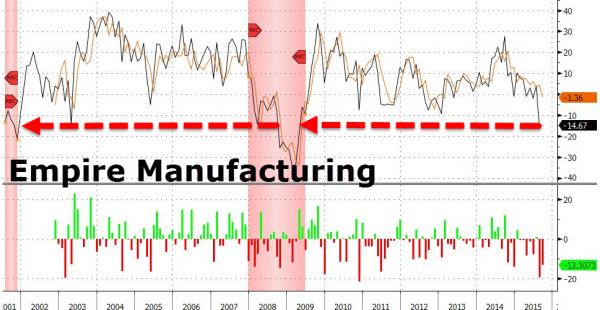

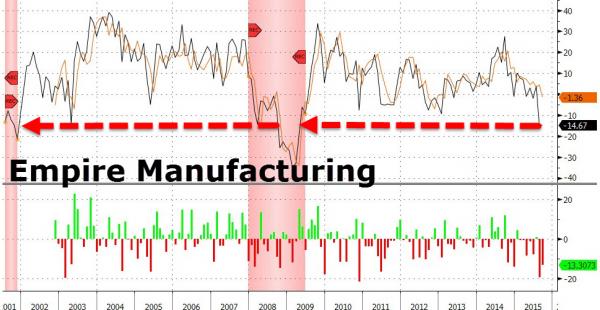

Despite some strangely optimistic expectation of a -0.5 print, September Empire Manufacturing printed -14.67, showing absolutely no hockeynesian dead-cat bounce mean-reversion. Hovering at the worst levels since April 2009, the underlying data is a total disaster. New Orders remain firmly negative and inventories collapse (who could have seen that coming?), and even more concerningly, employment and average workweek plunged into negative territory for the first time in over a year.

The read through the inflation outlook and for jobs – non-hamburger flipping jobs that is – from this report was simply abysmal:

Price changes were quite modest. The prices paid index slipped to 4.1, its lowest level since the Great Recession. The prices received index dipped below zero, falling six points to -5.2 in a sign that selling prices declined. Labor market conditions worsened,

with declines in employment levels and hours worked. The index for number of employees fell below zero for the first time in well over two years, slipping eight points to -6.2, and the average workweek index dropped to -10.3.

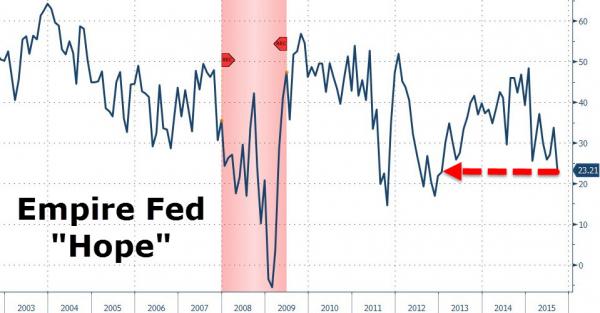

There was no silver lining pretty much anywhere in either the 6 month outlook or the current conditions:

Worst of all: the optimism is now gone. From the report:

Indexes for the six-month outlook displayed less optimism about future conditions than in August. The index for future business conditions fell ten points to 23.2.

Indexes for expected new orders and shipments dropped to similar levels, and the indexes for both future prices paid and future prices received declined. The index for expected number of employees edged up to 7.2, while the index for future average workweek turned negative. The index for expected capital expenditures fell six points to 11.3, and the technology spending index dropped to 2.1, indicating that tech spending plans were essentially flat.

Simply put, this report suggests total carnage in the manufacturing sector and, just as we have pointed out (most recently here and here), the exuberant inventory over-accumulation of the past few years – from Fed-deluded malinvestment – is about to come crashing down.

Leave A Comment