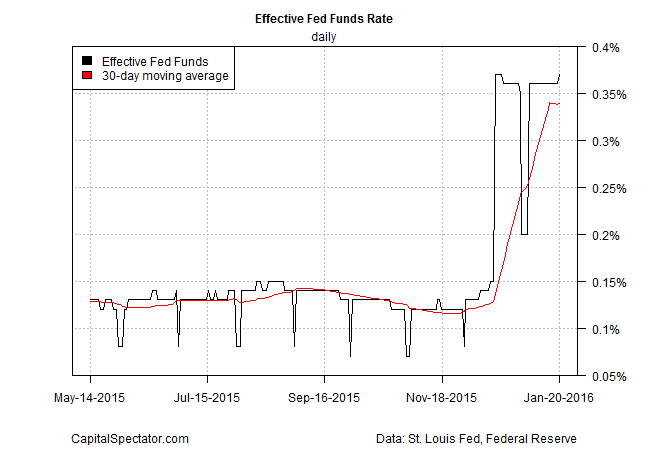

A Fed rate hike at a time when economic worries are on the rise? Fugetaboutit! In fact, some analysts are talking up the possibility that the central bank may be forced to back-track and reverse last month’s subtle but symbolically important 25-basis-point rate hike—the first since 2006. Perhaps, but there’s no sign of an imminent retreat in the effective Fed funds rate (EFF), which ticked up to 0.37% on Wednesday (Jan. 20)–the highest in a month. That’s an interesting talking point with next week’s Fed meeting on the radar.

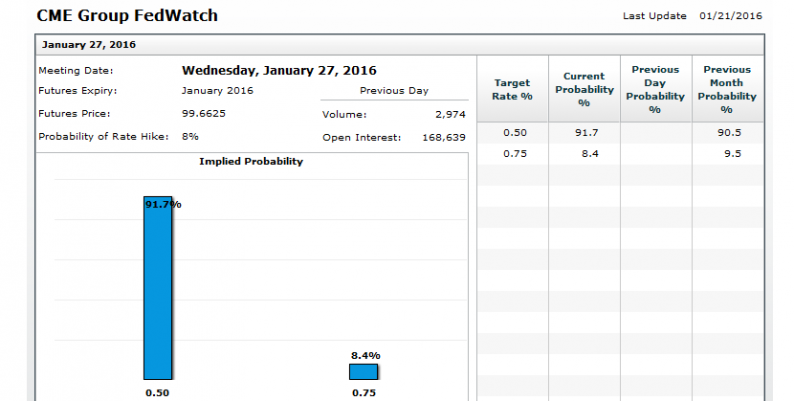

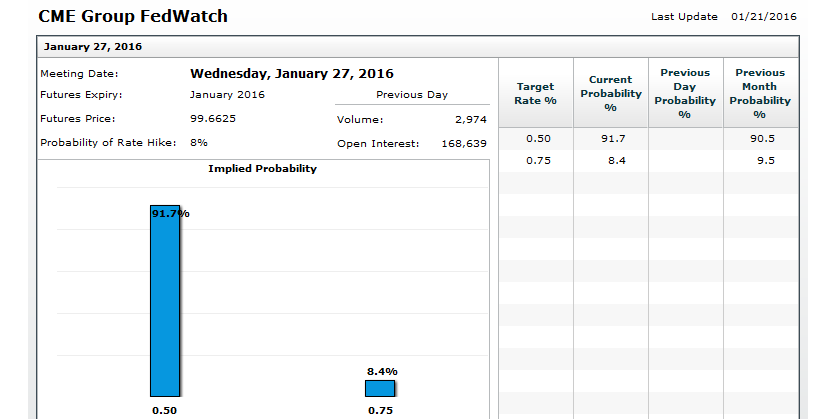

Will the Fed raise interest rates at the Jan. 27 FOMC meeting? Unlikely, according to Fed funds futures. The implied probability that the monetary mavens will boost the target rate above its current 25-to-50-basis-point range is less than 9%, according to CME data for Jan. 21.

But while it’s not obvious that Janet Yellen and company are set to push the target rate higher, EFF’s latest move doesn’t hint at easing either. In short, the status quo is a reasonable bet, based on the numbers in hand.

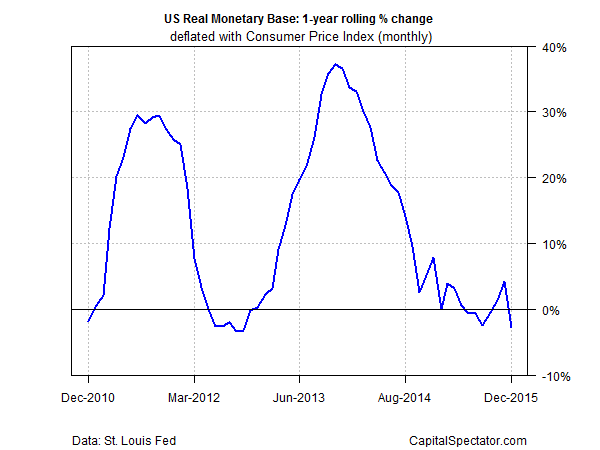

In fact, monetary policy from the 30,000-foot-level continues to look mildly hawkish. The real (inflation-adjusted) monetary base (M0) ticked lower last month, dipping 2.8% vs. the year-earlier level. That marks the deepest decline in three years, although recent history makes it easy to set new records on this front given the generally huge increases in money supply. In any case, the latest numbers suggest that the Fed was front loading a modest squeeze in policy at last year’s close. But a lot has happened in the new year, at least in terms of market perception.

As hawkish monetary history goes, M0’s current profile is relatively trifling, of course. Nonetheless, students of economic history will note that the troubling sight of policy tightening at a time when the US macro trend is looking shaky, as discussed in yesterday’s business-cycle review. We’ve seen this movie before, or at least variations of the narrative. Is history repeating? It’s too soon to say, although there’s no monetary smoking gun at the moment via the Treasury yield curve, which remains positively sloped. What’s more, the case is still weak for arguing that the US has slipped into a new NBER-defined recession—based on a broad set of indicators through last month.

Leave A Comment