Last week, Crude Oil tumbled despite the huge decline in the US Crude Oil Inventories, which posted the biggest weekly decline since September of last year. Crude Oil prices ignored these figures and continued to decline further.

Brent touched $50, and WTI slid to 46.50’s. Some OPEC reports came out, and that led to a notable rally. Brent closed the week higher by more than 3% on Friday, and WTI added around 2%.

So What’s Happened?

As we noted many times before, OPEC was on radio silence until the price of Brent started to slide below the $50, which is now seen as a key support.

They came back to the market with some remarks, increasing the hopes for new measures in the coming weeks/months.

OPEC said that the commitment ratio is now around 95%, which makes more sense than the previous ratio when it was over 100%, as OPEC production has been rising for the past three months.

OPEC also noted that they would meet in November, and in this meeting, they will decide on either to continue with the current deal or to stop it.

Why would they stop the deal right now or even in November, while the prices are still nearing this year’s lows? No one knows, but it’s an attempt to keep the markets wondering what might happen in November.

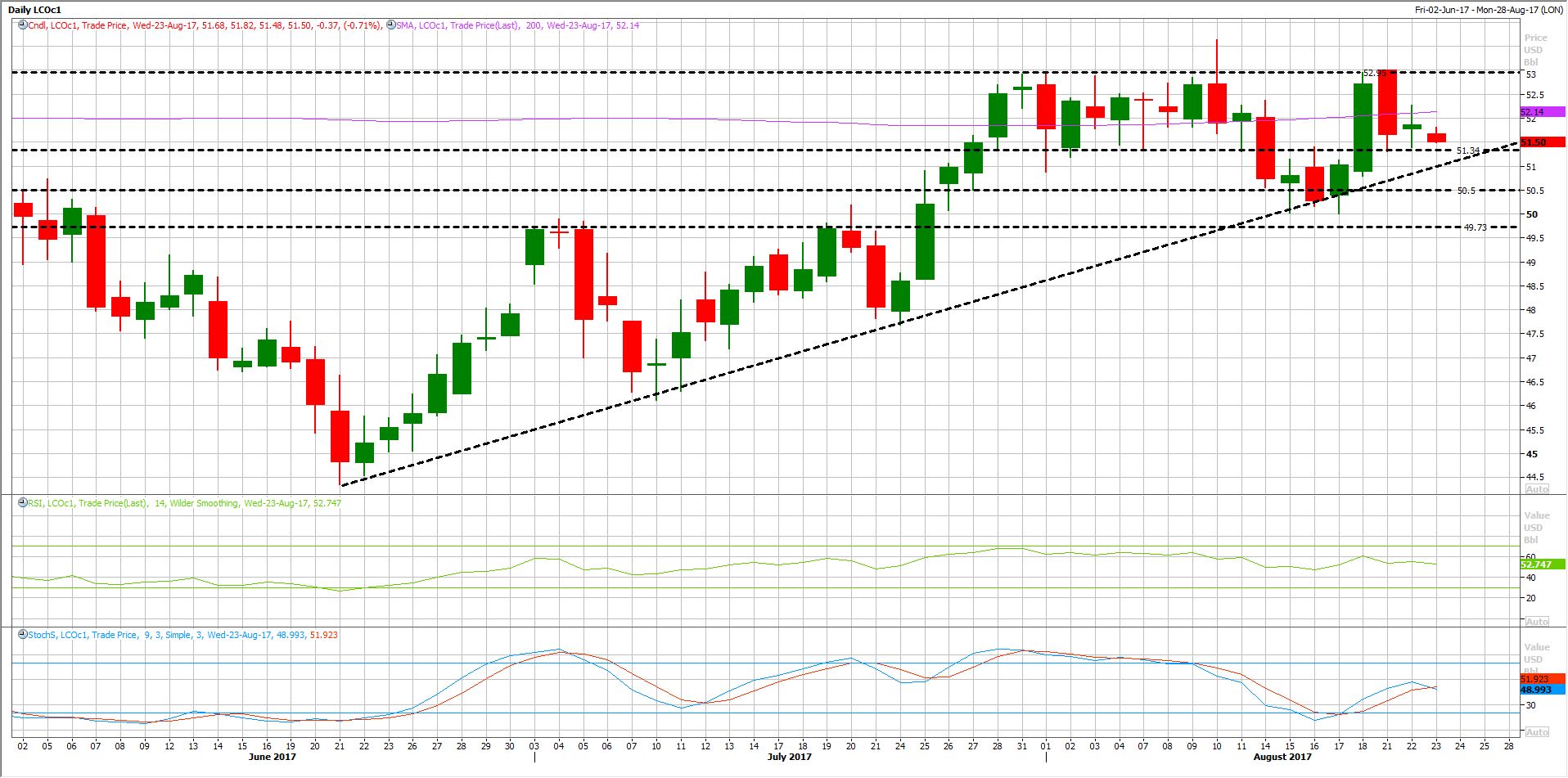

Keep An Eye on Brent At $50

As noted before, the $50 represents a solid and key support for the market and for the producers at the same time.

Since the beginning of this week, Brent has been trading within a tight range, between 53 and 50 with no clear break above or below those levels.

At the same time, traders need to keep an eye on the daily trend line as shown on the chart above, which stands around 51.0, as a break of which would clear the way for further declines, probably toward 50.50 first followed by 50.0 and 49.70’s.

The technical indicators are already crossed over to the downside, which keeps a high possibility for another leg lower ahead.

Leave A Comment