There are many investing strategies and principles that retired investors can utilize to reduce the risk associated with investing in equities (stocks) for their retirement portfolios. Choosing to invest in the highest quality stocks your mind can conceive sits at the top of the list. There are many components that investors can analyze and examine to determine whether a company is high quality or not.

The primary determinant of high quality is superior financial strength. Financially strong companies possess the staying power and resources to weather the occasional bad storms that will inevitably occur. Every business will on occasion face challenges and difficulties. Meeting those challenges requires a strong balance sheet and an adaptive and competent management team to guide the company across troubled waters.

Evaluating financial strength can be accomplished through the examination of a few simple but important fundamental metrics. Fortunately, much of that work is already done for us by established and reputable reporting agencies such as Standard & Poor’s, Value Line, MorningStar, etc., in the form of credit ratings.

There are many available sources where retired investors can find that information. The key is to look for companies that are awarded what is referred to in financial circles as investment-grade ratings. Typically, the companies with the best ratings will have a capital A or better in their credit rating.

Retired investors concerned with safety can dig deeper by examining important fundamentals such as cash flow, free cash flow and debt levels. Stated overly-simplistically, you will be looking for companies that have the strength of cash flows to support debt payments and current and future dividend distributions. Regarding safety considerations, cash flows are more relevant than earnings. Because when it comes to the survival of a business, cash flow is king. As it relates to safety, a business surviving as an ongoing concern is the last line of defense.

Additionally, when it comes to determining the safety associated with investing in a stock, determining whether it possesses superior financial strength is an obvious and commonly-utilized approach. However, there are additional important safety measurements that are more subtle, less understood and often either ignored or their importance not given the credit deserved.

These more subtle safety measurements are an above average, but sustainable, current dividend yield and sound valuation, or better yet, significant undervaluation. The remainder of this article will examine the financial strength and these two important but more subtle safety measurements as they apply to the much-maligned blue-chip stalwart IBM (IBM).

IBM’s Financial Strength

IBM was founded in 1910, and Incorporated in the state of New York in 1911. The company took on the iconic IBM name in 1924. Consequently, IBM has been an American technology stalwart even before technology became cool. As such, IBM has been long-renowned as a blue-chip dividend growth stock. So much so that legendary investor Peter Lynch once quipped “no one ever gets fired for buying IBM.”

Here are IBM’s Credit Ratings from 3 Reputable Sources:

Standard & Poor’s: AA-

MorningStar: AA-

Value Line: AA+

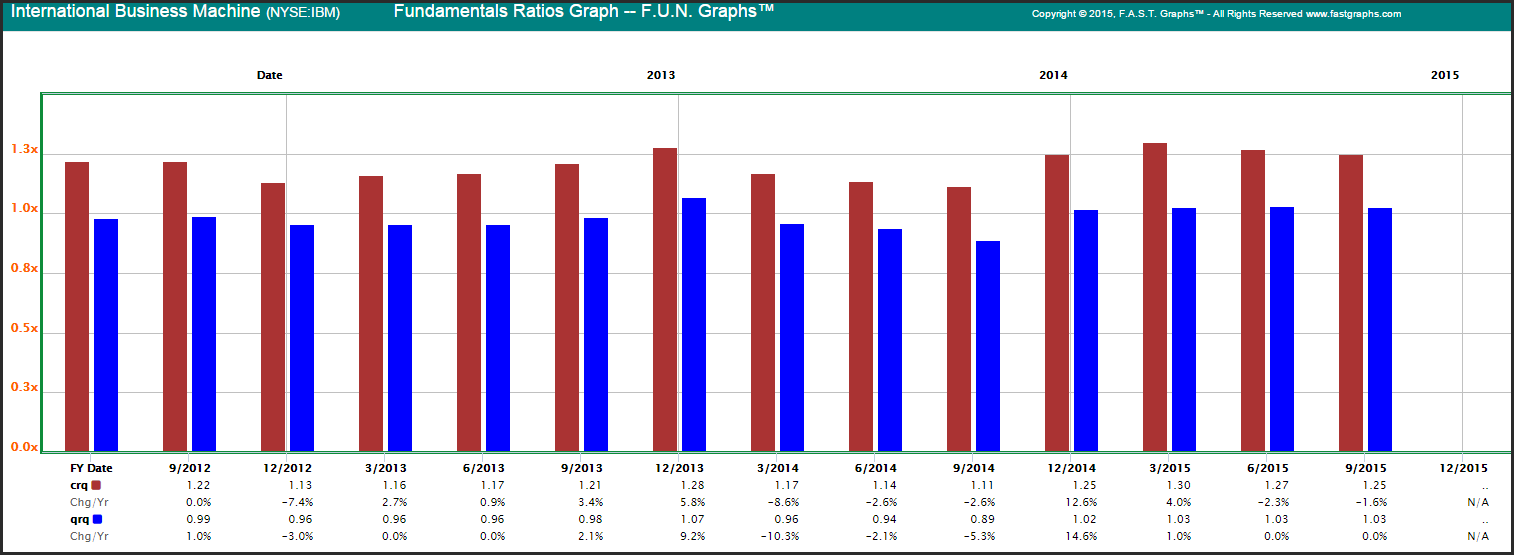

IBM Liquidity Ratios

IBM’s current ratio (crq) is and has been above 1, indicating that the company is fully capable of paying its obligations. IBM’s quick ratio (qrq) also supports its ability to meet short-term obligations. Importantly, both of these ratios continue to remain within IBM’s historical norms.

IBM’s Dividend Yield, Record and Sustainability

In the title of this article I sarcastically included the phrase “it’s about the income stupid.” However, I was not merely attempting to be sardonic, because that phrase represents a significantly important principle about investing in large blue-chip dividend growth stocks. Regardless of whether you’re investing in revered blue chips such as Johnson & Johnson (JNJ), Procter & Gamble (PG), Coca-Cola (KO), or IBM etc., it would be naïve on your part to believe you will automatically or always outperform the market on a total return basis.

Behemoths such as those described above have simply become too large to grow fast. Their primary appeal derives from their safety characteristics and the dividend income they have produced in the past, and are capable of providing in the future. In this regard, it would not be naïve to believe that these blue-chip dividend stalwarts might produce significantly more future dividend income than the general market, because in truth and historical fact, they all have – IBM included.

Leave A Comment