Not only did the Fed miss its window of opportunity to hike rates, but it did so at the worst possible time, launching the first tightening cycle in 11 years just as US manufacturing entered its first recession since the financial crisis, just as the credit cycle entered its slowdown phase, and just as the default cycle is picking up, first in the energy sector one year ago and now spreading to all other industries. In fact, if the Fed had an alarm clock set to ring at 2:30pm, it hit snooze so many times, the alarm went off at 8pm according to Citigroup, “or possibly even later.” But as the chart below shows, while the Fed’s credibility will be crushed as a result, the Fed’s woeful alarm timing will have dire consequences for both equity and credit returns.

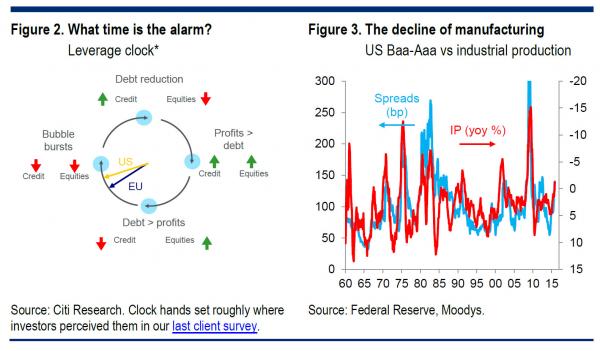

Here is a different perspective on the $4.5 trillion question: where in the credit cycle is the US economy, courtesy of Citigroup.

Typically rate rises start when profits are growing faster than debt and when companies are still deleveraging. This is around “half-past two” on our leverage clock2: 1994 and 2004 both fit this pattern. Now, with companies having been leveraging up for the past four years, and net debt/EBITDA in both Europe and especially the US at its highest non-recessionary level ever, it feels more like eight o’clock, or possibly even later (Figure 2).

What does being 6 hours late to your own rate hike party mean? The two downward facing red arrows in the left chart explain everything.

The rest follows logically, with Citi admitting that as of this moment “we have had all the improvement in growth and in profits we are likely to get.” However, the best part is when Citi’s Matt King, head of credit strategy, openly mocks “equity investors.”

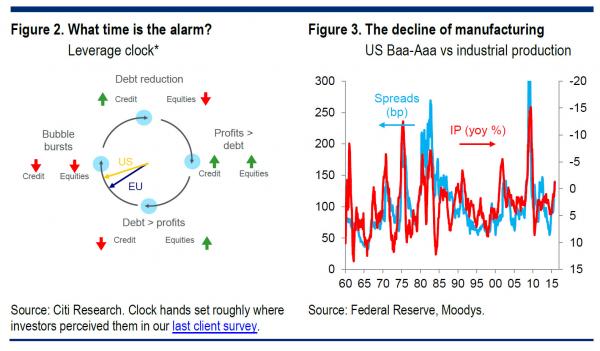

This is why we think the historical pattern of “credit spreads do well when central raise rates” is a poor guide in present circumstances. Credit spreads do well when the economy is recovering, and when profits are improving. This time around, it seems likely we have had all the improvement in growth and in profits we are likely to get. Indeed, the decline in the past few quarters’ EBITDA, and now in the last quarter’s US EPS, makes us feel dangerously close to the normal tipping point at which even equity investors realize that leveraging up is unsustainable, and credit and equities both sell off in a mutually reinforcing spiral. With industrial production growth negative, you could argue that the global manufacturing sector looks like it is in recession already (Figure 3).

Leave A Comment