October was at it again last week. After Wednesday’s close, the S&P 500 Index, Dow Jones Industrial Average and small-cap Russell 2000 Index had all erased their gains for 2018, while the tech-heavy Nasdaq Composite dipped into correction territory.

I don’t believe there’s any single cause for the selloff. Investors are simply nervous, thanks to rising interest rates and the upcoming midterm elections, among other things.

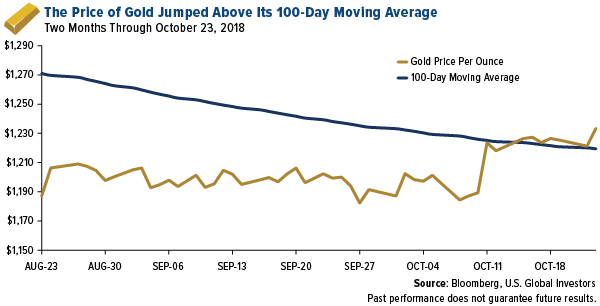

Meanwhile, gold performed precisely as we would expect it to. The price of the yellow metal jumped above its 100-day moving average, a bullish sign that could mean further moves to the upside if market volatility persists. On Friday, gold was trading at a three-month high of $1,246 an ounce.

So can we expect additional volatility going forward? In a recent note to investors, Citibank says it estimates that “some more volatility is likely through December” due to the impact of trade disputes on growth, rise in U.S.-Saudi Arabia tensions and Brexit stalemate. Analysts point out, though, that the present slowdown doesn’t necessarily signal the end of the historic bull market. Compared to the start of the previous two bear markets, in 2000 and 2007, only four out of 18 factors are flashing “sell” right now on Citi’s “bear market checklist.” Among those factors are overinflated global equity valuations, a flattening yield curve and high debt levels.

The bull is “tripping, not dying,” Citi says.

But Is It the End of “Buying the Dip”?

The bull market might not be dead, but we could be facing the end of “buying the dip.” According to a report last week by Morgan Stanley, buying the S&P 500 after a week of negative returns was a profitable strategy from 2005 through 2017. That may no longer be the case, as you can see in the chart below. Buying the dip in 2018 has resulted in an average loss of around 5 basis points.

Leave A Comment