Apple Inc. (Nasdaq: AAPL) generated an excellent return on equity of 37.1% over the past twelve months, while the Information Technology sector returned 3.8%. While Apple’s performance is highly impressive relative to its peers, it’s useful to understand what’s really driving the company’s strong ROE and how it’s trending. Understanding these components may change your views on Apple and its future prospects.

Apple’s Return On Equity

Return on equity represents the percentage return a company generates on the money shareholders have invested. Return on Equity or ROE is defined as follows:

ROE = Net Income To Common / Average Total Common Equity

In general, a higher return on equity suggests management is utilizing the capital invested by shareholders efficiently. However, it is important to note that ROE can be “manufactured” by management with the use of leverage or debt.

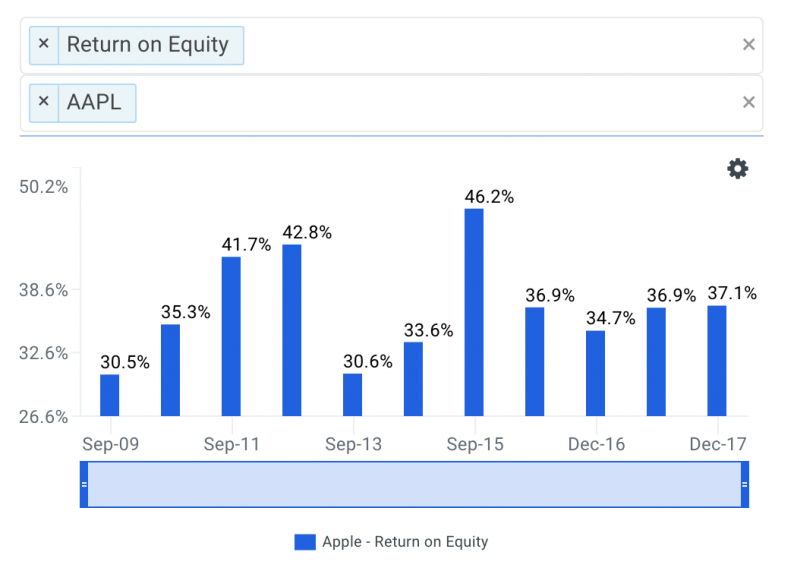

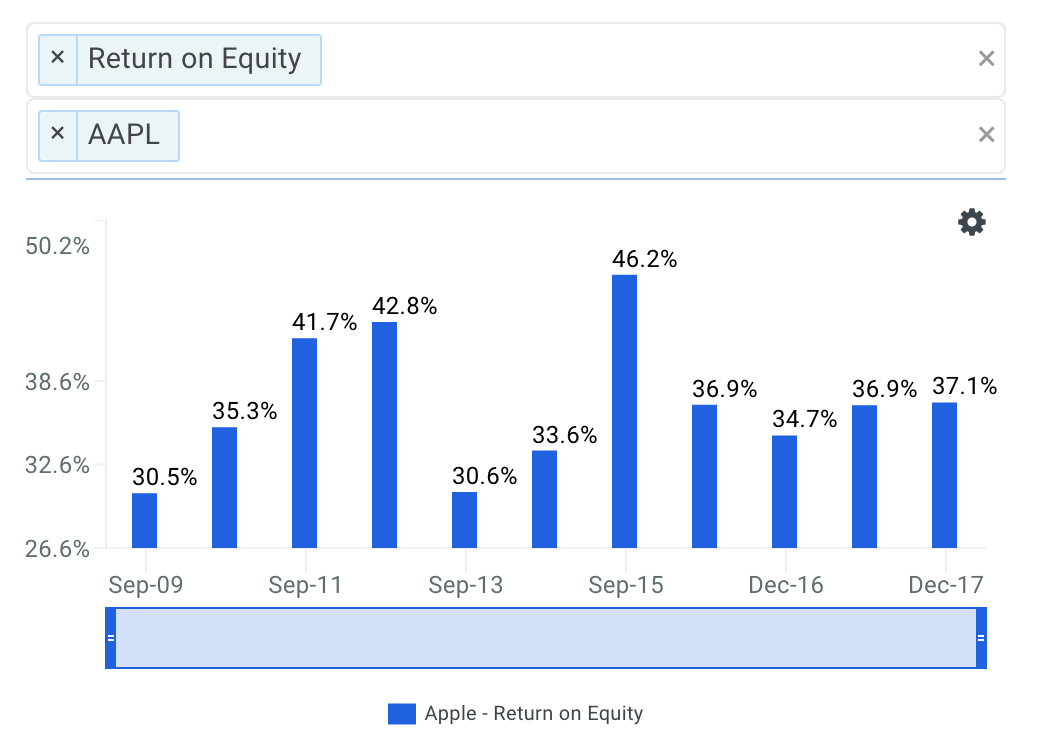

Apple’s historical ROE trends are highlighted in the chart below.

source: finbox.io data explorer: ROE

The finbox.io data explorer: ROE of Apple has generally been declining over the last few years. ROE decreased from 46.2% to 36.9% in fiscal year 2016, stayed there in 2017 and slightly increased to 37.1% as of LTM Dec’17. So what’s causing the general decline?

I break down what’s driving Apple’s ROE using finbox.io’s DuPont model.

What’s Driving Apple’s Declining ROE?

The DuPont analysis is simply a separate way to calculate a company’s ROE:

ROE = Net Profit Margin * Asset Turnover * Equity Multiplier

Created by the DuPont Corporation in the 1920s, the analysis is a useful tool that helps determine what’s responsible for changes in a company’s ROE. It highlights that a firm’s ROE is affected by three things: profit margin, asset turnover, and its equity multiplier or financial leverage.

Analyzing changes in these three items over time allows investors to figure out if operating efficiency, asset use efficiency or the use of leverage is what’s causing changes in ROE. Strong companies should have ROE that is increasing because its net profit margin and/or asset turnover is increasing. On the other hand, a company may not be as strong as investors would otherwise think if ROE is increasing from the use of leverage or debt.

Leave A Comment