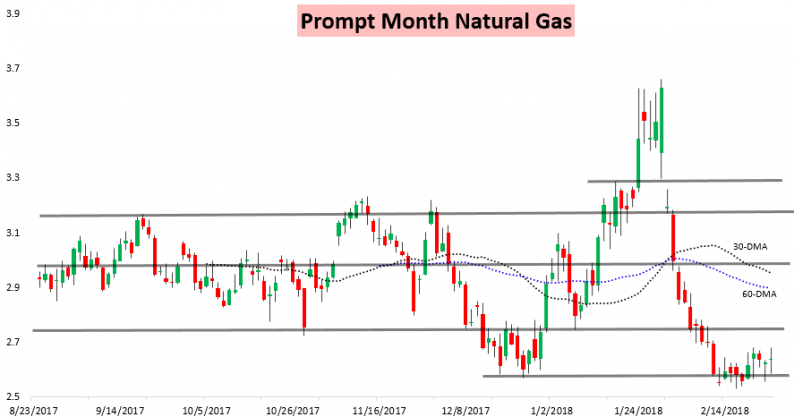

Upon becoming the prompt month contract, the March natural gas contract violently reversed in its first two days, selling-off heavily the ensuing two weeks. Yet on its expiry, it was much more tranquil; prices traded in a more narrow 9.4-cent day range today and settled only half a percent above where they did Friday.

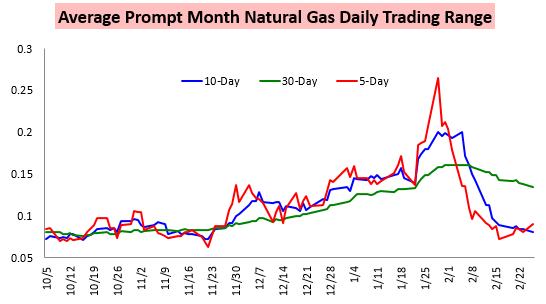

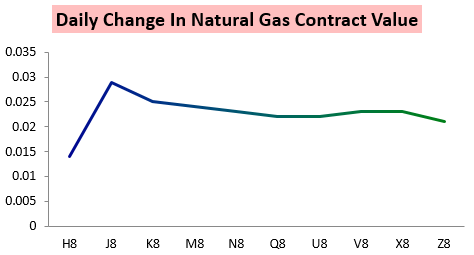

The March natural gas contract saw what amounted to a real crush of volatility. The average prompt month trading range plummeted.

The prompt month daily trading range, while being exciting to start February, has now fallen to the bottom of the historical range.

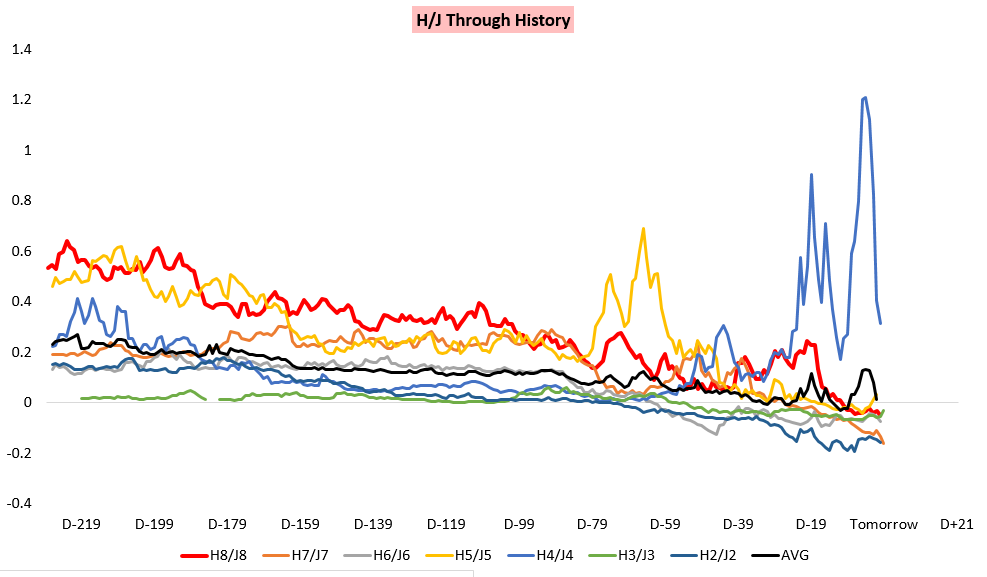

This came as H/J flipped into contango, with H/J expiring right in the middle of the past few years.

Today’s H/J decline came as much from gains with the April contract, which led the strip, as it did from March weakness into expiry.

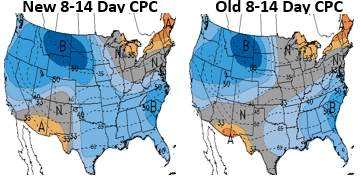

Much of this was thanks to another tick higher in medium and long-range cold risks on model guidance, as seen in today’s afternoon Climate Prediction Center update.

This is exactly what we warned clients in our Friday Pre-Close Update, where we expected model guidance to be more bullish to start this week than it was to end last week.

This verified the Slightly Bullish sentiment we had for clients in our Pre-Close Update overall as well.

Such sentiment carried over into today. Our intraday Note of the Day was published mid-morning after natural gas prices declined from the overnight rally. We saw cash weakness as primarily responsible for the decline, and in a number of updates had warned clients that afternoon model guidance today was likely to add some heating demand back. Sure enough, that occurred this afternoon, and prices were able to rally off their mid-morning lows.

This cash weakness is something we had been warning clients about since last week as well, as significant warmth across the country early this week will limit heating demand before the early March cold arrives.

Leave A Comment