The Man with the Inflation Plan

Proving beyond a shadow of doubt that Keynesian absurdity knows no bounds, Larry Summers has graced the FT – one of the West’s premier establishment propaganda mouthpieces advocating central economic planning as practiced by modern-day regulatory democracies – with yet another cringe-worthy editorial.

Larry Summers – it is probably no exaggeration to call the man a danger to civilization

Photo credit: Hyungwon Kang / Reuters / Corbis

The editorial is entitled “A world stumped by stubbornly low inflation” with a subheader reading “There is no evidence that policymakers are acting strongly to restore their credibility”.

The title and subheader alone deserve comment. First of all, absolutely no-one outside the inhabitants of the incestuous ivory tower of Keynesian and monetarist mainstream economists and the central planning bureaucrats infesting central banks is in any way “stumped” by “low inflation”.

We suspect that there are billions of consumers in the world who would prefer prices to stop rising altogether. In fact, we believe they not only want them to stop rising, they actually want them to decline. But what do they know? Mr. Summers and his central planning comrades have decreed that it is “bad” for them if they are able to buy more rather than less with their income!

As to the perceived lack of policymaker “credibility”: They don’t deserve any. The world’s economic malaise is to 100% their fault. If only it were true that they are “not acting”! The truth is unfortunately that they continue to heap folly upon folly.

Need we remind Mr. Summers of the Bank of Japan’s decision to implement the perversion of negative deposit rates, or the decision of the Riksbank to lower its negative rates to minus 50 basis points in the middle of a raging housing and consumer credit bubble, even though Sweden’s GDP is forecast to grow by 3%?

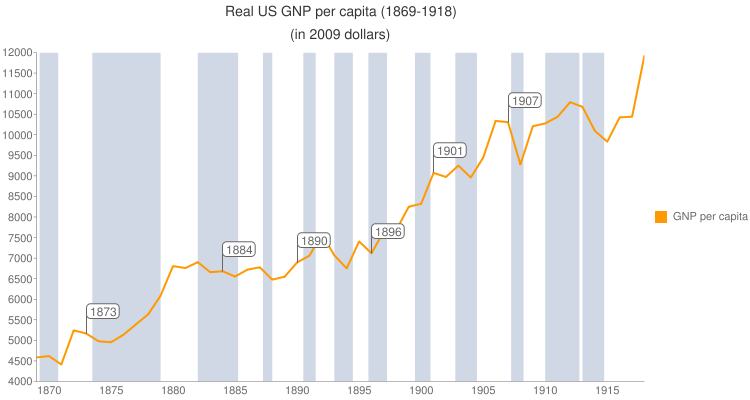

In an unhampered free market economy, mildly declining prices would be the rule, not the exception. In fact, the time period during which the US experienced the by far largest real economic growth per capita in history was one during which consumer prices steadily declined.

1869 – 1918 – the by far biggest and most equitable increase in US real economic output per capita in history was recorded in this time period. There was no Federal Reserve and government was but a footnote in most people’s lives. Federal spending amounted to less than 4% of GDP by 1910. People used sound money and a steady, mild decline in consumer prices took place – click to enlarge.

Mr. Summers urgently needs to familiarize himself with Hayek’s 1928 critique of the theories of two of the intellectual forebears of Keynes, the US-based economic cranks William Foster and Waddill Catchings. Hayek showed clearly that real economic growth has neither anything to do with spurring consumption spending, nor does it require any “price inflation”.

However, this insight requires one to understand capital theory, and to recognize that capital is heterogeneous and not a homogeneous, self-generating blob. It requires one to understand the inter-temporal interplay between saving, investment, production and consumption.

With respect to so-called “inflation” – the term originally designated an increase in the money supply. This definition is also the only one that makes any sense – both semantically and in terms of economic theory.

Inflation (in its original meaning of monetary inflation) has numerous possible effects. An increase in the prices of consumer goods is only one of these possible effects, and by no means the most pernicious one. What inflation invariably does cause are changes in relative prices in the economy.

This has far-reaching consequences, of which two of the most prominent ones are wealth redistribution (in practice largely from the poor to the rich) and the falsification of economic calculation. This in turn leads to capital malinvestment and the boom-bust cycle. In other words, these are ultimately the things of which Mr. Summers thinks we ought to have more of!

With regard to the change in the meaning of the term “inflation”, Ludwig von Mises notes in Human Action:

Leave A Comment