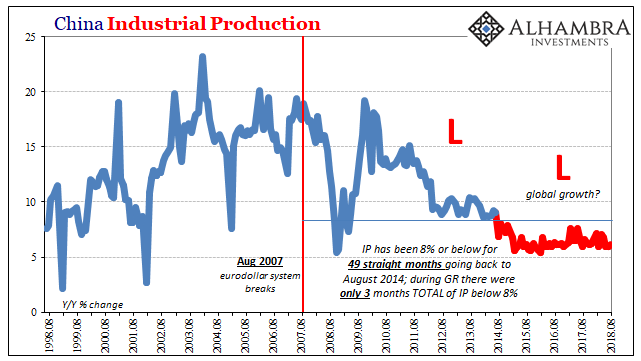

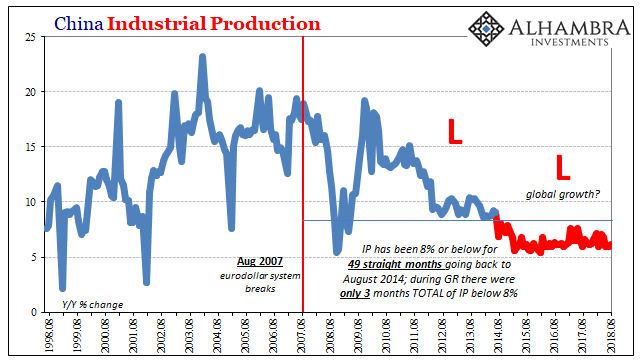

It’s no longer possible to know what state Chinese industry may be in. This is no small matter. Industrial production in China is the bedrock of economic growth throughout the rest of the world. Without it, there really isn’t anything left to do but struggle. And since industry’s performance there is predicated on demand in the Western world, this is the middle of everything.

According to China’s National Bureau of Statistics, Industrial Production is a six. What that six might mean is increasingly open for interpretation. Ever since August 2014, a span encompassing 49 months in total, Chinese IP has been at 8% or less. It’s never been like this in modern China. Of those four-plus years, 42 months straight have been fixed right around 6%. To write that it’s unusual for any statistic is one of those Hall of Fame understatements.

There have been a few months where IP has been less than 6%, as well as the occasional one at around 7%. Out of those 42 months, IP has been within 0.3% of 6% on either side in 27 of them. There is no longer variability in the figure, and that’s just not normal. In August 2018, Industrial Production was up 6.1% after rising 6.0% in both June and July.

What that proposes is how IP is showing us the best case for China’s underlying true industrial condition. For an upper boundary, this isn’t very good at all (which suggests why it may be at 6%). There is a reasonable probability that especially manufacturing is faring materially worse than the projected official rate.

It is the idea of rebalancing that pushes this question about industry back into the spotlight. Many years ago, as China’s economy slowed “unexpectedly” the idea was put forward the Chinese economy could survive and even thrive without an actual recovery in the West. It was at first dismissed because how could there be no recovery in the US and Europe with the dream tickets Bernanke/Yellen and Trichet/Draghi?

Leave A Comment