growth of Stoxx 600 companies has accelerated to 23% with reported earnings being 13% above pre-season expectations.

Breakdown of key events by day from Deutsche Bank:

On Monday, with it being a public holiday in the UK, Germany and France among other countries today, the main focus will be on the US session where there are a number of important releases include the PCE core and deflator readings and personal income and spending reports for March, as well as the ISM manufacturing reading for April and construction spending in March.

Tuesday kicks off in Asia with the Japan services and composite April PMIs and Caixin manufacturing PMI in China. Over in Europe all eyes will be on the final April manufacturing PMIs as well as a first look at the data for the periphery and UK. The Euro area unemployment rate will also be released. In the US tomorrow the only data due out is vehicle sales in April.

Kicking things off on Wednesday will be Germany where the April unemployment numbers are due to be released. Shortly after that we’ll get Euro area PPI for March and then the advanced Q1 GDP report for the Euro area. In the US on Wednesday we’ll get the ADP employment change report in April and the final April PMIs and ISM non-manufacturing reading. Also on Wednesday all eyes then turn over to the Fed meeting.

In Asia on Thursday the early data is out of China with the remaining April Caixin PMIs. In Europe we’ll also get the remaining April services and composite PMIs as well as Euro area retail sales in March and UK money and credit aggregates data. In the US on Thursday the data includes initial jobless claims, Q1 nonfarm productivity and unit labour costs, March trade balance, March factory orders and the final revisions to March durable and capital goods orders.

Leave A Comment