The poor are getting poorer but the rich, it appears, are no longer getting richer. With apartment vacancies at 9-month highs, Bloomberg reports that Manhattan’s luxury-home market is rapidly losing its luster. Prices have been dropping every month since February, when they reached their highest point on record, and, as one analyst notes, “the downward trend in that decline hasn’t abated, and we haven’t seen it wavering in any way.”

apartment vacancies at 9-month highs,

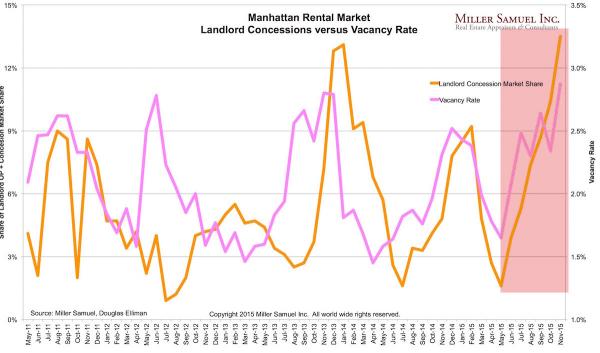

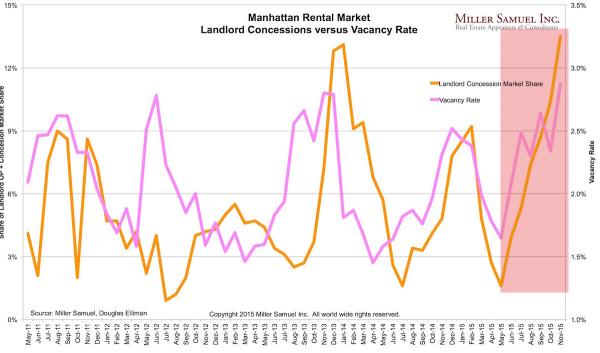

The vacancy rate in November was 2.87 percent, up from 2.31 percent a year earlier and the highest since August 2006, according to a report Thursday by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. Landlords eager to fill empty units lured tenants with the most concessions since 2011.

The rise in vacancies suggests tenants are reaching the upper limits of what they’re able to pay after more than four years of almost continuous rent growth, according to Jonathan Miller, president of Miller Samuel. In November, the median monthly apartment rent climbed 3.9 percent from a year earlier to $3,361. Leasing costs have jumped more than 18 percent since the end of the recession in June 2009.

“We’re reaching the point where things can’t go up as much,” Miller said in an interview. “The economics don’t make much sense anymore.”

“The conditions that are driving rents higher haven’t changed,” Miller said. “What’s changed is the acceptance of it, the affordability of it.”

The luxury-apartment market, the top 10 percent of all rentals by price, was the only category with a decline in prices. The median rent in November fell 1.4 percent to $8,537.

“Complaining about high rents in Manhattan is nothing new, but now it’s becoming more visceral to tenants,” said Miller, who’s been tracking the apartment market since 1991.

“We’re hitting the point where affordability is really becoming a much bigger issue than it has been in the past.”

Leave A Comment