This morning’s overnight dead-cat-bounce is once again being heralded as the beginning of the end of the carnage that investors have suffered in October. We’re not holding our breaths…

“Should we buy the dip?” “Has it gone far enough yet?” As former fund manager and FX trader Richard Breslow notes, those seem to be everyone’s favorite question.

Obviously, the first things that jumps to mind are equities. But the oil and currency folks are asking as well. And for all the talk about how muted the fixed income response has been to the share price melt-down, you can be sure that bond and credit traders want to know the answer as well.

Via Bloomberg,

This week brings to a close a month that certainly didn’t work out as expected. But it is doing it in style. Lots of economic news, some central bank meetings where no policy changes doesn’t mean bereft of meaningful information and a bunch of assets sitting at levels that are potentially important crossroads. Wouldn’t it be ironic, but somehow fittingly apt, if assets that failed to proportionately move with equities did so just when the stock indexes decided to bounce. Or shares bounce just when everything else begins to flash caution.

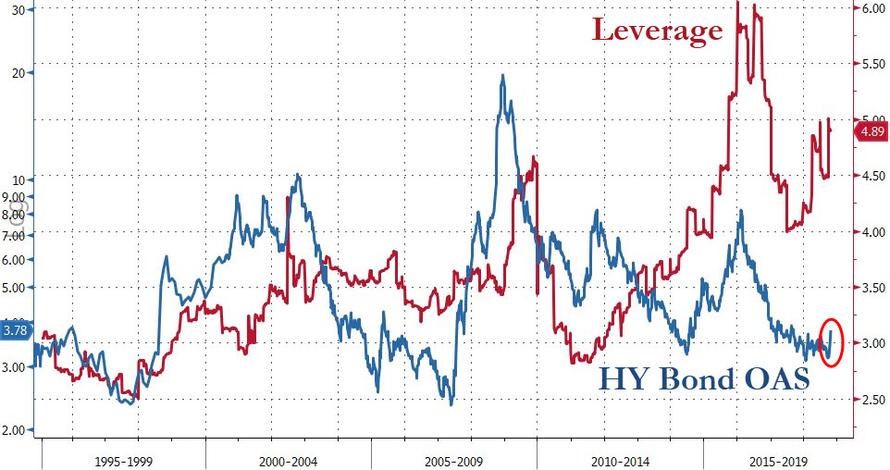

Credit, despite high corporate leverage, had been remarkably tame.

How can a business cycle end if there are no obvious signs of stress in this sector? Which is why it’s worth keeping an eye on both the investment grade and high-yield Markit CDX indexes.

Both of these measures of credit-default swap prices are in play and look like they are attempting to see how strong are their resistance levels. And both made year-to-date highs at the end of last week. They are near resistance, not clear of it. Risk premia demanded from bonds in these sectors are most assuredly getting pricier. But they’ve had false break-outs before.

Ten-year Treasury yields back below 3% would be a problem. We all know that. And there seems to be a creeping resignation that it is only a matter of time.

Leave A Comment