Fed Hikes; Silly Myths about Interest Rates & Gold Persist

The Fed finally acted this week – upping its benchmark Federal Funds rate by 0.25%. Now that the speculation over whether the Fed will hike has been put to rest, analysts are busily speculating about what the Fed’s move means for the economy and markets.

Many of these speculations are unfounded. It’s time to bust some silly myths.

Much of what’s spewed out in the financial media concerning interest rates is flat-out wrong, especially when it comes to their impact on precious metals markets. Since gold and silver are small markets compared to bonds and equities, some “analysts” apparently think they don’t need to do actual research on precious metals markets before commenting on them. It’s easier to regurgitate oft-repeated myths about rising rates being bad for gold than it is to actually check the data.

Ahead of the Fed’s decision, the Wall Street Journal naively reported that “a shift to higher rates is expected to hurt gold, which doesn’t pay interest and costs money to hold.”

Setting aside the fact that not everyone who holds gold incurs storage fees (it costs you nothing to keep gold coins in your own house), let’s consider the core assertion that higher rates hurt gold. Recent history shows that assertion to be utterly false.

The Fed’s last rate-raising campaign occurred from June 2004 to June 2006. Over that period gold wasn’t “hurt” at all. In fact, gold prices rose from under $400 an ounce in June 2004 to over $700 by May 2006.

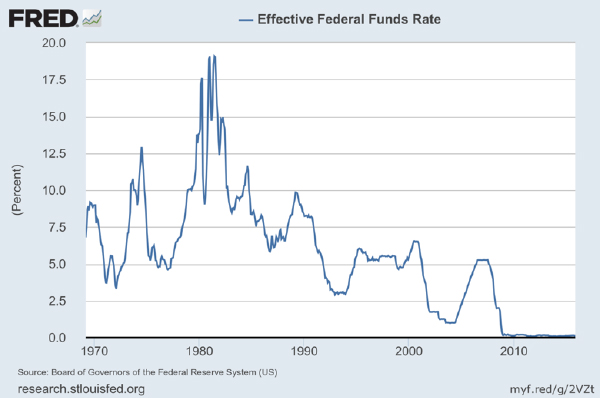

The historic run-up in gold and silver prices during the late 1970s coincided with the most aggressive rate-hiking effort in the Federal Reserve’s history. By the time gold and silver prices peaked in January 1980, the effective Federal Funds rate stood at 13.8%!

The myth of rising rates being bad for hard assets persists in spite of data that show the exact opposite is true.

Leave A Comment